TL;DR Summary

Amazon (AMZN:NASDAQ) delivered a strong Q1 2026 with accelerating AWS growth and expanding operating income, reinforcing its position as a core AI infrastructure player. However, massive AI-driven capex has compressed free cash flow, creating a key tension for investors. The stock is trading near fair value, with upside dependent on whether AI investments translate into durable returns.

Quarter Recap

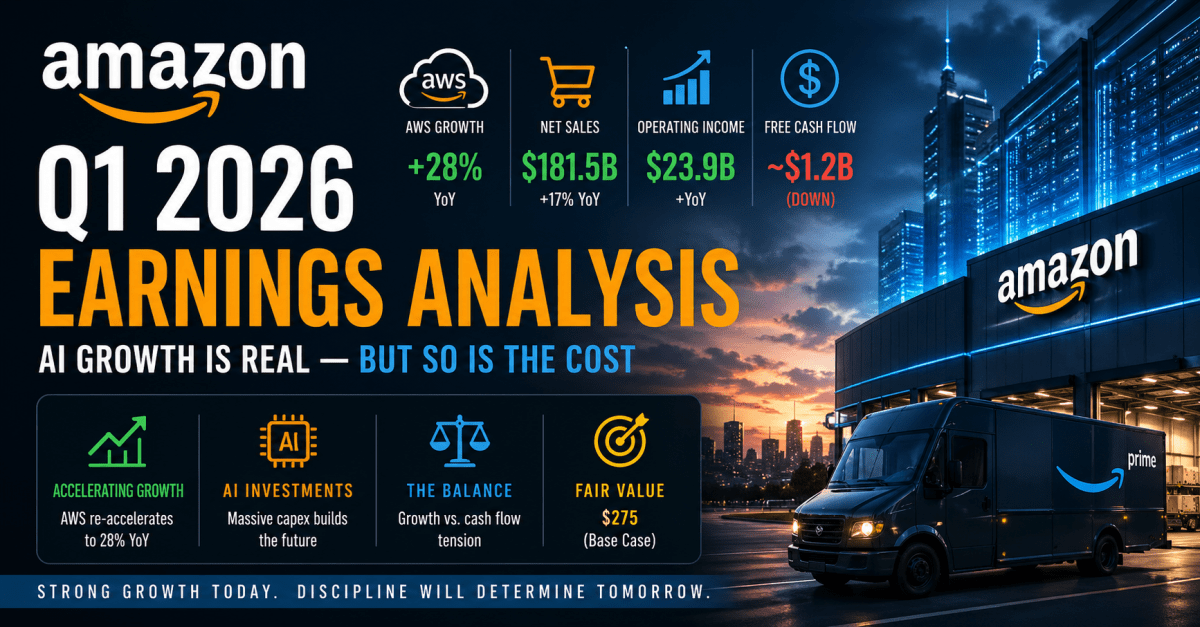

Amazon reported a solid Q1 2026, with revenue growing 17% year-over-year to $181.5 billion. The standout was AWS, which accelerated to 28% growth, marking a clear inflection after several quarters of slower expansion.

Operating income increased significantly, reflecting both stronger cloud profitability and continued efficiency improvements in the retail segment. However, net income was boosted by a large non-operating gain related to Amazon’s investment in Anthropic, which means headline earnings should be interpreted with caution.

At the same time, Amazon sharply increased capital expenditures, particularly in AI infrastructure, which led to free cash flow falling close to breakeven despite strong operating performance.

Key Highlights

Amazon’s quarter reinforces a structural shift in its business model. AWS and advertising continue to scale as high-margin engines, while retail is becoming more efficient and less of a drag on profitability.

The most important signal is AWS re-acceleration. A 28% growth rate suggests enterprise demand is returning, particularly driven by AI workloads. This positions Amazon firmly in the AI infrastructure race alongside its largest competitors.

However, the cost of that growth is rising. The surge in capital expenditure reflects an aggressive push to build out data centers, chips, and AI capacity. This creates a near-term tradeoff between growth and cash generation that investors cannot ignore.

SWOT Analysis

Amazon’s current positioning is defined by a simple dynamic: strong growth drivers are clearly visible, but the path to monetizing those drivers efficiently is still uncertain.

Strengths

- AWS re-acceleration (28% YoY growth) confirms strong AI-driven demand

Estimated price impact: +6% to +10% - High-margin businesses (AWS + Advertising) continue to scale, improving overall mix

Estimated price impact: +4% to +7% - Operating income expansion shows improving efficiency across segments

Estimated price impact: +3% to +5%

Weaknesses

- Free cash flow is compressed due to heavy AI-related capital expenditure

Estimated price impact: -5% to -8% - Earnings quality is partially distorted by non-operating investment gains

Estimated price impact: -2% to -4%

Opportunities

- AI monetization across AWS and enterprise services could unlock long-term pricing power

Estimated price impact: +8% to +15% - Continued logistics and retail efficiency improvements can drive margin expansion

Estimated price impact: +3% to +6%

Threats

- AI infrastructure arms race could lead to overinvestment and margin pressure

Estimated price impact: -6% to -10% - AWS growth remains exposed to enterprise spending cycles

Estimated price impact: -3% to -6%

Valuation Scenarios

Amazon’s valuation now hinges on whether its aggressive AI investment cycle will translate into sustained earnings growth or prolonged margin pressure.

Bear Case

AWS growth slows and AI investments fail to generate near-term returns, while margins come under pressure from continued infrastructure spending.

Estimated price: $220–$240

Base Case

AWS maintains strong growth, AI investments begin to show early monetization, and margins expand gradually over time.

Estimated price: $260–$290

Bull Case

AI demand accelerates further, AWS growth strengthens, and Amazon achieves meaningful operating leverage from its high-margin segments.

Estimated price: $300–$340

Probability-Weighted Fair Value

Combining these scenarios, the estimated fair value is approximately $275, placing the current price near fair value with limited margin of safety.

Verdict

Amazon is no longer just an e-commerce and cloud company — it is now firmly positioned as an AI infrastructure platform. The growth story is real, but so is the cost of building that future.

At current levels, the stock reflects cautious optimism. Investors are willing to believe in the long-term AI opportunity, but they are waiting for clearer evidence that these investments will translate into sustainable cash flow.

This is not a deep value opportunity. It is a conviction-driven growth investment that requires confidence in management’s ability to convert scale into returns.

Call to Action

If you believe Amazon can successfully monetize its AI investments, the current valuation offers a reasonable entry point. If you are concerned about capital efficiency and cash flow, it may be worth waiting for clearer signs of return on investment.

Follow SWOTstock for more structured, investor-focused earnings analysis grounded in official company data.

Disclaimer

This analysis is for informational purposes only and does not constitute financial advice. Always conduct your own research and consult with a licensed financial advisor before making investment decisions.