TL;DR

Accenture (ACN:NYSE) delivered another quarter of solid execution, beating expectations on revenue and earnings while maintaining margins and strong cash generation. AI demand continues to build, but management remains cautious on near-term revenue acceleration. At around $270, ACN appears fairly valued, with upside dependent on whether AI-led reinvention can meaningfully lift topline growth.

Quarter Recap

- Fiscal Q1 2026 revenue came in at the high end of guidance, reflecting resilient enterprise demand despite a cautious macro environment.

- Adjusted earnings grew faster than revenue, supported by disciplined cost control and modest operating leverage.

- New bookings remained healthy, including continued momentum in AI-related transformation programs.

- Management reiterated a cautious full-year outlook, emphasizing execution and long-term positioning rather than near-term acceleration.

Key Highlights

- Revenue growth remained in the low- to mid-single-digit range, consistent with guidance.

- Adjusted operating margins expanded modestly year over year.

- Free cash flow supported ongoing dividends and share repurchases.

- AI was framed as a core component of multi-year reinvention programs, not a standalone growth spike.

- U.S. federal-related work continued to weigh on near-term growth visibility.

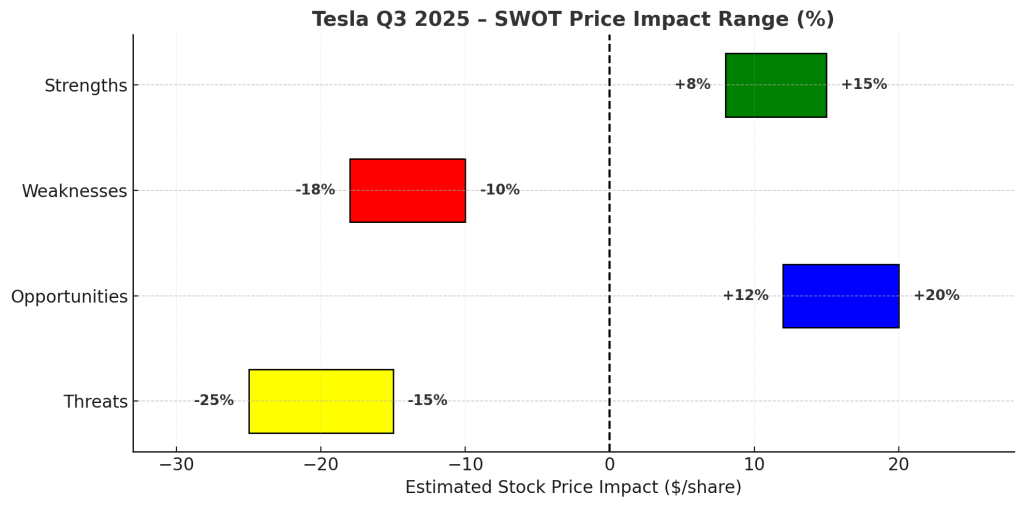

SWOT Analysis

Accenture’s investment profile reflects a balance between durable execution strength and a growth trajectory that remains steady rather than accelerating. The ranges below translate qualitative factors into estimated stock price impact.

Strengths

- Deep enterprise relationships and recurring transformation demand (+8% to +12%)

- AI embedded into large-scale reinvention programs, supporting long-term monetization (+6% to +10%)

- Strong cash flow, balance sheet discipline, and shareholder returns (+4% to +6%)

Strengths — overall impact: +18% to +28%

Weaknesses

- Low-single-digit organic revenue growth profile (–6% to –10%)

- Continued softness in U.S. federal business (–4% to –7%)

- Premium valuation leaves limited margin for disappointment (–5% to –8%)

Weaknesses — overall impact: –15% to –25%

Opportunities

- Scaling AI-led reinvention programs across global enterprises (+10% to +18%)

- Operating leverage if demand gradually normalizes (+6% to +10%)

- Leadership role as an enterprise AI orchestrator across platforms and models (+5% to +8%)

Opportunities — overall impact: +21% to +36%

Threats

- Prolonged enterprise budget caution delaying large transformation decisions (–10% to –15%)

- Investor narrative around AI commoditization compressing consulting multiples (–8% to –12%)

- Competitive pricing pressure from smaller firms and in-house teams (–5% to –8%)

Threats — overall impact: –23% to –35%

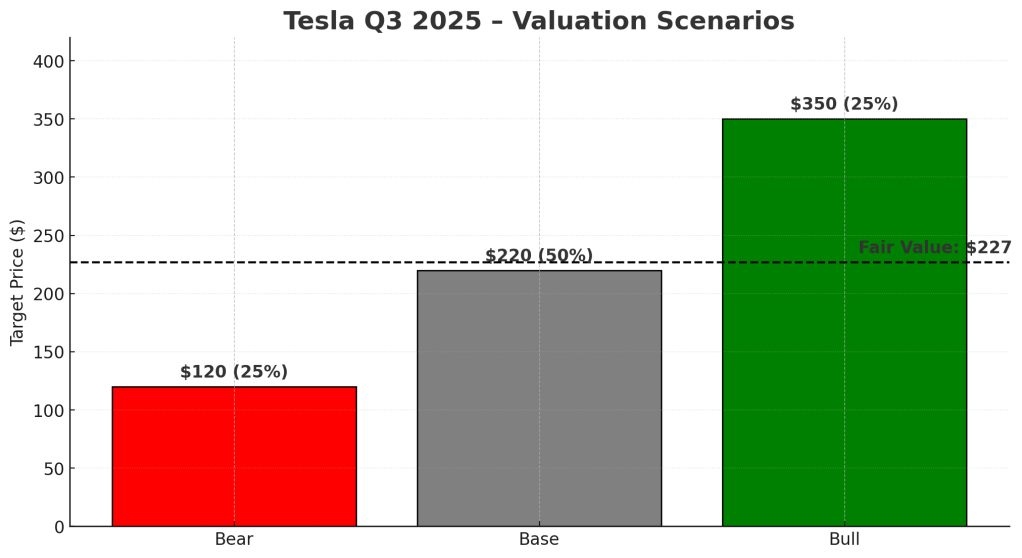

Valuation Scenarios

Accenture’s valuation outcome hinges less on margin execution—which remains strong—and more on whether AI-driven reinvention can re-accelerate revenue growth.

Using $270 as the current price anchor:

Bear Case

- Revenue growth remains around 2–3%

- Federal weakness persists and AI monetization is slower than expected

- Valuation multiple compresses toward the lower end of historical ranges

- Implied price: ~$209 (–22.5%)

Base Case

- Revenue growth stabilizes around 4–5%

- AI bookings convert gradually into revenue

- Margins expand modestly, supporting high-single-digit EPS growth

- Implied price: ~$290 (+7.5%)

Bull Case

- AI-led reinvention drives sustained revenue acceleration above 6%

- Enterprise spending cycle improves

- Operating leverage supports double-digit EPS growth with modest multiple expansion

- Implied price: ~$351 (+30%)

Fair Value Assessment

Applying a probability-weighted approach:

- Bear: 25%

- Base: 50%

- Bull: 25%

This results in a probability-weighted fair value of approximately $285, or about 5–6% upside from current levels.

Verdict

Accenture remains a high-quality compounder with durable client relationships, strong execution, and disciplined capital returns. At around $270, the stock looks fairly valued rather than cheap. Downside is cushioned by cash flow and margins, but meaningful upside will require clearer evidence that AI-led reinvention can translate into sustained topline acceleration.

Call to Action

If you’re tracking enterprise AI adoption beyond the hype, follow SWOTstock for earnings-driven analysis that focuses on what actually moves stock prices.

Disclaimer

This article is for informational purposes only and does not constitute investment advice. All analysis is based on publicly available, official company disclosures and earnings call commentary. Investors should conduct their own research or consult a financial professional before making investment decisions.