TL;DR Summary

JPMorgan Chase (JPM:NYSE) just delivered a standout Q1 2026, with $5.94 EPS, ~$50B revenue, and record Markets performance. Investment banking is rebounding, credit remains under control, and the balance sheet is exceptionally strong. Yet the stock only moved modestly. That tells you everything: investors are no longer pricing performance — they’re pricing how sustainable this level of earnings is. Fair value now sits around $200.

Quarter Recap

JPMorgan’s Q1 2026 results were strong across nearly every line item. The bank reported $16.5 billion in net income and $5.94 in EPS, supported by $50.5 billion in managed revenue. This was not a narrow beat — it was broad-based strength across consumer banking, investment banking, and trading.

Markets delivered a record $11.6 billion in revenue, while investment banking fees surged 28%, signaling a real recovery in capital markets activity. At the same time, Net Interest Income reached $25.5 billion, still benefiting from the prior rate environment.

Despite the strong numbers, management — led by Jamie Dimon — maintained a balanced tone. The U.S. economy remains resilient, but the forward path depends on interest rates, credit conditions, and broader macro dynamics.

Key Highlights

- EPS: $5.94 → near peak earnings level

- Managed revenue: $50.5B → broad-based growth

- Markets revenue: $11.6B (+20%) → record performance

- Investment banking fees: +28% → recovery gaining traction

- NII: $25.5B (+9% YoY), but +3% ex-Markets → growth slowing underneath

- Credit costs: $2.5B → rising but still controlled

- CET1 ratio: 14.3% → strong capital buffer

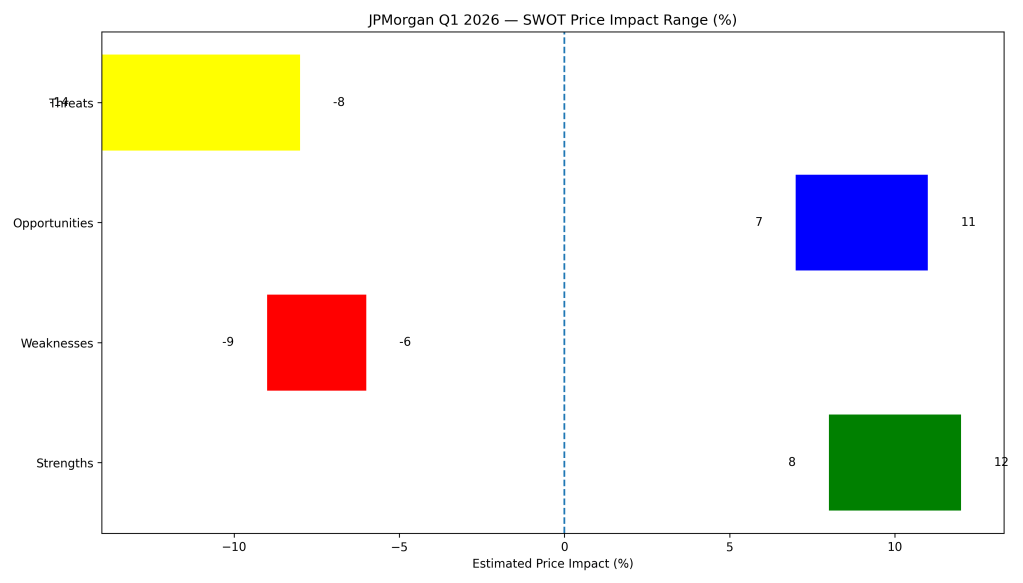

SWOT Analysis

JPMorgan just delivered one of its strongest quarters — but that’s exactly why the bar is now higher. The debate has shifted from performance to durability.

Strengths

- Record Markets revenue ($11.6B) confirms trading leadership→ Estimated impact: +8% to +12%

- Broad-based growth across all major segments (CIB +19%, CCB +7%, AWM +11%)→ Estimated impact: +6% to +9%

- Strong capital position (CET1 14.3%, $291B capital)→ Estimated impact: +5% to +8%

Weaknesses

- NII growth slowing beneath the surface (+3% ex-Markets)→ Estimated impact: -6% to -9%

- High cost base ($26.9B expenses) limits operating leverage→ Estimated impact: -3% to -5%

- Continued sensitivity to interest rate direction→ Estimated impact: -4% to -7%

Opportunities

- Investment banking recovery (+28% fees) could extend over multiple quarters→ Estimated impact: +7% to +11%

- Strong client activity and capital markets momentum→ Estimated impact: +4% to +7%

- Capital return (buybacks + dividends) supports valuation→ Estimated impact: +5% to +8%

Threats

- Credit normalization ($2.5B credit costs, rising charge-offs)→ Estimated impact: -8% to -14%

- Regulatory pressure on capital requirements→ Estimated impact: -4% to -7%

- Earnings peak risk as cycle normalizes→ Estimated impact: -6% to -10%

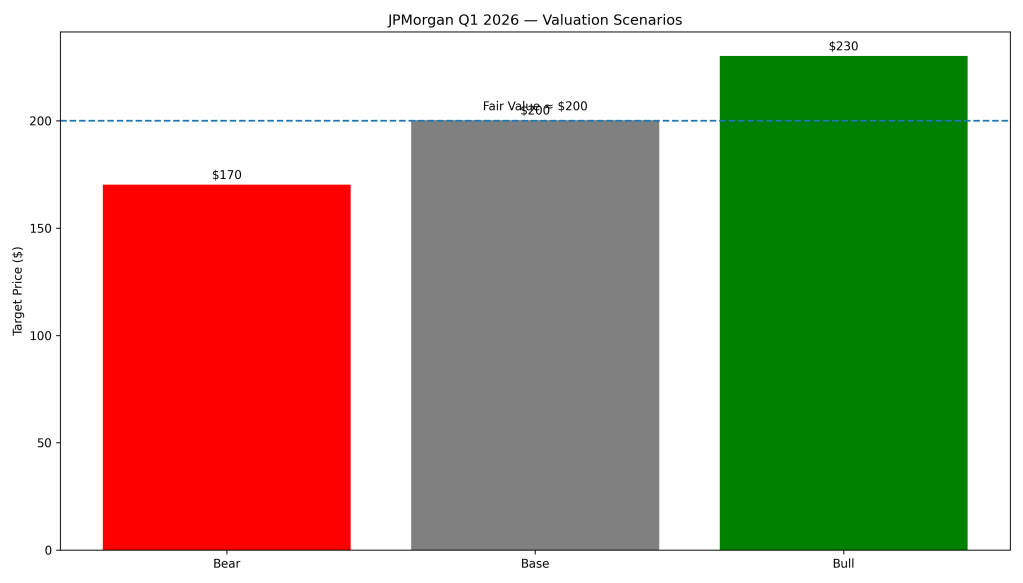

Valuation Scenarios

The key question is simple: is $5.94 EPS a new baseline — or a cyclical peak?

Bear Case — $170

- NII declines as rates fall

- Credit costs rise further

- Markets revenue normalizes

Base Case — $200

- NII softens but remains elevated

- IB recovery offsets part of the decline

- Credit increases gradually

Bull Case — $230

- Markets stay strong longer

- IB recovery accelerates

- Credit remains benign

Fair Value

👉 Probability-weighted fair value: ~$200/share

Verdict

JPMorgan remains the highest-quality bank in the market — and this quarter proves it. But quality is no longer the question. Sustainability is.

At current levels, the stock looks fairly valued. The upside case requires near-perfect conditions to persist, while the downside emerges if credit costs rise and NII declines at the same time.

For value investors, this is not a chase — it’s a stock to accumulate on weakness.

Call to Action

Would you buy JPMorgan below $180 if credit risks start to rise?

Or do you believe its earnings power justifies holding through the cycle?

👉 Follow SWOTstock for grounded, data-driven earnings analysis.

Disclaimer

This article is for informational purposes only and does not constitute financial advice. Investors should conduct their own research and consider their risk tolerance before making investment decisions.