TL;DR Summary

Goldman Sachs (GS:NYSE)delivered a powerful Q1 2026 with nearly 20% ROE and record equities trading, reinforcing its position as a top-tier investment bank. However, the stock’s muted reaction suggests that much of this strength was already priced in. At current levels, Goldman looks fairly valued — but without a clear margin of safety if earnings normalize.

Quarter Recap

Goldman Sachs reported a strong start to 2026, with performance driven primarily by its institutional businesses.

Revenue came in at $17.23 billion, with net earnings of $5.63 billion and EPS of $17.55. The firm delivered an impressive 19.8% ROE, signaling highly efficient capital deployment during the quarter.

The standout was Global Banking & Markets, particularly equities trading, which reached record levels. Investment banking also showed signs of recovery, suggesting that deal activity is gradually returning after a slower period.

At the same time, Asset & Wealth Management continued to grow steadily, with assets under supervision reaching $3.65 trillion, providing a more stable earnings base over time.

Key Highlights

- Record equities trading revenue, reinforcing Goldman’s leadership in institutional markets

- Investment banking recovery underway, supporting future earnings visibility

- ROE near 20%, significantly above historical mid-cycle levels

- Continued capital return through buybacks and dividends

- FICC trading declined YoY, showing uneven performance across segments

- Asset & Wealth Management scaling with consistent net inflows

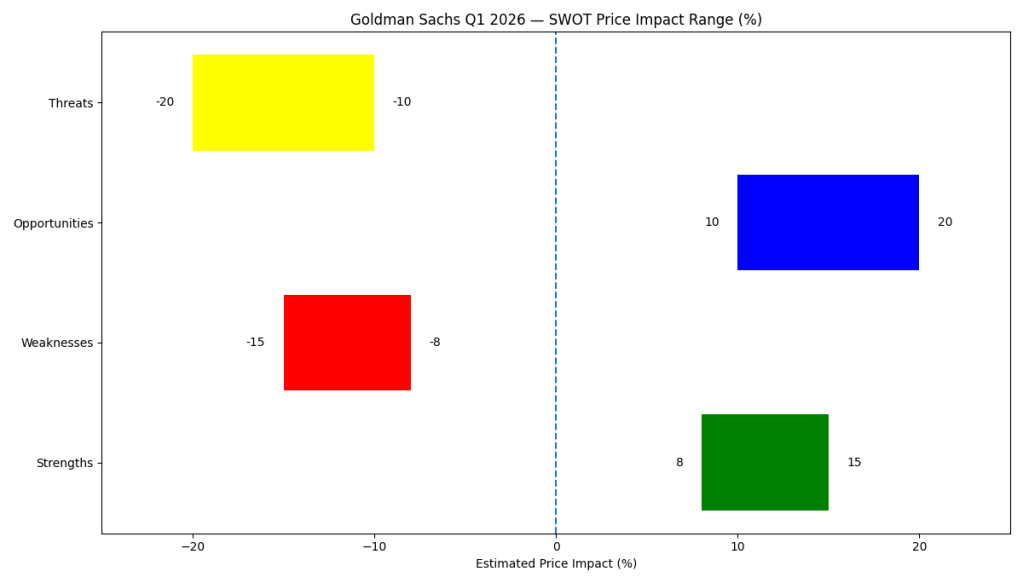

SWOT Analysis

Goldman Sachs is currently operating at a high level of profitability, but the key question for investors is whether this represents a new structural baseline or a cyclical peak.

Strengths

- Exceptional profitability with ROE near 20%, supporting premium valuation potential (+8% to +15%)

- Dominant equities trading franchise with record revenues (+6% to +12%)

- Investment banking showing recovery, providing cyclical upside (+4% to +8%)

- Strong capital return through buybacks and dividends (+5% to +10%)

Weaknesses

- Earnings remain highly dependent on market conditions (-8% to -15%)

- Weakness in FICC trading highlights uneven revenue mix (-4% to -8%)

- Limited recurring revenue compared to peers with stronger fee-based models (-5% to -10%)

- Cost structure still relatively elevated for a cyclical business (-3% to -6%)

Opportunities

- Growth in Asset & Wealth Management can stabilize earnings over time (+6% to +12%)

- Continued recovery in capital markets (M&A, IPOs) (+5% to +10%)

- Strategic shift toward more durable institutional and wealth revenue (+4% to +8%)

- Operating leverage in strong markets can drive margin expansion (+5% to +10%)

Threats

- Macro and geopolitical volatility impacting capital markets (-10% to -20%)

- Risk of trading normalization after record equities performance (-8% to -15%)

- Regulatory pressures limiting capital return (-4% to -8%)

- Market already pricing strong performance, limiting upside (-5% to -10%)

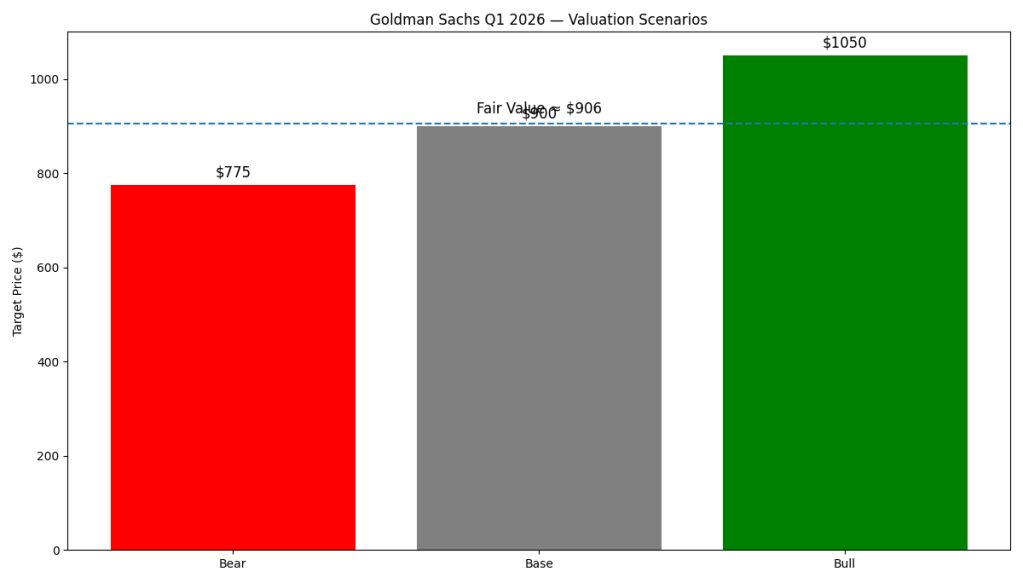

Valuation Scenarios

The valuation hinges on whether current earnings represent sustainable performance or cyclical strength.

Bear Case (~$750–$800)

If trading normalizes and investment banking recovery slows, ROE could fall back to the mid-teens. In this case, Goldman would trade closer to historical valuation ranges.

Base Case (~$880–$920)

If current earnings are largely sustainable with moderate growth, the stock remains around current levels, supported by steady capital return.

Bull Case (~$1,000–$1,100)

If capital markets remain strong and Goldman sustains near-20% ROE, the stock could justify a premium multiple and move higher.

👉 Probability-weighted fair value: ~$900

Verdict

Goldman Sachs is executing extremely well, but the investment case now depends less on performance and more on sustainability.

At current levels, the stock reflects:

- Strong earnings momentum

- High expectations

- Limited margin of safety

For value investors, this is a hold rather than an aggressive buy.

Call to Action

If you’re tracking financial stocks, the key question is:

👉 Do you believe Goldman’s current earnings are sustainable — or cyclical?

Follow SWOTstock for more earnings breakdowns that cut through the noise and focus on what actually drives stock prices.

Disclaimer

This analysis is for informational purposes only and does not constitute financial advice. Investors should conduct their own research and consult with a qualified financial advisor before making investment decisions.