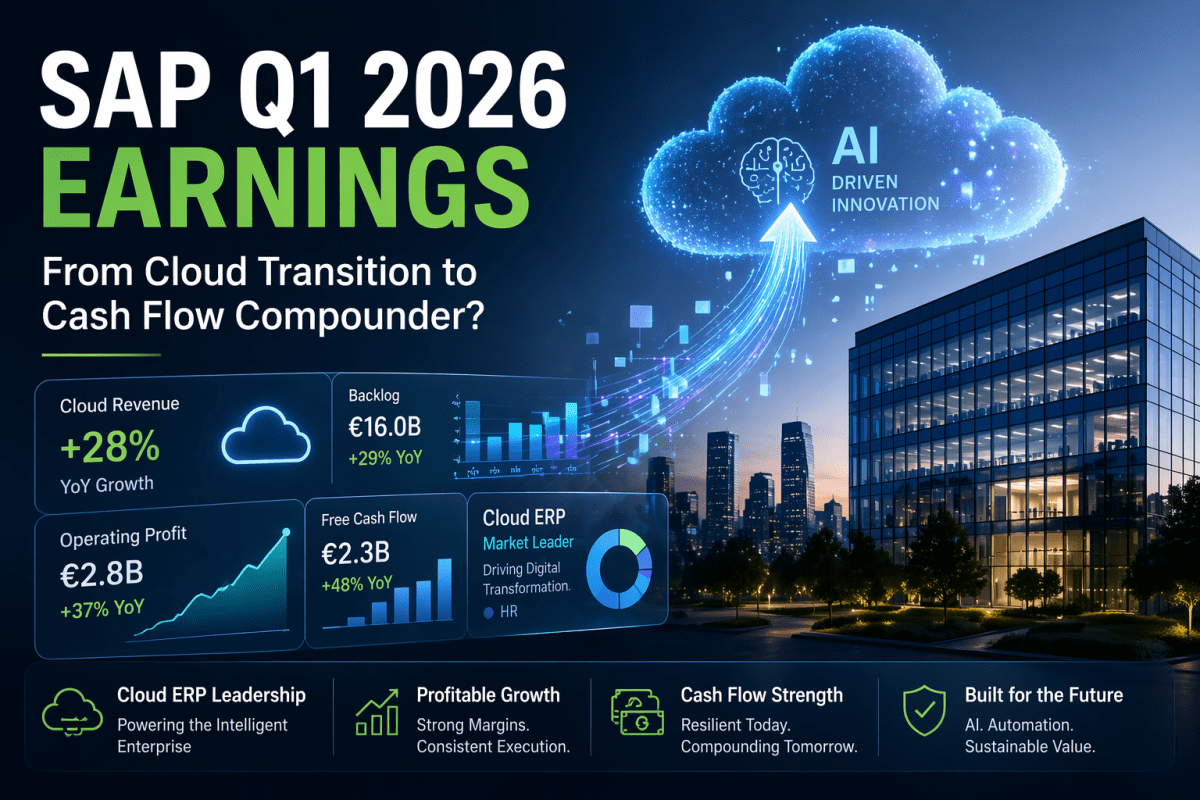

TL;DR

SAP (SAP:NYSE) delivered a strong Q1 2026 with accelerating cloud ERP growth, rising backlog visibility, and expanding margins. The stock’s ~+6% post-earnings reaction signals that investors are regaining confidence in SAP as a durable, high-quality enterprise software compounder.

However, the key debate has shifted: this is no longer about turnaround — it’s about whether SAP deserves a premium valuation.

Quarter Recap

SAP’s Q1 results confirmed that its multi-year cloud transition is not only intact but strengthening. Cloud backlog rose to €21.9B, growing 25% in constant currency, while cloud ERP suite revenue accelerated to 30% growth.

At the same time, profitability improved meaningfully, with operating profit rising 24% in constant currency. This combination — growth plus margin expansion — is exactly what long-term investors look for in a maturing software platform.

Yet, SAP did not raise full-year guidance. That detail matters more than it looks.

Key Highlights

SAP’s quarter can be summarized as follows:

- Strong cloud backlog growth reinforcing revenue visibility

- Continued dominance in cloud ERP, the company’s core moat

- Clear operating leverage and margin expansion

- Ongoing decline in legacy license and services revenue

- Stable (not upgraded) FY2026 guidance

This creates a tension between strong execution today and uncertainty about the growth trajectory ahead.

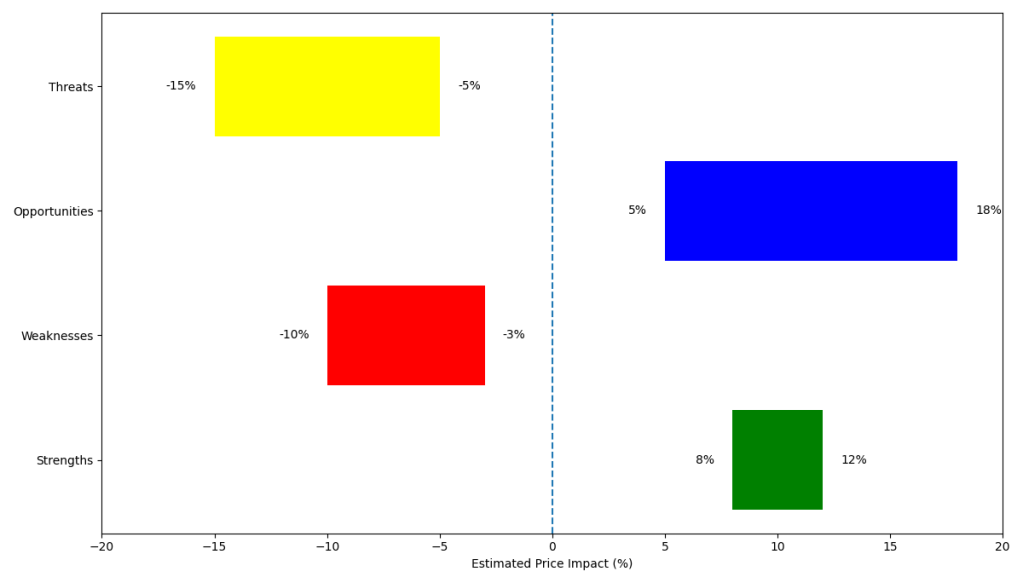

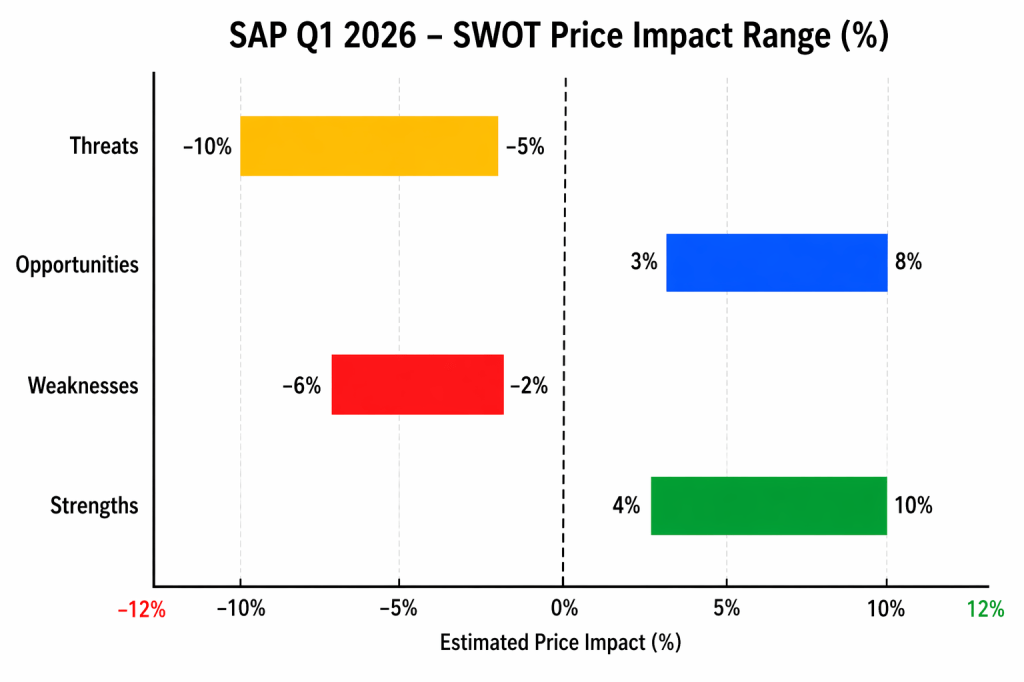

SWOT Analysis (with Price Impact)

SAP’s current positioning reflects a transition into a quality compounder, but not without risks.

Strengths

SAP’s backlog growth provides strong forward visibility, reducing downside risk and supporting valuation stability. At the same time, its cloud ERP suite continues to expand rapidly, reinforcing its dominance in mission-critical enterprise systems. Combined with rising operating leverage, SAP is increasingly viewed as a cash flow engine rather than just a cloud transition story.

Weaknesses

The decline in legacy license and services revenue continues to weigh on overall growth perception. More importantly, the decision to maintain — rather than raise — full-year guidance introduces uncertainty about how sustainable the current growth momentum really is.

Opportunities

SAP is uniquely positioned to embed AI into existing ERP workflows, which could unlock incremental monetization. In parallel, continued margin expansion could justify a re-rating toward premium software multiples.

Threats

Growth normalization remains the biggest risk. SAP itself signaled that Q1 benefited from timing effects, with slower growth expected in Q2. In addition, macro and geopolitical assumptions embedded in guidance introduce external uncertainty uncommon for software firms.

| Category | Driver | Price Impact |

|---|---|---|

| Strength | Backlog visibility | +6% to +10% |

| Strength | Cloud ERP dominance | +5% to +9% |

| Strength | Margin expansion | +4% to +8% |

| Weakness | Legacy decline | -3% to -6% |

| Weakness | No guidance raise | -2% to -5% |

| Opportunity | AI monetization | +3% to +8% |

| Opportunity | Multiple expansion | +4% to +7% |

| Threat | Growth normalization | -5% to -10% |

| Threat | Macro/geopolitical risk | -3% to -7% |

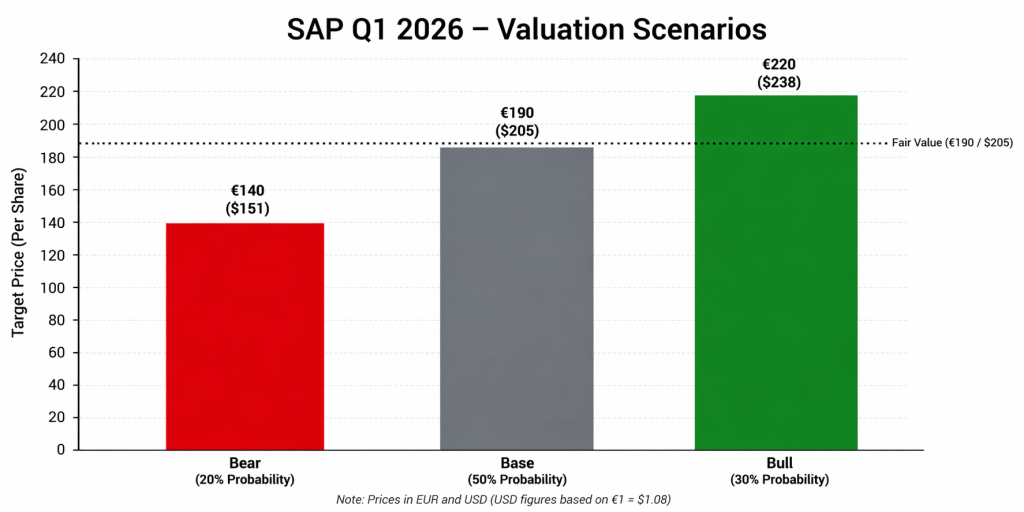

Valuation Scenarios (EUR & USD)

The ADR closing price after earnings released was ~USD175, up more than 7%

- FX assumption: €1 ≈ $1.08

Bull Case (30% probability)

SAP successfully transitions into a premium compounder with sustained ERP growth and continued margin expansion.

- EUR: €210 – €230

- USD: $227 – $248

Base Case (50% probability)

Growth moderates but remains durable. SAP trades as a high-quality but mature enterprise software leader.

- EUR: €184 – €196

- USD: $199 – $212

Bear Case (20% probability)

Growth slows faster than expected, and Q1 proves to be a peak quarter.

- EUR: €130 – €150

- USD: $140 – $162

Probability-Weighted Outcome

- Expected fair value range:

→ €187 – €193

→ $202 – $208

This implies moderate upside from current levels, but not a deep margin of safety.

Verdict

SAP is no longer a turnaround story. It is evolving into a high-quality enterprise compounder with strong cash flow characteristics.

But that evolution comes with a new challenge:

The market is already starting to price it that way.

For investors, the opportunity is not in identifying whether SAP is improving — that is now clear. The real question is whether the current valuation fully reflects that improvement.

Call to Action

If you are a long-term investor, SAP remains a strong candidate for a core portfolio holding, especially if you believe in the durability of enterprise ERP systems.

However, this is no longer a stock to chase aggressively. Entry discipline matters more than ever.

Disclaimer

This analysis is for informational purposes only and does not constitute financial advice. Always conduct your own research and consider your risk tolerance before making investment decisions.