TL;DR Summary

Berkshire Hathaway’s FY2025 results showed softer operating earnings and insurance volatility, yet the balance sheet has never been stronger. With over $370B in cash and disciplined capital allocation under Greg Abel, the long-term compounding story remains intact. However, at around $500 per BRK.B share, the stock appears close to fair value. For DIY value investors, the key question is no longer quality — it’s margin of safety.

Quarter Recap

Berkshire Hathaway reported FY2025 results in late February 2026. Operating earnings declined modestly year-over-year, reflecting weaker insurance underwriting and investment writedowns. GAAP net income was more volatile due to mark-to-market adjustments in the equity portfolio.

Despite softer earnings, Berkshire ended the year with a record cash position exceeding $370B. Share repurchases remained limited, and the company was a net seller of equities during much of the year.

This was also the first full annual report under CEO Greg Abel, marking a formal transition from the Buffett era while maintaining the same capital allocation philosophy.

Key Highlights

• Operating earnings declined modestly year-over-year

• Insurance underwriting results weakened in Q4

• Cash & equivalents reached record levels (~$370B+)

• No major acquisition deployed despite large liquidity

• Leadership transition to Greg Abel formally underway

• Equity portfolio remains concentrated in high-quality holdings

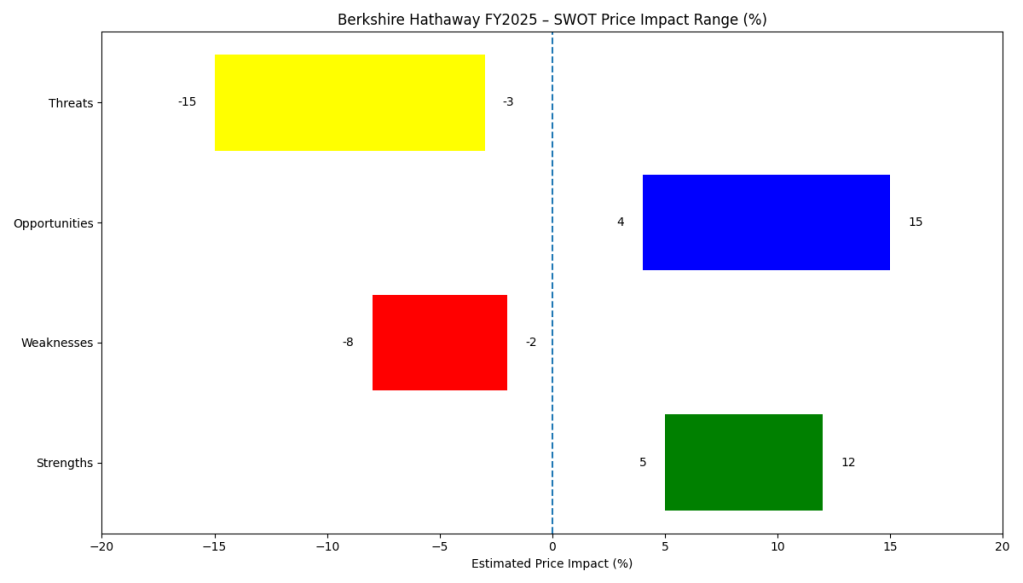

SWOT Analysis

Berkshire is not an earnings-momentum stock. It is a capital allocator built for long-term compounding. FY2025 did not break the story — but it did test investor patience. For value investors, durability matters more than quarterly growth.

Strengths

• Massive cash position providing downside protection and acquisition optionality

Estimated Price Impact: +5% to +12%

• Diversified operating businesses (insurance, rail, energy, manufacturing)

Estimated Price Impact: +4% to +8%

• Long-standing capital allocation discipline now reinforced under Abel

Estimated Price Impact: +3% to +7%

• High-quality equity portfolio generating dividends and embedded gains

Estimated Price Impact: +4% to +10%

Weaknesses

• Insurance earnings volatility and catastrophe exposure

Estimated Price Impact: -3% to -8%

• Slower organic growth relative to high-growth market leaders

Estimated Price Impact: -2% to -6%

• Leadership transition uncertainty in post-Buffett era

Estimated Price Impact: -3% to -7%

Opportunities

• Large-scale acquisition during market downturn

Estimated Price Impact: +8% to +15%

• Improvement in insurance pricing cycle

Estimated Price Impact: +4% to +9%

• Opportunistic share buybacks below intrinsic value

Estimated Price Impact: +5% to +10%

Threats

• Major insurance catastrophe event

Estimated Price Impact: -6% to -15%

• Significant equity portfolio drawdown

Estimated Price Impact: -5% to -12%

• Prolonged inability to deploy excess cash effectively

Estimated Price Impact: -3% to -8%

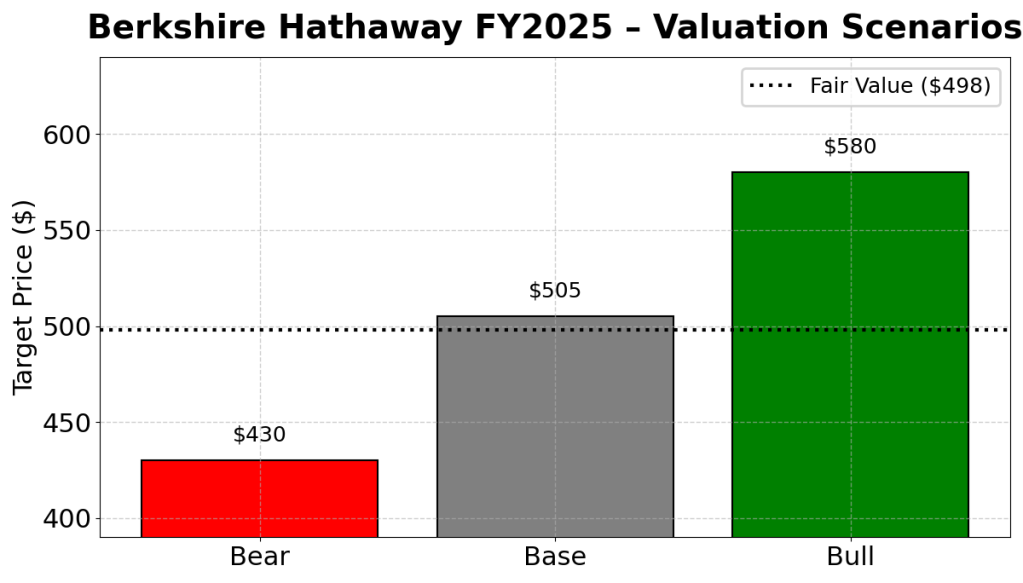

Valuation Scenarios (based on BRK.B)

Berkshire should be valued on normalized operating earnings rather than GAAP net income due to mark-to-market volatility. Using conservative assumptions aligned with Buffett-style valuation discipline:

Bear Case

Flat or declining operating earnings

14× earnings multiple

No major capital deployment

Implied Price Target: $430

Probability: 30%

Base Case

4–6% operating earnings growth

16× earnings multiple

Gradual capital deployment

Implied Price Target: $505

Probability: 50%

Bull Case

8–10% earnings growth

Successful large acquisition

18× earnings multiple

Implied Price Target: $580

Probability: 20%

Probability-Weighted Fair Value:

≈ $498

Verdict

Berkshire Hathaway remains one of the highest-quality capital allocators in the world. The balance sheet strength is extraordinary, and the business model remains durable.

However, at roughly $500 per BRK.B share, the stock trades close to intrinsic value under conservative assumptions. There is limited margin of safety unless earnings growth accelerates or a large acquisition creates incremental intrinsic value.

For DIY value investors, Berkshire is still a core compounding vehicle — but not a deep bargain today.

Call to Action

If you are building a long-term value portfolio, ask yourself:

Are you buying Berkshire for safety, or for upside?

Follow SWOTstock for structured, investor-focused earnings analysis grounded in intrinsic value logic — not headlines.

Disclaimer

This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consider their financial circumstances before making investment decisions.