Berkshire Hathaway revealed a US $4.3 billion investment in Alphabet Inc. during Q3 2025, buying approximately 17.8 million shares. This strategic move occurred as Alphabet achieved its first US $100 billion revenue quarter. Berkshire’s purchase reflects a value-focused approach amid a tech market rotation, emphasizing Alphabet’s solid fundamentals and growth potential.

Berkshire Hathaway has disclosed a new US $4.3 billion position in Alphabet Inc. (GOOGL), confirming that Warren Buffett’s conglomerate entered the stock during the third quarter of 2025 — the same period in which Alphabet reported its first-ever US $100 billion revenue quarter.

According to Berkshire’s latest 13-F filing, the company purchased roughly 17.8 million shares of Alphabet, making it one of Berkshire’s ten largest equity holdings. The move surprised market watchers who have long associated Berkshire’s tech exposure primarily with Apple, which the firm trimmed in the same quarter.

A Contrarian Entry at a Trillion-Dollar Scale

Berkshire’s timing stands out. Alphabet shares were trading around US $270 – 280 during Q3 2025 — only modestly above their estimated intrinsic value range. While other institutional investors were rotating out of mega-cap tech after two years of outperformance, Berkshire appears to have treated Alphabet as a value compounder rather than a momentum play.

For Buffett followers, the purchase echoes a familiar pattern: buying into a cash-rich franchise once its growth narrative collides with valuation discipline. Alphabet fits that mold neatly — a business generating more than US $80 billion in free cash flow annually, returning US $15 billion in quarterly buybacks, and maintaining over US $100 billion in cash reserves.

Fundamentals Back the Move

Alphabet’s Q3 2025 report, released October 29, underscored that growth and prudence can coexist in Big Tech.

Revenue: US $102.3 billion (+16 % YoY)

Operating Income: US $31.7 billion (+23 %)

EPS: US $2.87

Google Cloud: +34 % YoY, margin rising to 9 %

CapEx: Raised to US $91 – 93 billion for AI data-center expansion

CEO Sundar Pichai described the period as “a reflection of how AI is transforming every corner of our business,” while CFO Ruth Porat stressed “disciplined long-term investment.”

Those remarks align closely with Buffett’s own playbook — durable cash flow, reinvestment discipline, and capital allocation guided by intrinsic value rather than quarterly optics.

Reinforcing the “Still Underpriced” Thesis

Our prior SWOTstock analysis of Alphabet’s Q3 results placed fair value near US $284 per share, with the market trading just above that level post-earnings. Berkshire’s purchase suggests that even at these prices, long-term investors still see a margin of safety — particularly as Alphabet’s AI infrastructure spending begins to translate into productivity and monetization gains across Search, YouTube, and Cloud.

For value-oriented readers, the implication is clear: when Berkshire buys into a trillion-dollar tech name after a record quarter, it’s not chasing growth — it’s buying durability.

Market Reaction

The disclosure briefly lifted Alphabet shares in after-hours trading on Friday, as investors digested the significance of Berkshire’s first new mega-cap tech stake in years. Analysts now expect fresh comparisons between Alphabet’s AI capital discipline and Apple’s maturing growth profile, which Berkshire has been gradually reducing.

As of mid-November 2025, Alphabet trades around US $277, giving the stake a paper value near its initial cost — a rare instance where Buffett’s patience and Alphabet’s execution appear perfectly aligned.

Disclosure: This article is based on public filings and Alphabet’s official Q3 2025 financial results. It does not constitute investment advice.

Alphabet (GOOGL) achieved over $100 billion in quarterly revenue for the first time, showing 16% year-over-year growth. Key drivers include a strong Cloud business and effective YouTube monetization. Despite CapEx concerns, the company remains cash-rich, positioning itself for long-term growth in AI and other sectors, recommending a hold strategy.

TL;DR Summary

Alphabet (GOOGL:NASDAQ) just passed the $100 billion quarterly revenue mark for the first time — growing 16 % year over year with broad strength across Search, YouTube, and Cloud. Despite record profits, the stock still trades near fair value, offering patient investors a long-term compounding story powered by disciplined AI execution.

Q3 2025 Financial Highlights

Revenue: $102.3 B (+16 % YoY)

Operating Income: $31.7 B (+23 %)

EPS: $2.87 (diluted)

Google Cloud: $15.2 B (+34 %), operating margin 9 % (up from 5 %)

CapEx: Guidance raised to $91–93 B (from $85 B) to expand AI infrastructure

Management Commentary — The AI Era at Work

CEO Sundar Pichai described the quarter as “a reflection of how AI is transforming every corner of our business.” He highlighted how Gemini models are now woven across Search, Workspace, and Android, while Google Cloud has become “a foundation for the next wave of AI applications.”

Pichai also drew attention to Waymo’s momentum, noting tens of thousands of fully autonomous rides weekly — a reminder that Alphabet’s portfolio still holds long-term optionality beyond advertising. CFO Ruth Porat reiterated a focus on “disciplined investment” and sustainable capital returns, ensuring AI expansion doesn’t come at the expense of profitability.

Market Reaction

Shares rose roughly 6 % post-earnings to around $288, as investors applauded Alphabet’s combination of growth and cost control. Growth investors celebrated the $100 B milestone; value investors noticed something quieter but more powerful — free-cash-flow compounding and balance-sheet strength, with over $100 B in cash and a business model that still prints double-digit operating margins despite surging AI spend.

SWOT Analysis — What’s Driving and Challenging Alphabet

Strengths — The Engine Still Scales

Alphabet’s ability to integrate AI across core products has turned efficiency into a margin lever, driving a 23 % jump in operating income.

Cloud growth of +34 % confirms enterprise adoption of Google AI and Vertex AI, while YouTube continues to monetize Shorts effectively.

A balance sheet boasting $109 B in cash and $80 B in free cash flow gives management the flexibility to invest and repurchase shares without financial strain.

These elements together could support a 6 – 12 % upside in valuation, equivalent to +$16–32 per share, if current trends hold.

Weaknesses — Spending Before the Payoff

The biggest risk near term is CapEx intensity: management raised 2025 guidance to $91–93 B, pushing short-term margins down to 31 %.

Cloud infrastructure build-out and TPU chip development consume cash before incremental revenue arrives.

For value investors, this is the “patience tax” — reinvestment that depresses earnings temporarily but is critical to maintain AI leadership. Estimated drag: −6 to −10 % on near-term fair value.

Opportunities — Optionality Beyond Ads

The rollout of Gemini-powered experiences across Search and Workspace is still early. If user engagement and monetization scale as expected, Alphabet could open entirely new revenue lines within existing products.

Waymo’s commercialization offers an overlooked lever: as autonomous rides expand to new cities, the segment could evolve from cost center to strategic asset.

Together, these trends imply +8 to +15 % potential uplift as new businesses begin contributing meaningfully.

Threats — The Unseen Headwinds

Alphabet faces regulatory pressure in the U.S. and EU that could reshape how it structures Search partnerships.

Rising AI training costs and limited chip supply could inflate unit economics in 2026.

Global digital tax initiatives also threaten to trim net margins.

These could shave 10 – 18 % off valuation in a downside scenario.

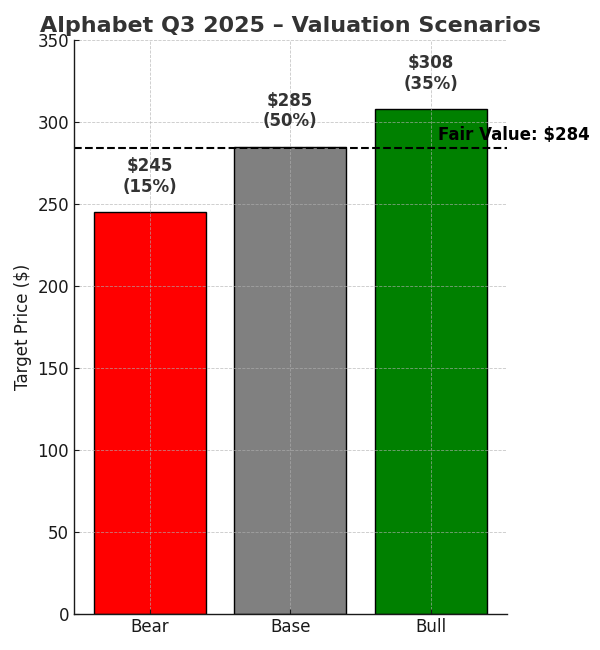

Valuation Scenarios — Fair Value Still Around $284

Bull Case (35 % probability) If Gemini monetization accelerates and Cloud margins surpass 10 %, EPS could reach $14 in FY 2026. At 22× earnings, that implies a $308 target — driven by full AI adoption and modest multiple expansion.

Base Case (50 % probability) A more realistic view assumes 12 % revenue growth and modest margin recovery. With EPS near $13 and 20× multiple, fair value sits at $285 — consistent with steady compounding and disciplined reinvestment.

Bear Case (15 % probability) If regulatory constraints slow Search deals or AI costs balloon, EPS might stall around $12. Applying 17× multiple yields $245 per share. Even here, Alphabet remains profitable and cash-rich, limiting true downside risk.

Weighted Fair Value: ≈ $284/share — almost identical to where the stock trades now (~$288). For long-term holders, that suggests limited short-term upside but strong margin of safety given cash reserves and buyback velocity.

Verdict — Hold, Accumulate Below $270

Alphabet remains a quiet compounding engine: dominant in AI infrastructure, prudent in spending, and generous in shareholder returns. At $288, the stock sits near intrinsic value. But below $270, its 3.5 % free-cash-flow yield and recurring revenue make it a compelling long-term hold for patient investors.

For value investors, the strategy is clear: own quality, wait through the CapEx cycle, and let compounding do the work.

Returns from AI infrastructure CapEx and Waymo expansion

Call to Action

Follow SWOTstock for clear, fundamentals-based coverage of high-cash-flow AI compounders like Alphabet, Microsoft, and Amazon. Subscribe to receive new posts right after each earnings call.

Disclaimer

This analysis is based solely on Alphabet Inc. official Q3 2025 financial report and earnings call transcript. It is not investment advice. Please conduct independent research before investing.

One response to “💡 Alphabet Q3 2025 Earnings — A $100 B Quarter that Still Feels Underpriced”

McDonald’s Q1 2025 earnings revealed a mixed performance, with total revenue at $5.96 billion, down 2% year-over-year. U.S. sales fell 3.6%, but global sales rose 1.9%. While profitability remained stable with EPS at $2.66, investor concerns over U.S. weakness led to a 1.9% stock decline. Analysts suggest the stock may be overpriced.

McDonald’s (NYSE: MCD) just released its earnings for the first quarter of 2025 on May 1, 2025, and the market had a mixed reaction. While global growth remained steady, softness in the U.S. weighed on investor sentiment. In this post, we’ll break down what happened this quarter, summarize the key highlights, provide a structured SWOT analysis, and assess whether the current stock price is justified—or a bit ahead of itself.

Q1 2025 Recap: A Mixed Meal

McDonald’s reported total revenue of $5.96 billion, down 2% year-over-year, falling short of expectations. The main drag? U.S. comparable sales declined 3.6%, driven by reduced traffic among low-income consumers. This came as a surprise, especially given the resilience shown in prior quarters.

On the bright side, global comparable sales rose 1.9%, with particularly strong performance in International Developmental Licensed Markets. The company’s digital flywheel continues to expand, now boasting over 170 million 90-day active users and generating $30 billion in annual systemwide sales.

Profitability held steady. EPS came in at $2.66, flat compared to last year, and the company maintained its full-year guidance, signaling long-term confidence.

Still, investors punished the stock on release day, driving it down by –1.9%, reflecting concern about core market softness.

Quarter Summary – Key Highlights

Revenue: $5.96B (–2% YoY), below consensus

EPS: $2.66 (flat YoY)

U.S. Comparable Sales: –3.6% (unexpected contraction)

Global Comparable Sales: +1.9%

Digital Engagement: 170M+ active loyalty users; $30B in system sales

Store Growth: Targeting 2,200 new units globally in 2025

SWOT Analysis with Quantitative Stock Price Impact

Now that we’ve covered the surface, let’s dive deeper. A SWOT analysis gives us a structured way to assess the quarter’s real implications—including how each element likely impacted the stock price.

Strengths

McDonald’s international operations continue to deliver. The 1.9% global comparable sales growth helped soften the blow from weak U.S. performance. In addition, the company’s digital ecosystem is a major asset. With 170M+ loyalty users contributing to $30B in sales, this customer retention engine is likely to support long-term revenue stability.

Stock impact: These strengths contributed to a +1.0% to +1.7% positive pressure on the stock price.

Weaknesses

The glaring weakness this quarter was the –3.6% decline in U.S. comparable sales, reflecting a pullback in visits from lower-income consumers. Management acknowledged that value offerings weren’t enough to fully retain traffic. Flat EPS ($2.66) also showed that margin strength couldn’t offset volume weakness.

Stock impact: Weaknesses contributed to a –1.8% to –2.7% downward adjustment.

Opportunities

McDonald’s sees opportunity in its global expansion plans, with 2,200 new store openings planned this year (including 1,000 in China). Value menu strategies, like a €4 Happy Meal in Germany, are also being deployed to retain budget-conscious customers.

Stock impact: These growth signals added +0.5% to +1.0% upside potential.

Threats

Consumer sensitivity to inflation, especially among low-income groups, poses a real threat to short-term performance. Additionally, competitive pressure in Europe, especially the UK, remains elevated and was acknowledged by management on the call.

Stock impact: Threats exerted –0.7% to –1.2% negative pressure.

Net Stock Impact Estimate: Combining all elements, the stock saw a net estimated drop of –0.8% to –1.2%, which aligns closely with the actual decline of –1.9% post-earnings.

SWOT Summary

SWOT Analysis – Q1 2025

Strengths

• Digital loyalty program scaling globally

• $30B in digital systemwide sales

• Global comparable sales +1.9%

• Stock impact: +1.0% to +1.7%

Weaknesses

• U.S. comparable sales –3.6%

• Soft traffic among low-income groups

• Flat EPS YoY

• Stock impact: –1.8% to –2.7%

Opportunities

• 2,200 store openings in 2025

• Strong growth in China

• Value-based pricing in Europe

• Stock impact: +0.5% to +1.0%

Threats

• Rising price sensitivity

• Competitive pressure in key markets

• Inflation could impact margin recovery

• Stock impact: –0.7% to –1.2%

Base, Bull, and Bear Cases

Let’s now examine where McDonald’s stock could go from here, using base, bull, and bear cases based on the earnings report.

Scenario

Narrative

Stock Price Estimate

Probability

Base Case

Balanced view: EPS flat, U.S. weak, digital stable

$310.67 (–1.2%)

60%

Bull Case

Focus on digital loyalty, global expansion offsets U.S. drag

$317.56 (+1.0%)

25%

Bear Case

Market reacts strongly to U.S. weakness and low-income trends

With the actual current price at $308.42 (May 2, 2025), the market is leaning more pessimistic than our weighted scenario suggests.

Valuation: Is the Stock Fairly Priced?

McDonald’s is currently trading at a P/E ratio of ~27.15×, which is slightly above its 5-year historical range of 23×–26×. With no earnings growth and U.S. comps turning negative, the fundamentals suggest that a 25× multiple is more appropriate, implying a fair value around $284.

Metric

Value

Current Price

$308.42

Fair Value (Base Case)

$284

Premium to Fair Value

+8.6%

Verdict

Overpriced by ~8–10%

Final Take

McDonald’s remains a strong global brand with a powerful digital strategy, but the U.S. consumer softness and flat profitability raise questions about near-term growth. While long-term investors may look past these issues, at today’s price, the stock appears to be slightly overpriced relative to its fundamentals.

If you’re holding, stay patient—but if you’re considering buying, it may be worth waiting for a better entry point.

Comment on Source Usage: This analysis is based exclusively on McDonald’s official Q1 2025 financial report and the corresponding earnings call transcript. No third-party news articles, analyst opinions, or external data sources were referenced. This approach ensures the insights presented reflect only the company’s own disclosures and strategic messaging.

Disclaimer: This content is for informational purposes only and does not constitute financial advice, investment recommendations, or an endorsement to buy or sell any securities. Readers should conduct their own research or consult a qualified financial advisor before making investment decisions.

Please subscribe to our blog for the latest analysis. If you want a detailed full analysis report, please leave a comment.

Leave a comment