TL;DR Summary

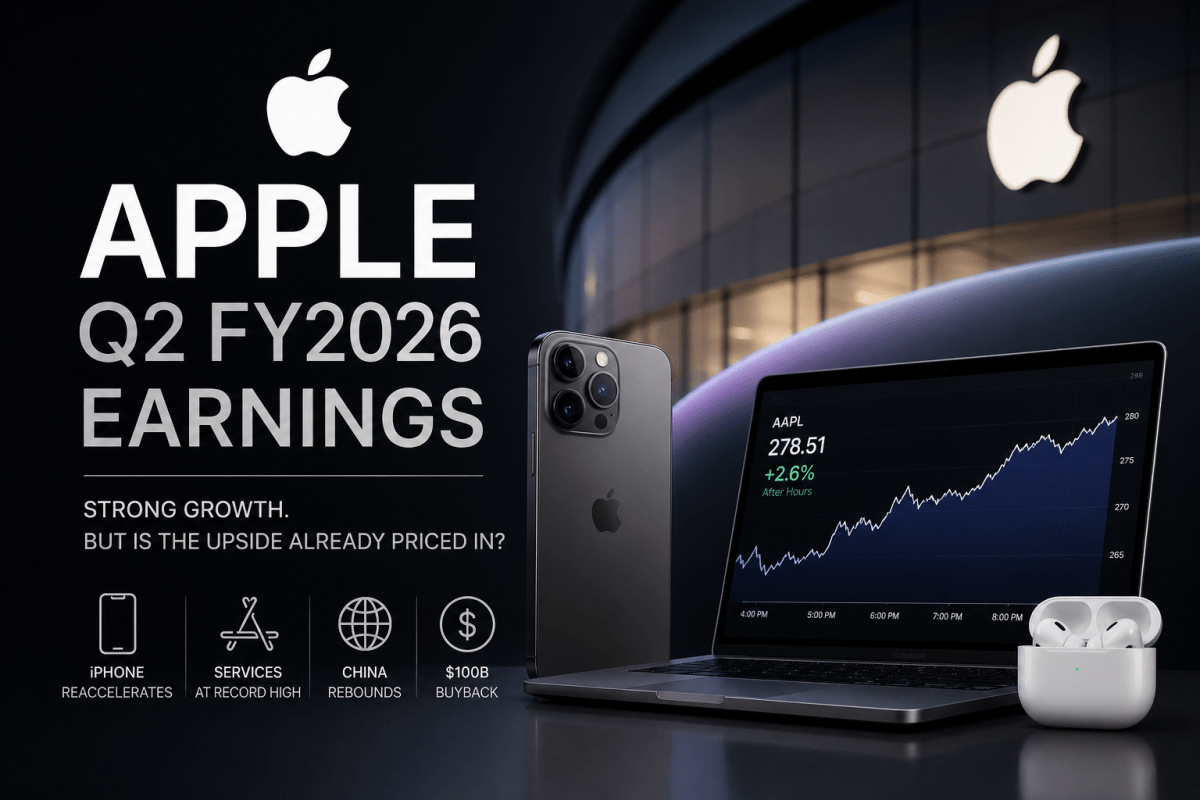

Apple Inc. (AAPL:NASDAQ) delivered a strong quarter, with growth driven by iPhone momentum, Services expansion, and a clear rebound in China. The business looks as durable as ever.

But the story is shifting.

At $278.51 after hours, the question is no longer whether Apple is strong—it clearly is. The real question is whether the market is already pricing in the next phase of growth, particularly around AI.

At this level, Apple looks less like a value opportunity and more like a premium-quality stock where execution has to keep up with expectations.

Quarter Recap

Apple’s March quarter reinforced something investors have been debating for the past year: whether the company is slowing down or simply going through a temporary pause.

This quarter leans clearly toward the latter.

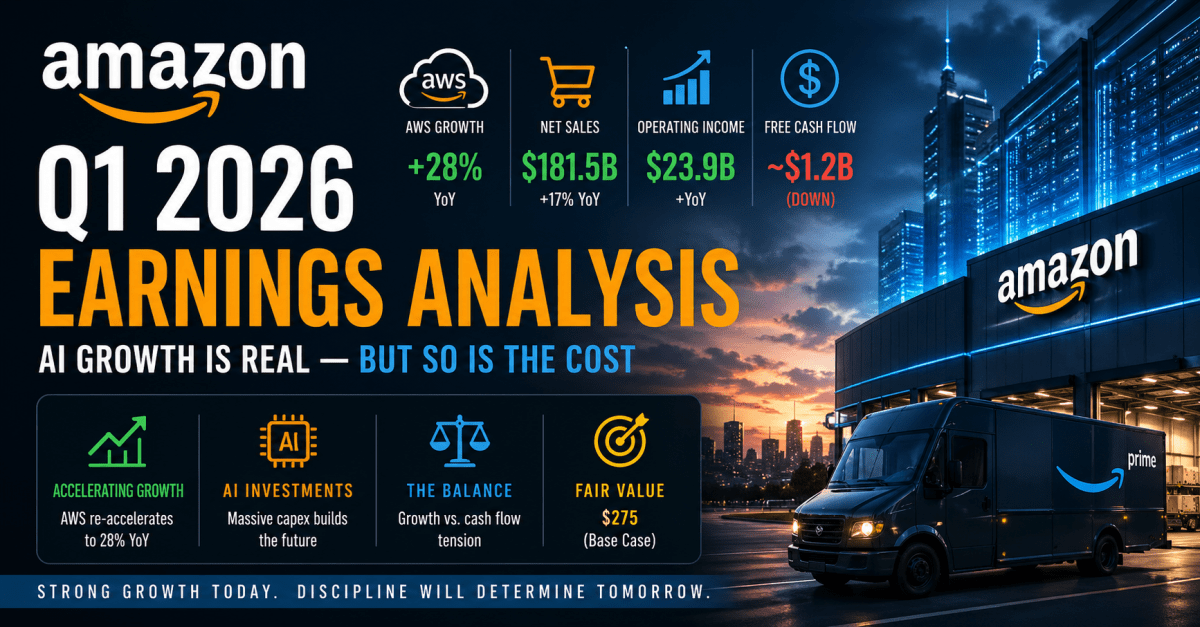

Revenue grew 17% year over year to $111.2B, while EPS rose 22% to $2.01, both record levels for a March quarter. More importantly, the growth came from the right places.

iPhone revenue reaccelerated meaningfully, pushing back against the narrative of a mature, flat cycle. Services reached another all-time high, continuing to strengthen the margin profile of the business. And China, which had been a persistent concern, showed a clear rebound.

Taken together, this was not just a “good quarter.” It was a quarter that removed several key risks at once.

At the same time, Apple reinforced its capital return strategy, announcing another $100B buyback authorizationalongside a dividend increase. That continues to anchor the stock as a long-term cash flow compounder.

Key Highlights

If you had to summarize the quarter in one idea, it would be this:

Apple didn’t introduce a new story—it strengthened the existing one.

iPhone demand came in stronger than expected, suggesting that the upgrade cycle still has life. Services continued to scale, providing a structural margin advantage. And China stabilized, reducing one of the biggest downside risks investors had been pricing in.

None of these are new drivers individually. But seeing them all move in the right direction at the same time is what matters.

Market Reaction

The market response was positive but controlled. After-hours trading pushed the stock up about +2.6% to $278.51.

That move is telling.

This wasn’t a euphoric reaction. It was a confirmation move.

Investors are not suddenly discovering Apple’s strength—they already believed in it. What this quarter did was increase confidence in that belief, particularly around iPhone demand and China.

But the limited magnitude of the move also suggests something else:

The market is no longer reacting to Apple as a “surprise growth story.” It is reacting to it as a high-confidence, already-priced-in compounder.

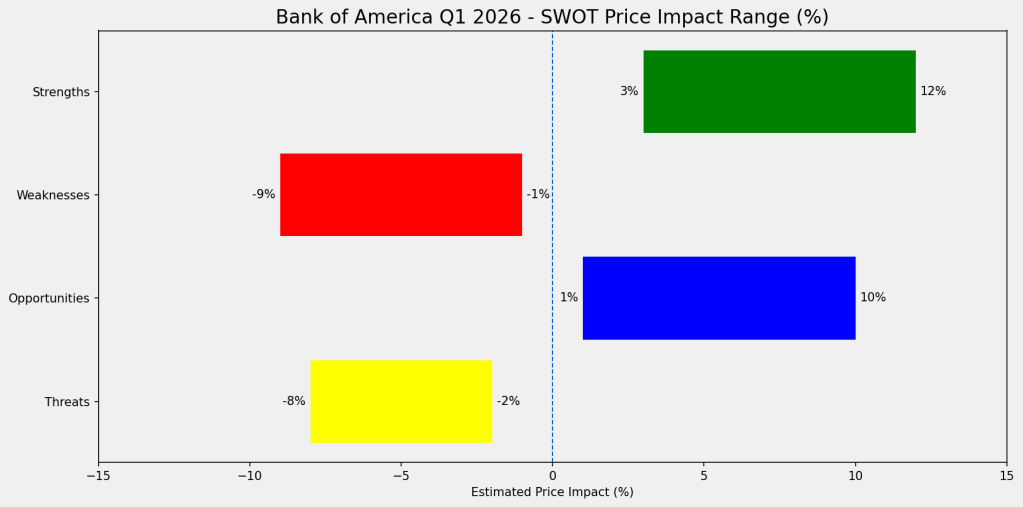

SWOT Analysis (with Price Impact Ranges)

Apple’s investment case now revolves around a different question than it did a few years ago. It is no longer about whether the company can grow—it is about whether that growth can justify the premium investors are already paying.

Strengths

Apple’s biggest strength remains its ecosystem, now reinforced by a reaccelerating iPhone cycle and a rapidly expanding Services business. Together, they create a combination of demand stability and margin durability that very few companies can replicate.

Estimated impact: +4% to +7% (iPhone strength), +3% to +5% (Services), +2% to +4% (capital return)

Weaknesses

At the same time, Apple’s scale is becoming a constraint. With such a large revenue base, even strong execution translates into incremental growth rather than step changes. The continued reliance on iPhone also means the business is still tied to product cycles.

Estimated impact: -3% to -5% (concentration), -2% to -4% (scale limitations)

Opportunities

The most important upside driver is not in the current numbers—it is in what could come next. AI integration across Apple’s ecosystem has the potential to unlock a new narrative, particularly if it leads to monetizable services or device differentiation.

China’s recovery, if sustained, also adds to the upside by reversing a previously negative sentiment driver.

Estimated impact: +5% to +10% (AI), +3% to +6% (China recovery)

Threats

The key risks are tied to normalization. A strong iPhone quarter can be followed by a weaker one if demand was pulled forward. At the same time, regulatory pressure on the App Store and ecosystem could affect the high-margin Services segment.

Estimated impact: -4% to -7% (demand normalization), -3% to -6% (regulation)

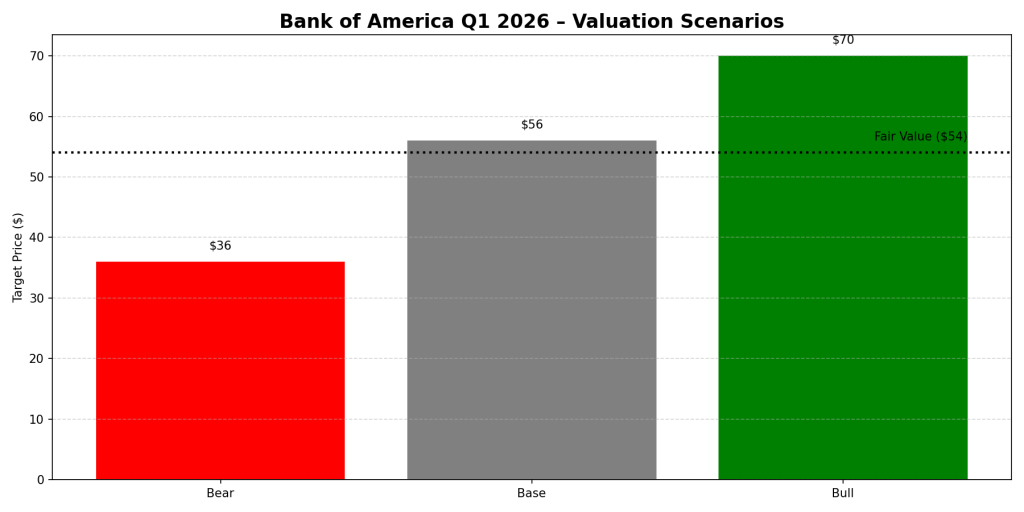

Valuation Scenarios

Apple’s valuation today is less about whether it will grow and more about how much of that growth is already reflected in the price.

Using a ~$8.00 EPS run-rate and a reasonable multiple range:

- In a bear case, where growth normalizes and no new driver emerges, the stock could justify a valuation closer to $192.

- In a base case, where Apple continues its current trajectory as a stable compounder, fair value sits around $224.

- In a bull case, where AI meaningfully expands the growth profile, valuation could reach $256.

That leads to a probability-weighted fair value of roughly $220–225.

Verdict

This is where the story changes.

At $278.51, Apple is not just reflecting its current strength—it is reflecting future expectations that have not yet materialized in the numbers.

That doesn’t make it a bad investment. But it does change the nature of the investment.

You are no longer buying Apple because it is undervalued. You are buying it because you believe:

The next layer of growth—most likely AI-driven—will justify today’s premium.

That introduces a different kind of risk. Not execution risk, but expectation risk.

At this level, the setup is no longer balanced. The downside, if expectations don’t materialize, is meaningfully larger than the upside from current fundamentals alone.

Call to Action

Apple remains one of the highest-quality businesses in the market. That hasn’t changed.

What has changed is the price you are being asked to pay.

The key question now is simple:

Are you investing in Apple’s current business—or in what it might become next?

Follow SWOTstock for grounded, investor-focused analysis that connects earnings to real valuation implications—not just headlines.

Disclaimer

This content is for informational purposes only and does not constitute investment advice. All financial data is based on official company disclosures. Valuation estimates are based on assumptions and should not be interpreted as predictions. Always conduct your own research before making investment decisions.