TL;DR Summary

Citigroup (C:NYSE) delivered a strong quarter, with revenue up 14% and net income up 42%, showing real progress in its turnaround.

The stock responded positively — but at current levels, much of that improvement may already be priced in.

For value investors, Citi is no longer a deep discount. It’s now an execution story.

Quarter Recap

Citi’s Q1 2026 results were strong across the board, and importantly, not just in one area.

Revenue came in at $24.6 billion, up 14% year-over-year, while net income reached $5.8 billion. Earnings per share hit $3.06, supported by both improved operations and continued buybacks.

The strength was driven by Citi’s core institutional businesses. Services continued to deliver steady growth, while Markets saw a strong rebound, particularly in equities trading. These higher-quality businesses are increasingly shaping the bank’s earnings profile.

At the same time, weaker areas remain. U.S. Consumer Cards saw profits decline, and credit costs are beginning to normalize, which could become a headwind.

Market Reaction

The stock moved from around $126 before earnings to about $129.6 after, a gain of roughly 2.6%. It opened higher, traded up during the day, and held most of those gains into the close.

That kind of price action typically signals that investors not only reacted positively to the results, but also found them credible enough to hold positions rather than sell into strength.

Key Highlights

Citi’s strongest asset remains its Services business, which continues to generate stable growth and high returns.

Markets also delivered a strong quarter, showing Citi can still compete globally in trading, especially during periods of volatility.

Capital return is another key pillar. Citi repurchased $6.3 billion of stock in just one quarter, reinforcing the investment case.

On the other hand, consumer credit remains an area to watch, with declining profits in cards and rising signs of stress in credit metrics.

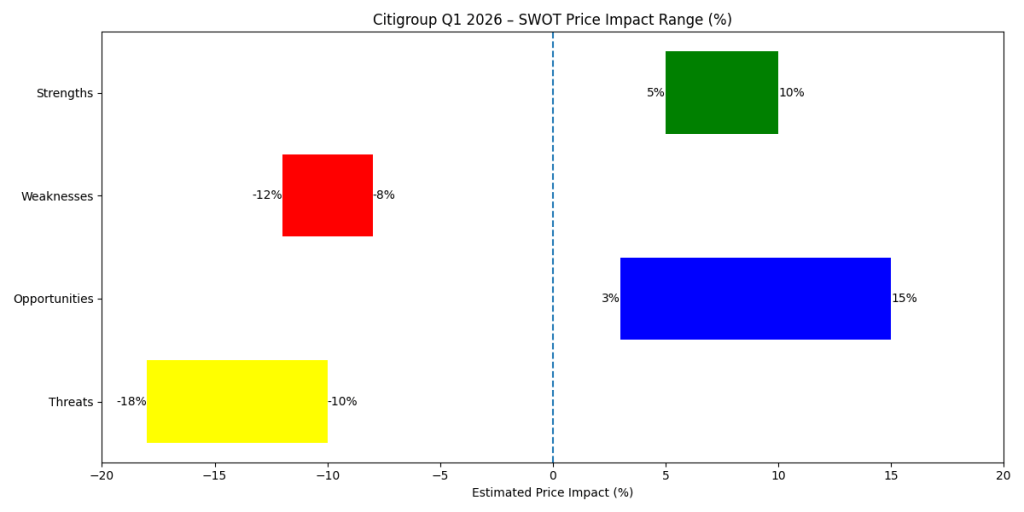

SWOT Analysis (with Price Impact Ranges)

Citi today sits at an interesting point — the business is clearly improving, but the stock is increasingly reflecting that improvement. The following ranges show how each factor could influence valuation.

Strengths

Citi’s biggest strength is the growing contribution from its higher-quality businesses.

The Services franchise continues to deliver strong, stable returns, and as it becomes a larger part of the mix, it can lift overall profitability. At the same time, aggressive share buybacks are supporting earnings per share and helping anchor the stock. Markets also contributed meaningfully this quarter.

👉 Estimated upside impact: +5% to +10% (Services mix improvement)

👉 +4% to +8% (buybacks support)

👉 +3% to +6% (Markets strength, cyclical)

Weaknesses

Despite the progress, Citi still trails the best-performing banks in terms of overall profitability, which limits how much investors are willing to pay for the stock.

Costs remain elevated due to ongoing transformation efforts, and consumer banking — particularly credit cards — continues to face pressure as credit costs normalize.

👉 Estimated downside impact: -8% to -12% (profitability gap vs peers)

👉 -4% to -7% (cost inefficiency)

👉 -3% to -6% (consumer credit pressure)

Opportunities

The biggest opportunity lies in execution. Citi is nearing the end of its transformation program, and meaningful cost improvements could significantly boost returns.

If Citi can sustain higher returns on equity, the market may be willing to re-rate the stock closer to or above book value. Continued buybacks also provide an additional tailwind.

👉 Estimated upside impact: +10% to +18% (cost transformation)

👉 +8% to +15% (RoTCE expansion and re-rating)

👉 +3% to +6% (balance sheet growth)

Threats

The main risks are tied to the credit cycle and the sustainability of recent performance.

Credit quality is starting to show early signs of deterioration, and Markets revenue — while strong this quarter — can be volatile. There is also ongoing execution risk, as Citi still needs to prove that its turnaround is durable.

👉 Estimated downside impact: -10% to -18% (credit deterioration)

👉 -5% to -9% (Markets normalization)

👉 -6% to -10% (execution risk)

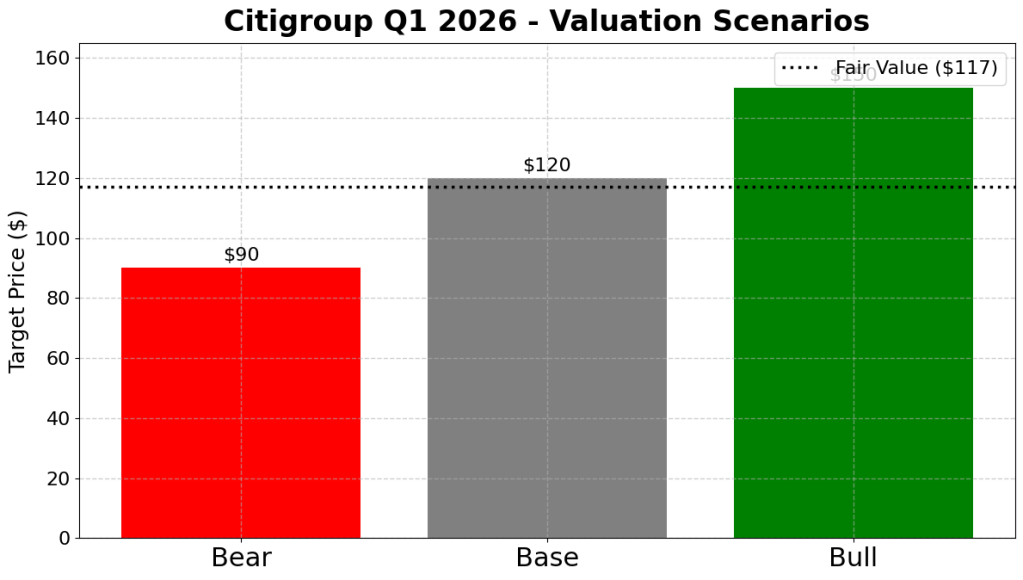

Valuation Scenarios

Citi’s valuation still anchors to its tangible book value of around $99 per share. The key variable is how much return the bank can generate on that capital.

Bear Case (30% probability)

In a downside scenario, credit costs rise and Markets normalize, pushing returns closer to ~10%.

In this case, Citi would likely trade below book value, around 0.9x TBV.

👉 Target Price: ~$90

Base Case (50% probability)

In a more balanced scenario, Citi continues to execute steadily, maintaining returns around 11–12% and delivering gradual efficiency improvements.

This would justify a valuation closer to 1.2x TBV.

👉 Target Price: ~$120

Bull Case (20% probability)

In a stronger execution scenario, Citi successfully improves efficiency and sustains higher returns (13–14%+), leading to a re-rating.

This could push valuation toward 1.5x TBV.

👉 Target Price: ~$150

Probability-Weighted Fair Value

Blending these scenarios results in a fair value of approximately:

👉 ~$117 per share

Verdict

Citi is clearly making progress. The latest results show that the turnaround is real and gaining traction.

But the stock has already moved ahead of that improvement.

At around $130, Citi is trading above what a probability-weighted valuation would suggest. That means investors are no longer buying a discount — they are betting on continued execution.

Call to Action

For value investors, the key question is simple:

👉 Would you buy Citi today, knowing that the upside depends on continued strong execution?

Or would you wait for a pullback to get a better margin of safety?

Disclaimer

This article is for informational purposes only and does not constitute investment advice. All analysis is based on publicly available information from Citigroup’s official financial disclosures. Investors should conduct their own research before making any investment decisions.