TL;DR Summary

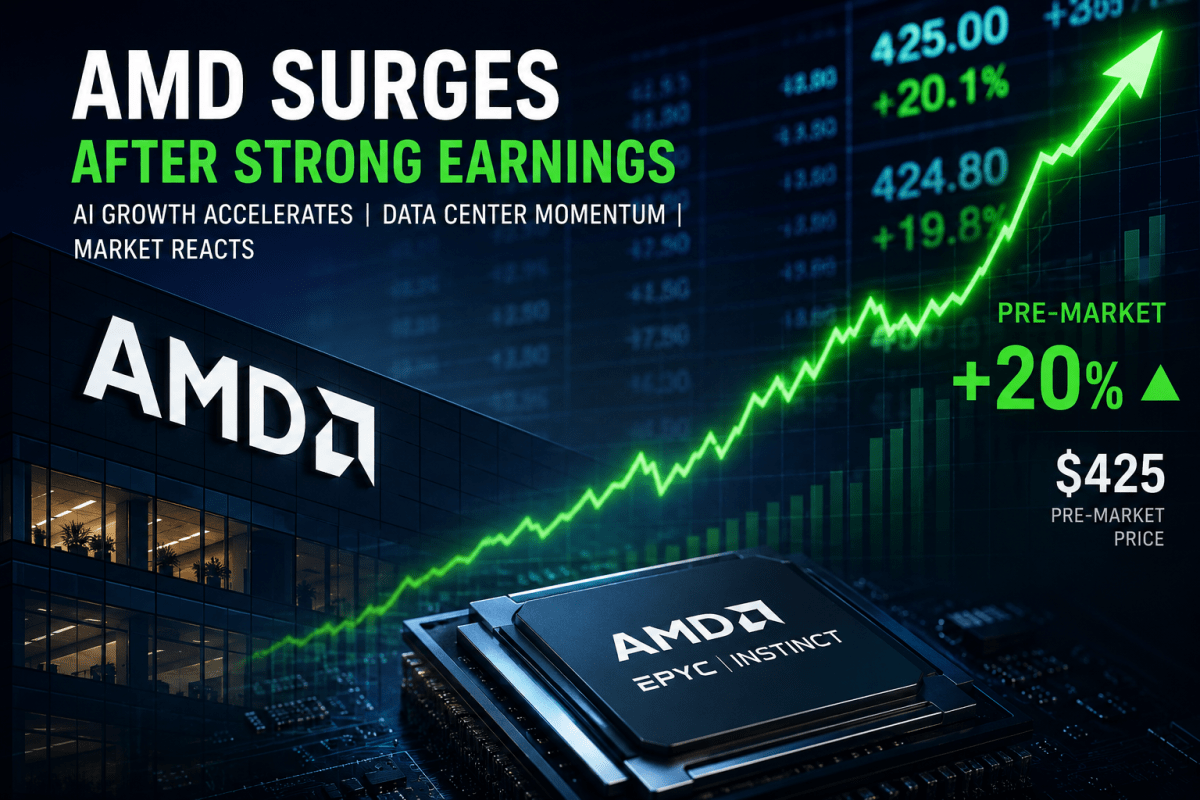

Advanced Micro Devices (AMD:NASDAQ) delivered a clear AI-driven breakout in Q1 2026, triggering a ~20% pre-market gain at one time, re-rating from ~$355 to ~$425. The market is no longer questioning AMD’s role in AI—it is pricing in continued execution. The key question now is not whether AMD can grow, but whether it can outperform already elevated expectations. Upside remains, but risk has shifted toward expectation compression.

Quarter Recap

AMD’s Q1 2026 results confirm a structural shift in the business.

The company is no longer driven by a balanced portfolio across client, gaming, and embedded segments. Instead, growth is now clearly concentrated in Data Center, powered by EPYC CPUs and MI300 AI accelerators.

Client showed early signs of stabilization after a prolonged downturn, while Gaming and Embedded continued to decline due to cyclical normalization and inventory digestion. Profitability improved, supported by a mix shift toward higher-margin AI and data center products.

Management emphasized strong hyperscaler demand and an accelerating AI deployment pipeline, reinforcing that AMD is now positioned as a meaningful participant in AI infrastructure.

Key Highlights

AMD’s earnings were not just “good”—they were better than what the market had already priced in.

The most important takeaway is that AI is no longer a future narrative for AMD. It is now the current growth engine, with real revenue contribution and margin impact.

However, this strength is not evenly distributed. Legacy segments remain weak, and the company is increasingly dependent on continued AI momentum to sustain growth.

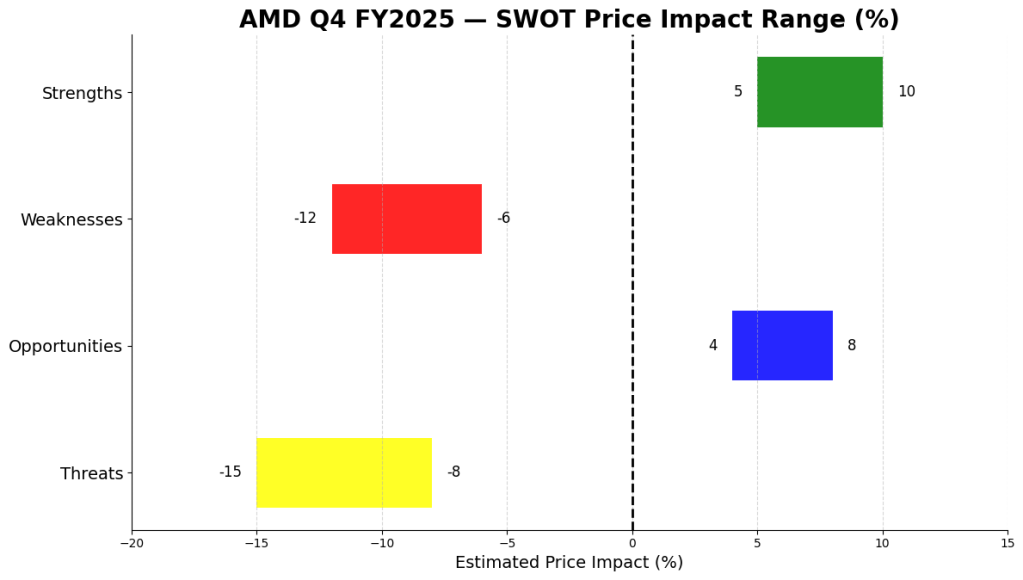

SWOT Analysis (with Price Impact)

AMD’s valuation must now be understood in the context of a post-re-rating stock. The ~20% jump pre-market reflects a shift in expectations, not just fundamentals.

Strengths

AMD’s AI and data center business has reached an inflection point. The MI300 ramp and EPYC demand validate that AMD is no longer an AI outsider. This directly drove the recent re-rating and remains the core upside driver, contributing an estimated +10% to +20% impact on valuation.

At the same time, the mix shift toward higher-margin AI products is improving profitability, supporting an additional +5% to +10% upside.

Weaknesses

Despite strong hardware progress, AMD still trails NVIDIA in software ecosystem strength. CUDA remains a significant moat, limiting AMD’s ability to fully capture AI demand. This gap represents a -10% to -20% valuation drag.

Additionally, AMD’s reliance on AI is increasing as other segments underperform. Gaming and Embedded remain weak, creating concentration risk, with a -5% to -10% impact.

Opportunities

The AI market remains the largest opportunity. If AMD continues to gain share in hyperscaler and enterprise deployments, the upside is substantial, contributing +20% to +40% potential.

AMD also benefits from being a credible second supplier in a market dominated by NVIDIA. Hyperscalers are actively seeking alternatives, creating a structural tailwind worth +10% to +20%.

Threats

The biggest risk is no longer execution—it is expectations.

After a ~20% move, the market now requires AMD to consistently exceed forecasts. Any sign of normalization could trigger -20% to -35% downside through multiple compression.

Competition remains intense. NVIDIA continues to innovate aggressively, while companies like Amazon and Microsoftare investing in in-house AI chips. This creates a -10% to -25% risk to long-term positioning.

SWOT Summary Table

| Category | Factor | Price Impact |

|---|---|---|

| Strength | AI/Data Center breakout | +10% to +20% |

| Strength | Margin expansion | +5% to +10% |

| Weakness | NVIDIA ecosystem gap | -10% to -20% |

| Weakness | AI concentration risk | -5% to -10% |

| Opportunity | AI market share expansion | +20% to +40% |

| Opportunity | Second supplier advantage | +10% to +20% |

| Threat | Expectation compression | -20% to -35% |

| Threat | Competitive pressure | -10% to -25% |

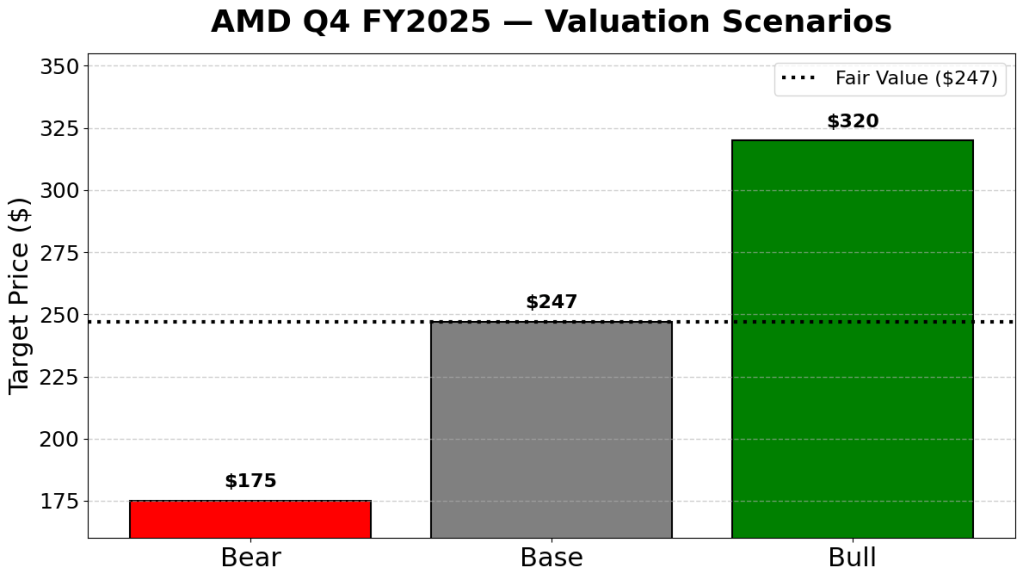

Valuation Scenarios

AMD is now trading at approximately $425 post-earnings, following a significant re-rating.

Instead of relying on arbitrary EPS assumptions, we anchor valuation to business outcomes and market positioning.

- Bear Case ($200–300): AI growth slows or fails to exceed expectations. Multiple compresses as the narrative weakens.

- Base Case ($300–400): AMD executes well, with steady AI growth and margin improvement.

- Bull Case ($400–600+): AMD achieves meaningful AI share gains and is re-rated closer to top-tier AI infrastructure players.

Verdict

AMD has successfully crossed the most important threshold—it has proven that it belongs in the AI conversation.

However, the stock is no longer early. At ~$425, the market is already pricing in a significant portion of future success.

This creates a shift in the investment thesis. AMD is no longer a “discovery” story but an execution story, where upside depends on consistently exceeding already high expectations.

For investors, this means the risk-reward profile has become more balanced, with less margin for error.

Call to Action

If you’re following AI infrastructure stocks, AMD is now a critical name to watch—not for its potential, but for its ability to deliver quarter after quarter.

Follow SWOTstock for grounded, investor-focused earnings analysis that separates facts, market reaction, and real valuation thinking.

Disclaimer

This content is for informational purposes only and does not constitute financial advice. Investors should conduct their own research and consider their risk tolerance before making investment decisions.