Oracle and Adobe both beat earnings expectations, but their stocks moved in opposite directions. Discover why Oracle soared while Adobe slipped—and what it reveals about investor confidence in AI execution vs. hype.

Two enterprise tech giants—Oracle and Adobe—both reported strong quarterly results this past week. Each beat Wall Street expectations and highlighted their advancements in artificial intelligence. But the stock market reaction couldn’t have been more different:

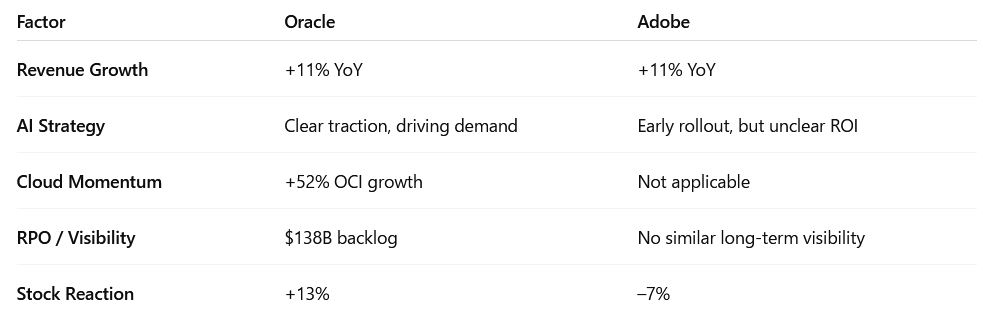

Oracle stock surged +13%

Adobe stock declined –7%

At SWOTstock, we examined the earnings reports, management commentary, and investor sentiment. What we found illustrates a growing gap in how the market values AI strategy: it’s not about who talks the loudest—it’s about who delivers results.

Oracle: AI Execution Drives Confidence and Capital

Oracle’s Q4 FY2025 earnings confirmed the company’s transformation from legacy enterprise vendor to cloud-first AI infrastructure provider. Revenue climbed 11% YoY, while Oracle Cloud Infrastructure (OCI) accelerated an impressive 52%.

What truly stood out was Oracle’s $138 billion in remaining performance obligations (RPO), offering investors forward-looking visibility. With high-profile partnerships (NVIDIA, Cohere) and GenAI workloads already in production, Oracle isn’t pitching an AI future—it’s reporting on AI present.

SWOTstock Takeaway Oracle’s strength lies in its ability to turn AI demand into revenue now—not years from now.

Key Strengths:

Cloud Infrastructure (OCI) grew +52% YoY

AI partnerships with NVIDIA and Cohere are already monetizing

$138B RPO provides long-term visibility and stability

Risks to Watch:

Continued competition from AWS, Microsoft, and Google

Legacy on-premise business still weighs on blended growth

Adobe: Solid Results, But Investors Want AI ROI

Adobe’s Q2 FY2025 results were strong on the surface: 11% revenue growth, earnings beat, and raised guidance. Yet investors responded with skepticism, sending the stock down 7%.

The issue? Despite promoting new AI tools like Firefly, GenStudio, and Acrobat AI, Adobe has yet to show how these innovations will contribute meaningful revenue in the short term. Investor patience is wearing thin.

Meanwhile, competition is heating up. Canva is gaining ground in design, while OpenAI and Google are introducing productivity tools that threaten Adobe’s document business. In this environment, a premium pricing model without clear AI-driven ARR growth becomes difficult to defend.

SWOTstock Takeaway Adobe’s innovation story is still credible, but without visible monetization, the stock is vulnerable.

Key Strengths:

Industry-leading suite across Creative, Document, and Experience Cloud

Rapid rollout of AI-powered features

Risks to Watch:

No clear monetization path from AI features

Growing threats from Canva, OpenAI, and Google

Pressure on margins and customer retention

Why the Divergence?

Despite similar top-line growth, the market saw Oracle and Adobe very differently:

Oracle showed the market what execution looks like. Adobe reminded investors that potential alone is no longer enough.

What to Watch in the Next 6–12 Months

🔮 Oracle Outlook: Expect continued strength if cloud growth persists and GenAI partnerships scale. RPO offers downside protection in case of macro softness.

⚠️ Adobe Outlook: Needs to prove that AI tools are driving ARR and enterprise wins. Without that, competitive pressures may accelerate valuation compression.

Final Thoughts: AI Is Entering the Show-Me Phase

This earnings season proves that we’re past the AI hype cycle. The market is now demanding proof—measurable, monetizable traction.

At SWOTstock, we’ll keep tracking this shift as it plays out in earnings calls, product roadmaps, and valuation resets.

👉 Follow us for AI-enhanced stock insights built for growth-minded and DIY value investors.

⚠️ Disclaimer

This analysis is based on publicly available company financials, earnings call commentary, and official press releases as of June 2025. It is intended for informational purposes only and does not constitute investment advice. Always perform your own due diligence.

Salesforce Q1 FY26 earnings: strong cash flow, $1B+ AI revenue, and raised guidance—but the stock dipped. Discover our in-depth SWOT analysis, valuation scenarios, and why long-term tech investors may see upside.

🚀 TL;DR – Earnings Solid, Outlook Raised, But Street Unconvinced

Salesforce (NYSE: CRM) delivered on many fronts in Q1 FY26: strong free cash flow, a raised full-year outlook, and impressive AI momentum with over $1B in annualized AI revenue. Yet the market reaction was subdued. Shares slipped ~3% post-earnings as investors weighed modest growth against growing acquisition dependency. For long-term investors focused on enterprise AI, the current pullback may offer an attractive re-entry point — but execution risk remains high.

Salesforce reported Q1 FY26 revenue of $9.8 billion, reflecting 8% growth year-over-year. The company continues to demonstrate financial discipline, posting a 32.3% non-GAAP operating margin and generating $6.3 billion in free cash flow — a key metric that reinforces the strength of its subscription-based business model.

However, the earnings story wasn’t just about operational metrics. Management spent considerable time during the call highlighting Salesforce’s evolving identity as an AI-first enterprise software provider. The AI and Data Cloud segment reached a milestone of over $1 billion in annualized recurring revenue, up 120% from the prior year. Additionally, Agentforce — the company’s AI-powered sales assistant platform — closed over 8,000 deals, with 50% of them already monetized.

Despite these advancements, investor enthusiasm appeared tempered. Salesforce also unveiled its intention to acquire Informatica in a transaction valued at over $8 billion. While the strategic rationale centered on data integration and platform expansion, some investors viewed it as a sign that organic AI monetization remains in its early innings.

📌 Key Highlights

(📌 Visual Placeholder: Q1 FY26 Metrics Snapshot)

Revenue: $9.8B (+8% YoY)

Subscription & Support Revenue: $9.3B (+8% YoY)

Non-GAAP Operating Margin: 32.3%

Free Cash Flow: $6.3B (+4% YoY)

AI & Data Cloud ARR: $1B+ (+120% YoY)

Agentforce Deals: 8,000+ closed, 50% paid

Shareholder Return: $3.1B (including $2.7B in buybacks)

FY26 Guidance: Revenue raised to $41–41.3B, EPS to $11.27–11.33

🧠 SWOT Analysis – Is Salesforce Building Sustainable AI Moats?

To evaluate Salesforce’s trajectory, we use a SWOT framework — layering qualitative insight with quantitative impact ranges to assess where the stock could go next.

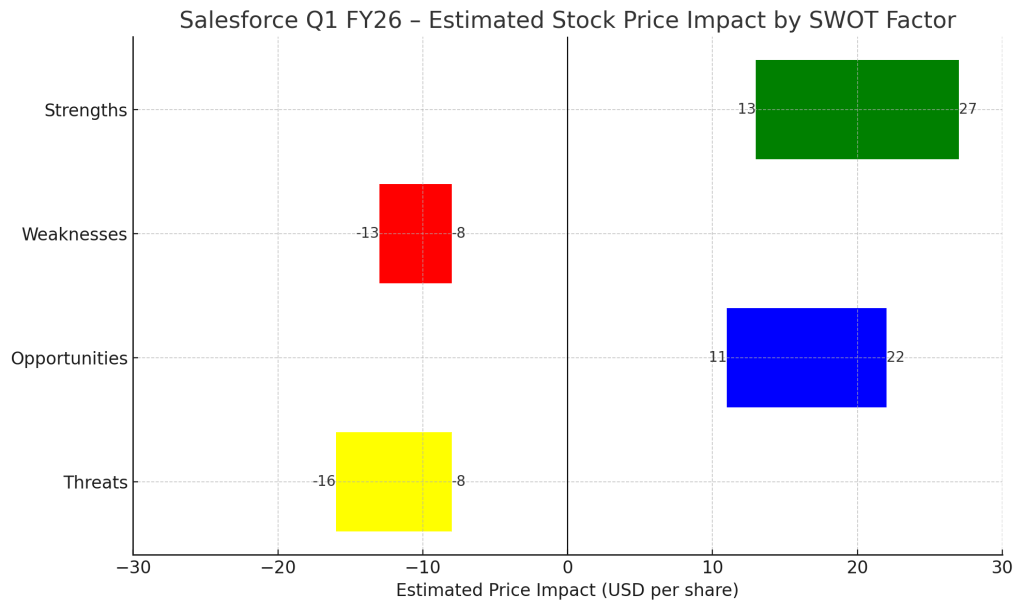

✅ Strengths

Salesforce’s high-margin business continues to generate substantial cash, supporting both R&D and shareholder returns. With a 32.3% non-GAAP operating margin and $6.3B in quarterly free cash flow, the company remains financially resilient. Meanwhile, the $1B+ in AI annual recurring revenue — up 120% year-over-year — signals that the firm’s early bets on generative AI are beginning to materialize.

Estimated Price Impact: +5% to +10% ($13–27)

⚠️ Weaknesses

At 8% year-over-year growth, revenue is expanding — but not at a pace that excites growth-focused investors. Combined with an $8B acquisition of Informatica, some view the quarter as a reminder that Salesforce still leans heavily on M&A for platform expansion. This can dilute long-term returns if integration is poorly executed or if synergy realization takes longer than anticipated.

Estimated Price Impact: –3% to –5% ($8–13)

🌱 Opportunities

The most obvious upside lies in the scaling of Agentforce and global AI deployment. Management noted that over 8,000 Agentforce deals were signed, with paid conversion already at 50%. On top of that, international expansion — particularly in Japan, the UK, and Canada — could provide incremental growth via cross-product bundling and new verticals.

Estimated Price Impact: +4% to +8% ($11–22)

🧨 Threats

Salesforce is not immune to macroeconomic uncertainty. Should enterprise IT budgets tighten further, even AI-led offerings could face delayed adoption. Add to that the integration risk tied to Informatica, and the bear case begins to take shape. Investors have seen how difficult it can be to maintain focus and cost discipline amid large-scale acquisitions.

Estimated Price Impact: –3% to –6% ($8–16)

📋 SWOT Summary Table

📐 Valuation Scenarios – Realistic Upside, But No Easy Wins

🟢 Bull Case – Target: $320 (Probability: 30%)

A best-case scenario assumes Salesforce executes flawlessly: Agentforce expands rapidly, international AI rollouts outperform, and Informatica is integrated smoothly. In this case, margin expansion and top-line acceleration could support a price of $320.

⚫ Base Case – Target: $290 (Probability: 50%)

In a more measured scenario, AI and cloud revenue continue to build gradually while macro headwinds and integration friction create a modest drag. Here, the valuation rests on steady execution — not breakout success.

🔴 Bear Case – Target: $260 (Probability: 20%)

The bear case includes a slower-than-expected AI ramp, growing customer budget constraints, and post-acquisition inefficiencies. Margins may hold, but revenue growth could fall short.

Weighted Fair Value:

(0.3 × $320) + (0.5 × $290) + (0.2 × $260) = $293

🔍 Peer Comparison – Where Salesforce Stands in the AI-Enterprise Cloud Race

While Salesforce has made impressive strides in monetizing AI, investors are right to compare its positioning against other enterprise software giants. Let’s take a closer look at how Salesforce stacks up against Microsoft and ServiceNow — two of the most visible players in enterprise AI and workflow automation.

Microsoft (MSFT) remains the dominant force in cloud infrastructure and productivity software, with its AI integration deeply embedded in products like Office 365, Azure OpenAI, and Dynamics. Although Microsoft has been less transparent about standalone AI ARR, its cross-product integration strategy has kept it at the forefront of enterprise adoption. Its advantage lies in seamless native integration — rather than monetizing AI as a separate revenue line, it’s baking it into everything.

ServiceNow (NOW), on the other hand, is pursuing a focused strategy in workflow automation with GenAI capabilities tied to task orchestration, IT operations, and HR service delivery. While it doesn’t disclose AI revenue explicitly, estimates suggest significant uptake across modules, especially post its strategic partnerships with NVIDIA and Microsoft. Its modular SaaS structure allows for more agile, vertical-specific AI adoption.

Salesforce (CRM) is unique in that it publicly discloses AI ARR, which recently crossed the $1B threshold (up 120% YoY). This offers greater transparency — a potential edge with analysts and investors — but also sets higher expectations. Salesforce’s AI strategy is tied closely to its Data Cloud and the Agentforce platform, but the question remains whether it can scale these innovations organically or will rely on acquisitions like Informatica to accelerate adoption.

Overall, Salesforce appears to be ahead in AI monetization transparency, but trails in seamlessness of integration (vs. Microsoft) and vertical execution (vs. ServiceNow). The coming quarters will be critical in demonstrating that these early AI wins are scalable — not just showcase projects.

🧭 Verdict – AI Execution Will Make or Break This Re-Rating

At ~$267, Salesforce is trading about 9% below its probability-weighted fair value of $293. That’s not a deep discount — but for investors willing to wait on Agentforce and international AI scaling, it may represent a reasonable opportunity.

Still, this is not a momentum trade. Salesforce must show it can deliver consistent AI-driven revenue growth without leaning too heavily on M&A to do it.

📩 Call to Action

Follow @SWOTstock and subscribe to get clear, no-spin earnings breakdowns.

⚠️ Disclaimer

This article is based solely on Salesforce’s official Q1 FY26 earnings report and management’s public comments. It is not investment advice.

Leave a comment