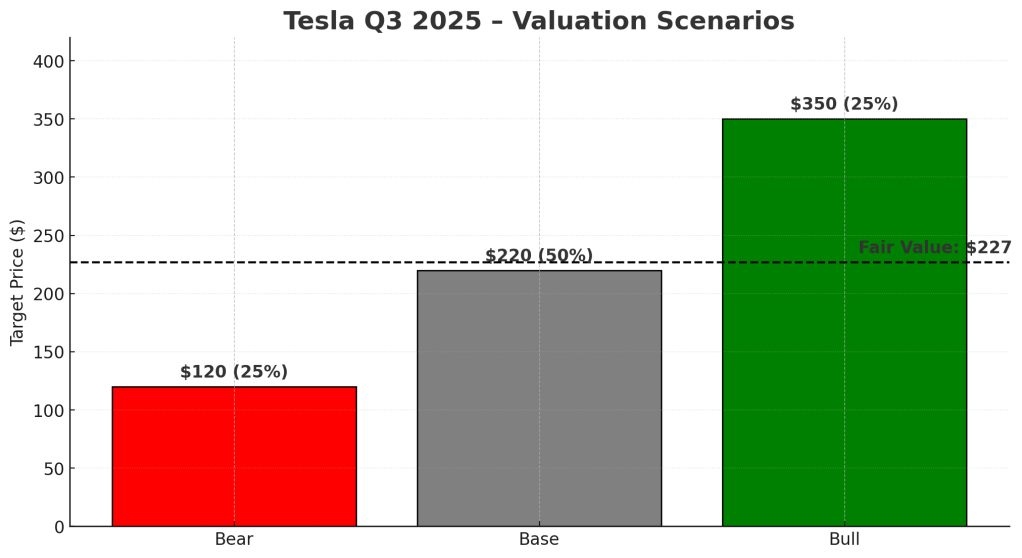

Tesla’s Q3 results show record revenue of $25.2 billion and net income of $2.1 billion. While margins are recovering, they remain below 2022 levels. The fair value estimate is $227 per share, with current valuation suggesting a hold recommendation. Investors should consider a buy zone around $180-$190.

TL;DR:

Tesla reported record Q3 revenue of $25.2 B (+7.8 %) and net income of $2.1 B (+11 %), but margin recovery remains shallow.

The fair value sits near $227/share — reasonable for holders, not yet a bargain for new buyers.

📊 Quarter Recap

• Revenue $25.2 B (+7.8 %)

• Gross Profit $5.65 B (+13 %)

• Operating Income $2.17 B (+29 %)

• Free Cash Flow $1.47 B (+61 %)

• Auto Gross Margin 19.6 % (↑ 1.3 pts YoY)

Margins have stabilized after two years of price cuts — but at ~19 %, still far below the 25 % peak of 2022.

Each 1 pt margin shift ≈ $1 B impact to net income.

💬 Management Tone

“We’re entering the autonomy era — vehicle hardware is ready.” – Elon Musk

“Capex will rise into 2026 as we ramp Optimus and Dojo.” – CFO

Translation: positive cash flow continues, but the AI and robotics push keeps capex heavy. Patience required.

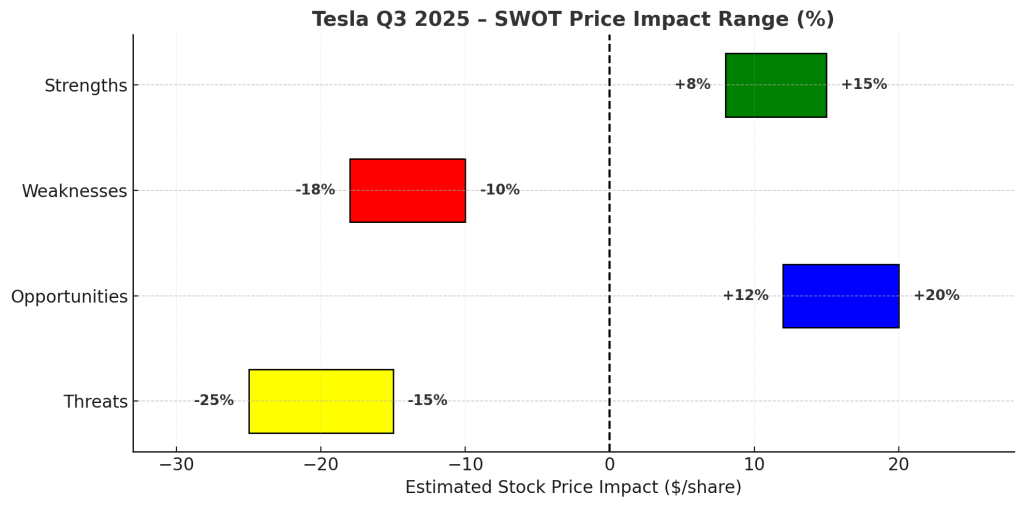

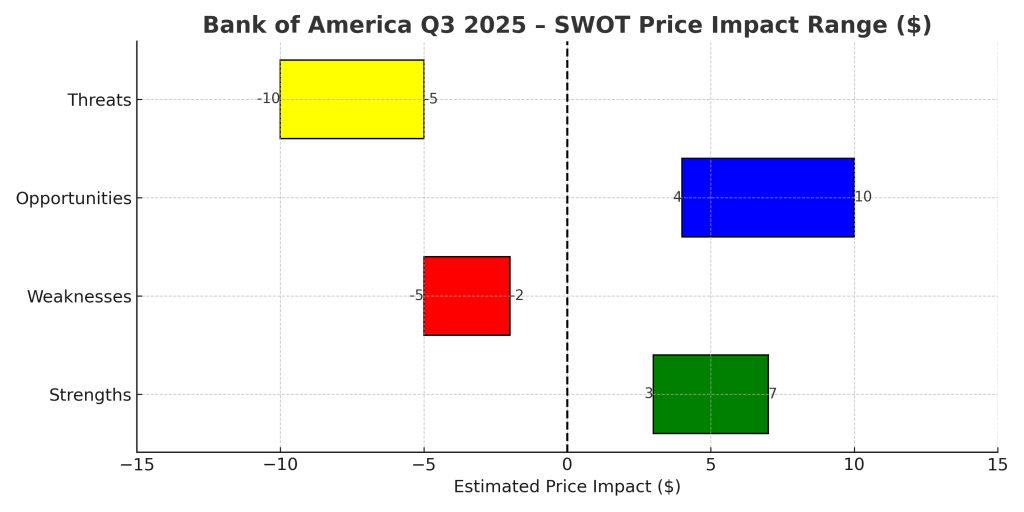

🧩 SWOT Summary (Price Impact Ranges)

Strengths (+8 – 15 %)

– Vertically integrated EV + AI ecosystem

– $25 B net cash cushion

– Sequential margin recovery

Weaknesses (–10 – 18 %)

– Margins well below 2022 levels

– Tariff + mix pressure

– Energy unit still small

Opportunities (+12 – 20 %)

– FSD subscriptions and Dojo compute could add 1–2 pts to margin

Bank of America demonstrated strong Q3 2025 results with an EPS of $1.06 and a net interest income of $15.2 billion, alongside a 43% rise in investment-banking fees. Management’s increased Q4 guidance reflects confidence. The bank’s stability positions it as a reliable choice for value investors amid economic uncertainty.

TL;DR

Bank of America reported a steady and resilient Q3 2025: EPS came in at $1.06, net interest income rose to $15.2 billion, and investment-banking fees jumped 43%. Management also raised Q4 NII guidance, signaling confidence heading into year-end. After the release, the stock traded roughly 2–3% higher, reflecting a market that values stability in a choppy macro environment. For DIY value investors, this quarter underscores BofA’s role as a dividend-reliable, moderately undervalued financial anchor rather than a high-beta trade.

Quarter Recap

Bank of America delivered a steady and confident performance in Q3 2025, leaning more on disciplined execution than dramatic surprises. Net income reached $8.5 billion, translating to $1.06 per share, comfortably above expectations and supported by $15.2 billion in net interest income that remained resilient despite shifting rate dynamics. Management emphasized that positive operating leverage reflected tighter cost control and continued investment in risk management and technology. Capital markets activity added a welcome boost, with investment-banking fees rising 43% as dealmaking and underwriting improved from last year’s lows. Importantly for long-term investors, the bank’s CET1 ratio stayed above 12%, reinforcing its capacity to maintain dividends and pursue selective buybacks even in a more uncertain macro backdrop. Overall, the quarter underscored BofA’s ability to produce stable, repeatable earnings at a time when many peers are navigating more uneven conditions.

Key Highlights

EPS: $1.06, above internal targets and analyst expectations.

Net Interest Income: $15.2B, maintaining upward momentum.

Investment-Banking Fees: +43% YoY, continued rebound in capital markets.

• Prolonged macro uncertainty affecting NII trajectory

Valuation Scenarios (12-Month Outlook)

Using official Q3 performance, NII guidance, and credit commentary:

Bull Case – $56 (+15%)

• Sustained NII strength

• Continued recovery in investment banking

• Flat credit losses into 2026

Base Case – $51.3 (+5%)

• Stable NII

• Moderate fee growth

• Expense discipline maintained

Bear Case – $44 (–10%)

• Margin compression from declining rates

• Credit costs rise toward the historical mean

• CRE pockets worsen

Probability-Weighted Fair Value:

(0.3 x 56) + (0.5 x 51.3) + (0.2 x 44) = approx. $51.1

Verdict

Bank of America continues to deliver what value-focused investors want: predictable earnings, conservative capital management, and a stable dividend.

This quarter didn’t redefine the company—but it didn’t need to.

Instead, it reinforced that BofA’s risk-reward profile is built on durability rather than excitement.

At around $50–51 post-earnings, shares sit close to their $51 fair value, leaving modest upside but strong downside support. For long-term investors comfortable with financial-cycle volatility, BofA remains a hold with opportunistic accumulation on dips below $48.

Call to Action

If you find this style of earnings-driven, valuation-based analysis helpful, follow SWOTstock for more breakdowns across banks, tech, and industrials—always grounded in official filings and management commentary.

Disclaimer

This article is for informational and educational purposes only. It does not constitute investment advice or a recommendation to buy or sell any securities. All analysis is based solely on Bank of America’s official Q3 2025 financial results and publicly available management commentary. Investors should conduct their own research or consult a licensed advisor before making investment decisions.

Berkshire Hathaway revealed a US $4.3 billion investment in Alphabet Inc. during Q3 2025, buying approximately 17.8 million shares. This strategic move occurred as Alphabet achieved its first US $100 billion revenue quarter. Berkshire’s purchase reflects a value-focused approach amid a tech market rotation, emphasizing Alphabet’s solid fundamentals and growth potential.

Berkshire Hathaway has disclosed a new US $4.3 billion position in Alphabet Inc. (GOOGL), confirming that Warren Buffett’s conglomerate entered the stock during the third quarter of 2025 — the same period in which Alphabet reported its first-ever US $100 billion revenue quarter.

According to Berkshire’s latest 13-F filing, the company purchased roughly 17.8 million shares of Alphabet, making it one of Berkshire’s ten largest equity holdings. The move surprised market watchers who have long associated Berkshire’s tech exposure primarily with Apple, which the firm trimmed in the same quarter.

A Contrarian Entry at a Trillion-Dollar Scale

Berkshire’s timing stands out. Alphabet shares were trading around US $270 – 280 during Q3 2025 — only modestly above their estimated intrinsic value range. While other institutional investors were rotating out of mega-cap tech after two years of outperformance, Berkshire appears to have treated Alphabet as a value compounder rather than a momentum play.

For Buffett followers, the purchase echoes a familiar pattern: buying into a cash-rich franchise once its growth narrative collides with valuation discipline. Alphabet fits that mold neatly — a business generating more than US $80 billion in free cash flow annually, returning US $15 billion in quarterly buybacks, and maintaining over US $100 billion in cash reserves.

Fundamentals Back the Move

Alphabet’s Q3 2025 report, released October 29, underscored that growth and prudence can coexist in Big Tech.

Revenue: US $102.3 billion (+16 % YoY)

Operating Income: US $31.7 billion (+23 %)

EPS: US $2.87

Google Cloud: +34 % YoY, margin rising to 9 %

CapEx: Raised to US $91 – 93 billion for AI data-center expansion

CEO Sundar Pichai described the period as “a reflection of how AI is transforming every corner of our business,” while CFO Ruth Porat stressed “disciplined long-term investment.”

Those remarks align closely with Buffett’s own playbook — durable cash flow, reinvestment discipline, and capital allocation guided by intrinsic value rather than quarterly optics.

Reinforcing the “Still Underpriced” Thesis

Our prior SWOTstock analysis of Alphabet’s Q3 results placed fair value near US $284 per share, with the market trading just above that level post-earnings. Berkshire’s purchase suggests that even at these prices, long-term investors still see a margin of safety — particularly as Alphabet’s AI infrastructure spending begins to translate into productivity and monetization gains across Search, YouTube, and Cloud.

For value-oriented readers, the implication is clear: when Berkshire buys into a trillion-dollar tech name after a record quarter, it’s not chasing growth — it’s buying durability.

Market Reaction

The disclosure briefly lifted Alphabet shares in after-hours trading on Friday, as investors digested the significance of Berkshire’s first new mega-cap tech stake in years. Analysts now expect fresh comparisons between Alphabet’s AI capital discipline and Apple’s maturing growth profile, which Berkshire has been gradually reducing.

As of mid-November 2025, Alphabet trades around US $277, giving the stake a paper value near its initial cost — a rare instance where Buffett’s patience and Alphabet’s execution appear perfectly aligned.

Disclosure: This article is based on public filings and Alphabet’s official Q3 2025 financial results. It does not constitute investment advice.