ASML posted a solid Q3 with €7.5 billion in sales and €2.1 billion in net income, leading to a positive stock reaction. Despite a projected decline in Chinese demand for 2026, management remains optimistic, maintaining a fair valuation of approximately $1,190 per share, indicating significant growth potential driven by AI advancements.

🔎 TL;DR Summary

ASML (AMSL:NASDAQ) just delivered another steady quarter: €7.5 billion in sales, €2.1 billion net income, and margins holding above 51 %. The stock reacted positively in pre-market, climbing ~3 %, as investors looked beyond a cautious China outlook to renewed confidence in ASML’s long-term AI-driven roadmap. Our fair-value model points to ~ $1,190 per share, ≈ 25 % upside.

🧭 Quarter Recap

Management called Q3 “in line with guidance.” Bookings hit €5.4 billion, supported by continued momentum in EUV and early shipments of High-NA EUV systems. The company also highlighted its new AI partnership with Mistral AI, aiming to embed machine-learning control into yield and productivity.

The only dark cloud: ASML expects a “significant decline in China demand in 2026.” Still, management does not foresee overall sales falling below 2025 levels — a sign of resilience amid geopolitical shifts.

💡 Key Highlights

Net sales: €7.52 billion | Gross margin: 51.6 %

Net income: €2.13 billion | EPS: €5.49

Bookings: €5.4 billion | Service revenue: €1.96 billion

ASML Q3 2025 Valuation Scenarios: Target prices under Bear, Base, and Bull cases.

🧠 Verdict

ASML remains the “picks-and-shovels” play for the AI era. Even as near-term demand wobbles, its EUV and High-NA roadmap locks in a multi-year growth path few companies can match. For tech-savvy growth investors, the setup still favours accumulation on dips.

💬 Investor Takeaway

Market reaction shows confidence in ASML’s long-term story: from chipmaker orders to AI co-design tools, it continues to define the semiconductor future. Short-term noise aside, the firm’s monopoly position and AI-linked flywheel justify a premium valuation — and our $1,190 fair price reflects that potential.

Disclaimer: This post is for informational purposes only and not financial advice. Please do your own research before investing.

The article discusses the rising importance of edge AI in enterprise technology, emphasizing its role in reducing latency, enhancing privacy, and optimizing costs. Accenture is positioned well to capitalize on this trend due to its strategic acquisitions and industry relationships. Potential valuation growth is estimated at around $378 per share by 2030, contingent on successful execution.

If you follow enterprise tech, you’ve probably noticed that “edge AI” has shifted from buzzword to board-level priority. Companies want AI that runs close to where data is created—on phones, sensors, cameras, factory lines, cars—so decisions happen in milliseconds, data stays private, and costs don’t balloon in the cloud. This article looks at where Accenture sits in that shift, how crowded the field has become, and what all of this could mean for the stock. I’ll keep the tone conversational and minimize bullet points, while still laying out a clear, investor-minded view with a fair-value estimate at the end.

Edge AI, briefly—why it matters now

Edge AI means running models locally on devices rather than shipping everything to cloud data centers. The benefits are straightforward: lower latency, better privacy, less bandwidth, and the ability to operate even when connectivity is spotty. Think of a security camera that flags anomalies on-device, a factory sensor that predicts failures in real time, or a car that fuses vision and language models to assist the driver without calling home.

Generative AI gets more headlines, but edge AI sits where operational value is created—on the shop floor, in vehicles, at retail, inside hospitals. The two are connected: many enterprises will pair cloud-scale GenAI with compact models running at the edge. Any services firm that can bridge that gap has a shot at premium work.

How Accenture has built its edge-AI muscle

Over the last couple of years Accenture has been stitching together a mix of consulting depth and hands-on engineering. It acquired silicon design firms (Excelmax and Cientra), invested in a model-compression startup (CLIKA), and trained a very large portion of its workforce in AI practices. That combination lets the company talk strategy with the C-suite, design and test solutions with embedded systems teams, and then scale deployments across dozens of plants or thousands of devices. Few consultancies can credibly do all three.

Just as important, Accenture already sits inside the industries where edge AI is landing first: manufacturing, automotive, telecom, healthcare, energy. Those client relationships, plus a broad partner web with chipmakers and cloud providers, position the company to win repeat work as pilots graduate to rollouts.

The competitive reality

This is not an empty field. On the platform and hardware side, NVIDIA, Qualcomm, Intel, Apple and others drive silicon and software stacks; hyperscalers offer toolchains that extend to the edge; consulting rivals like IBM and Capgemini bring strong engineering pedigrees; Deloitte and McKinsey remain influential with boards and regulators. In a crowded landscape, Accenture’s edge is less about owning a platform and more about orchestrating outcomes—choosing the right models and hardware, compressing them to fit, integrating with legacy systems, and running change management at enterprise scale.

SWOT analysis with price impacts

Accenture’s strengths in edge AI are unusually tangible for a services firm. The chip-design acquisitions and the investment in model optimization give it a way to reduce the “last mile” friction that often kills edge projects: getting models small, fast, and reliable on constrained devices. Coupled with its global delivery network, that capability can add real growth optionality. In valuation terms, I see those strengths supporting roughly +5% to +8% upside versus a no-edge-AI baseline, because investors tend to pay up for firms that can both advise and execute.

Weaknesses are more prosaic but matter. Accenture does not sell chips or devices, so it relies on partners for the building blocks. And because the company is already very large, even successful edge programs may represent a modest slice of overall revenue for a while. Those factors can dampen the multiple and shave –2% to –4% from what otherwise looks like an AI-premium narrative.

Opportunities are where things get interesting. Edge AI spending is compounding as factories modernize, cars become rolling computers, and hospitals instrument workflows. Accenture can bundle cloud GenAI and on-device intelligence into “reinvention” programs that attack cost, speed, and safety at once. If execution matches the pipeline, that story can support another +7% to +12% of valuation tailwind as investors price in higher growth durability.

Threats are real and mostly competitive. If hardware vendors and hyperscalers push turnkey offerings faster than expected, services can look more like commodity integration. If clients deploy more slowly, or if ROI takes longer to prove in regulated industries, momentum can stall. Put a –3% to –6% drag on valuation for those risks and you have a balanced, but still favorable, tilt.

Scenarios and fair value (illustrative)

Because Accenture doesn’t break out “edge AI revenue” as a line item, we model the impact at the level investors actually trade on: earnings power and the multiple the market is willing to pay. To keep this grounded, I anchor on reasonable ranges for EPS growth and P/E by 2030, then weigh the outcomes.

Bull case (40% probability). Edge programs scale alongside cloud GenAI work. AI-related revenue becomes a visible growth wedge, margins hold, and investors reward execution. If EPS reaches about $16 by 2030 and the market assigns a 28× multiple, you get an implied price near $448.

Base case (45%). Edge AI contributes meaningfully but remains under 10% of total revenue. Growth is steady, not explosive. With EPS around $14 and a 25× multiple, the implied price is about $350.

Bear case (15%). Adoption is slower, work skews toward integration, and the multiple compresses. With EPS near $12.5and a 22× multiple, the stock sketches to roughly $275.

Weighting those three paths yields a probability-weighted fair value of ~$378. It is not a moonshot number; it reflects confidence that Accenture will keep winning complex, multi-year AI programs where edge and cloud meet, without assuming platform-owner economics.

(Note: current share price fluctuates; the scenario math is illustrative rather than price-tick precise.)

What could change this view

Two things would push the needle higher. First, proof that model-compression and embedded engineering are shortening time-to-value on real deployments—think a global auto program or a multi-country factory network moving from pilot to standard with measurable savings. Second, clearer disclosure connecting AI bookings to revenue and margin expansion, so investors can track conversion rather than treating it as a narrative line.

On the downside, watch for customers delaying capital plans, hyperscalers tightening their grip on the edge toolchain, or a visible shift in project mix from “design and build” to lower-margin staff augmentation.

Bottom line

Edge AI isn’t a side show; it’s the place where AI meets the physical world. Accenture’s blend of consulting reach, embedded engineering from its acquisitions, and model-optimization capability puts it in a strong position to lead enterprise edge deployments. The field is busy and the company is already large, so don’t expect edge AI alone to redefine the business overnight. But as part of a broader AI reinvention engine, it can support healthier growth and a sturdier multiple. On the numbers above, that argues for a fair value around $378, with the bias skewed to the upside if execution stays crisp.

Disclosure & methodology: This article synthesizes public information on Accenture’s recent acquisitions and AI investments, industry reports on edge-AI adoption, and a scenario framework based on plausible EPS and P/E ranges through 2030. Accenture does not separately disclose edge-AI revenue, so assumptions are required; figures are illustrative, not precise forecasts. This is for education and discussion only and is not investment advice.

Morgan Stanley reported strong Q2 2025 results, with $16.8B revenue and $2.13 EPS, surpassing expectations. Wealth Management added $59B in assets, while trading revenues increased. Despite a 5% drop in investment banking fees, the firm raised its dividend and initiated a $20B buyback, reflecting ongoing shareholder commitment. Shares fell post-announcement amid market caution.

TL;DR Summary

Morgan Stanley delivered a strong Q2 2025, with $16.8 B revenue and EPS of $2.13, both above expectations. Wealth Management inflows of $59 B and robust trading performance offset a 5% decline in investment banking fees. The firm also raised its dividend to $1.00/share (yielding ~2.8%) and approved a $20 B share buyback, underscoring its commitment to returning capital. Despite these positives, shares slipped ~1–2% post‑earnings, reflecting cautious sentiment around capital markets headwinds. Our fair value estimate remains ~$144, near current levels, with upside tied to a revival in dealmaking and continued strength in Wealth Management.

Quarter Recap

Morgan Stanley reported net revenues of $16.8 B, up 12% YoY, and EPS of $2.13, beating consensus by 7.6%. ROTCE reached 18.2%, reaffirming the firm’s profitability strength.

Wealth Management added $59 B in net new assets, partially offset by $22 B in tax-related outflows. Trading was a bright spot: equities revenue came in at ~$3.7 B (+23% YoY) and fixed income at ~$2.2 B (+9%). These gains helped offset investment banking fees, which fell ~5% YoY and remain below pre‑2022 levels.

Capital returns were a highlight: the board approved a quarterly dividend increase to $1.00/share (yielding ~2.8% at current prices) and a $20 B share repurchase program, beginning in Q3 2025.

Key Highlights

Revenue: $16.8 B (+12% YoY)

EPS: $2.13 (+7.6% above consensus)

ROTCE: 18.2%

Wealth Management: $59 B net new assets, offset by $22 B in tax outflows

Trading: Equities $3.7 B (+23%); Fixed income $2.2 B (+9%)

Investment Banking: Down ~5% YoY; still lagging pre‑2022 levels

Capital Returns: Dividend raised to $1.00/share (~2.8% yield); $20 B buyback approved

Peer Comparison

Morgan Stanley’s steady, wealth-led approach continues to differentiate it. But when comparing to peers, Goldman Sachs grew investment banking revenue ~26% YoY, while Morgan Stanley saw a 5% decline. JPMorgan also outpaced MS in advisory and underwriting activity. This highlights a strategic trade‑off: Morgan Stanley prioritizes stable Wealth Management growth, sacrificing some upside in deal-driven businesses.

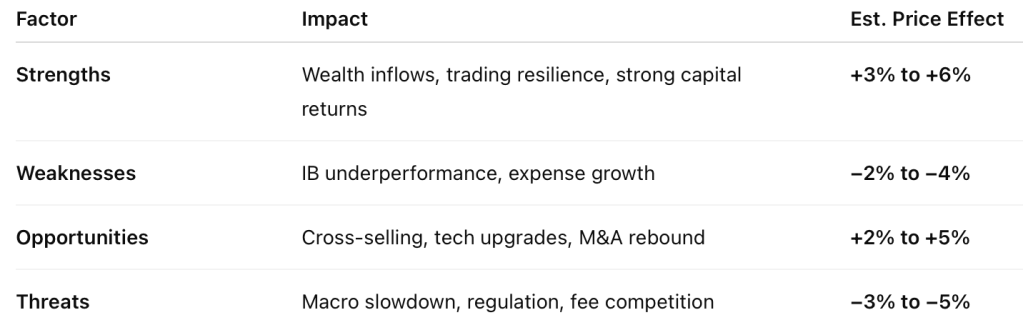

SWOT Analysis

Morgan Stanley’s Q2 shows why the market reacted cautiously: the firm delivered solid results, but investors remain concerned about weaker capital markets revenue and near-term growth visibility.

Strengths (+$4 to +$8):

Wealth inflows: $59 B new assets despite tax-related outflows

Trading strength: Equities +23%, Fixed Income +9% YoY

Capital returns: Dividend raised to $1/share (~2.8% yield) and $20 B buyback

Strong profitability: ROTCE at 18.2%, EPS beat of 7.6%

Weaknesses (−$3 to −$6):

Investment banking lag: −5% YoY vs Goldman’s +26%

Expense growth: Costs rising faster than some revenue lines

Client outflows: Tax outflows muted net inflow impact

Opportunities (+$3 to +$7):

Cross-selling E*TRADE clients within Wealth Management

Tech and AI investments to enhance operating leverage

Rebound in IPO/M&A could significantly lift investment banking revenues

Threats (−$4 to −$7):

Macro risks: Slowing economy could cut dealmaking & trading volumes

Regulatory pressures: Higher capital requirements could restrict buybacks

Competitive fee pressure: Margin erosion in Wealth Management & brokerage

Net SWOT price impact:−$7 to +$8 (implying short-term trading range between ~$136 and $151).

Fair value:~$144 Assessment:Fairly valued. Any upside depends on an M&A/IPO rebound and sustained asset growth in Wealth Management.

12‑Month Outlook

Looking ahead, Morgan Stanley’s fortunes will hinge on:

Capital markets recovery: IPO/M&A activity improving in 2026 could reaccelerate IB revenue.

Sustained Wealth inflows: Maintaining $50 B+/quarter will support fee growth and capital returns.

Regulatory clarity: New capital requirements could affect buyback pace.

Verdict

Morgan Stanley remains a defensive, shareholder-friendly play, with stable wealth-led earnings and enhanced capital returns. While near-term upside is capped by muted deal activity, long-term investors benefit from solid dividends, repurchases, and consistent profitability.

Call to Action

Are you bullish on Morgan Stanley’s wealth-first strategy? Drop your thoughts below, and subscribe for more SWOT-driven earnings breakdowns to help you invest smarter.

Disclaimer

This analysis is based solely on Morgan Stanley’s official Q2 2025 financial report and earnings call transcript. It is for informational purposes only and is not investment advice.

Leave a comment