TL;DR Summary

Berkshire Hathaway (BRK.A, BRK.B:NYSE) delivered solid Q1 2026 results, with operating earnings up ~17% year-over-year and continued strength in insurance underwriting. However, because earnings were released on a Saturday, the market reaction came on Monday—where BRK-B closed at $468.52, down 0.95%.

The muted decline suggests not a concern about fundamentals, but a lack of new catalysts—particularly around capital deployment.

Quarter Recap

Berkshire reported Q1 2026 earnings on May 2, 2026.

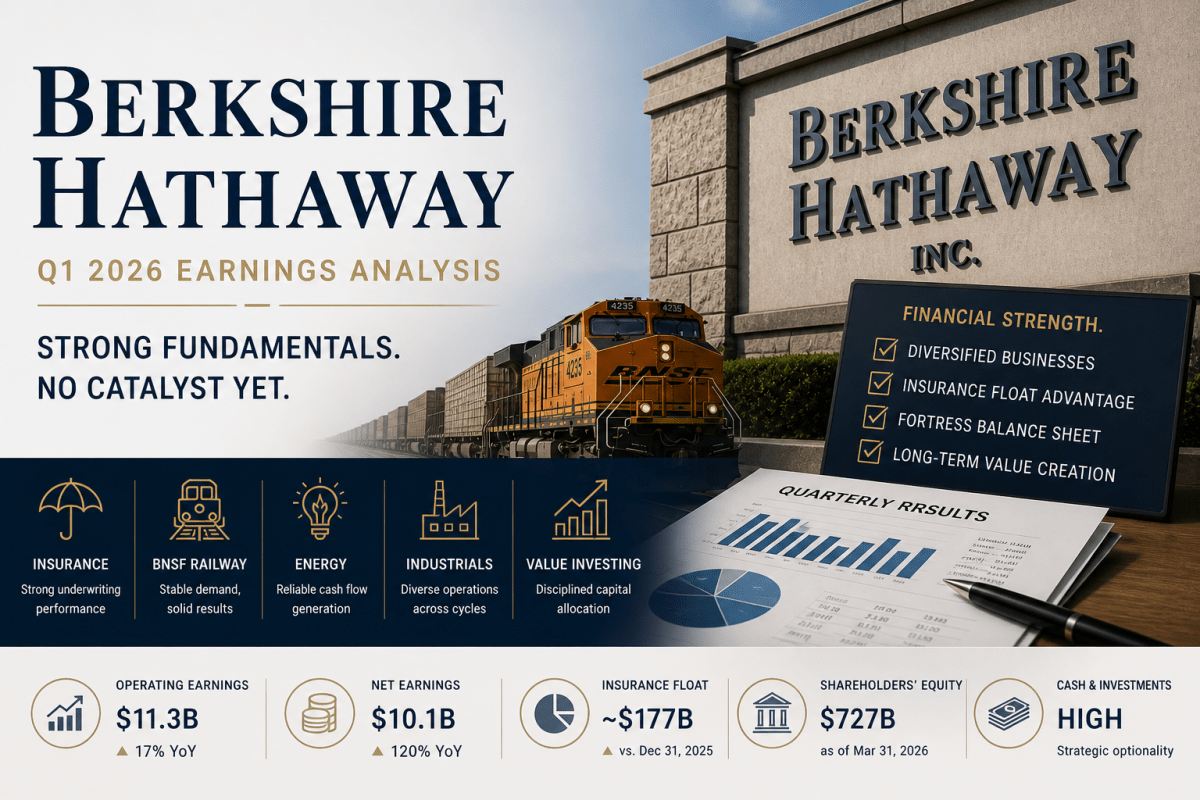

Key figures from official filings:

- Operating earnings: ~$11.3B (vs ~$9.6B last year)

- Net earnings: ~$10.1B (volatile due to investment swings)

- Revenue: ~$93.7B

The core story remains consistent:

insurance continues to anchor the business, while rail, energy, and industrial operations provide steady, diversified earnings.

Key Highlights

- Insurance underwriting improved, reinforcing a favorable cycle

- Float expanded to approximately $177B, strengthening Berkshire’s capital base

- BNSF delivered higher earnings, reflecting stable demand

- Investment income declined slightly, showing rate sensitivity

- Cash remains elevated, with limited visible deployment

Market Reaction — What Actually Happened

Berkshire released earnings on Saturday, when it closed on Monday (May 4, 2026):

- BRK-B closed at $468.52

- Down ~0.95%

What this tells us:

- The market did not react negatively to the earnings quality

- Instead, it reacted to what was missing

👉 No major acquisition

👉 No aggressive buyback signal

👉 No shift in capital allocation strategy

In other words:

The market is not questioning Berkshire’s business — it is questioning the next move.

SWOT Analysis

Berkshire is best understood as a capital allocation platform rather than a traditional operating company. Its valuation is driven by how effectively it deploys capital across cycles.

Strengths

- Insurance float as low-cost leverage (+5% to +10%)

~$177B float provides structural funding advantage and enhances long-term returns. - Diversified earnings engine (+3% to +6%)

Insurance, rail, energy, and industrial businesses create resilience across cycles. - Proven capital allocation track record (+5% to +8%)

Long-term value creation is driven by disciplined investment decisions. - Fortress balance sheet (+2% to +4%)

High liquidity provides downside protection and strategic flexibility.

Weaknesses

- Capital deployment drag (-3% to -6%)

Large cash reserves dilute returns when not actively deployed. - Succession uncertainty (-2% to -5%)

Future capital allocation quality remains a key unknown. - Conglomerate discount (-2% to -4%)

Structural complexity leads to valuation discount versus sum-of-parts.

Opportunities

- Large-scale acquisitions in downturns (+5% to +12%)

Berkshire’s biggest upside comes during market dislocations. - Higher interest income on cash (+2% to +4%)

Elevated rates increase returns on idle capital. - Insurance cycle tailwinds (+3% to +6%)

Strong underwriting conditions can drive outsized profits.

Threats

- Equity portfolio volatility (-4% to -10%)

Reported earnings remain sensitive to market movements. - Scale limitation (-3% to -7%)

Berkshire’s size limits high-return opportunities. - Catastrophe risk (-3% to -8%)

Large insurance events can materially impact results.

Valuation Scenarios

Berkshire’s valuation depends less on earnings beats and more on capital deployment and earnings durability.

Bear Case (25%)

- Limited capital deployment

- Insurance cycle weakens

- ~1.3x book multiple

👉 Estimated price: $400–420

Base Case (50%)

- Stable earnings growth

- Moderate buybacks

- No major acquisition

👉 Estimated price: $460–480

Bull Case (25%)

- Major capital deployment at attractive returns

- Strong insurance cycle persists

- Multiple expansion to ~1.7x book

👉 Estimated price: $520–550

Probability-Weighted Fair Value

👉 ~$470

Verdict

Berkshire Hathaway continues to execute exactly as expected:

steady earnings, strong underwriting, and unmatched balance sheet strength.

But the market reaction—a modest -0.95% decline on Monday—reveals the real issue:

This is no longer a story about earnings. It’s a story about capital deployment.

At current levels, the stock appears fairly valued.

The upside will not come from incremental earnings—it will come from decisive capital allocation.

Call to Action

If you’re a long-term investor, Berkshire remains a core holding for stability and compounding.

But if you’re looking for upside:

👉 Watch the cash.

👉 Watch the deals.

That’s where the next move will come from.

Follow SWOTstock for more earnings breakdowns grounded in official filings and real investor thinking.

Disclaimer

This article is for informational purposes only and does not constitute financial advice. Always conduct your own research before making investment decisions.