TL;DR Summary

Vertiv (VRT:NYSE) delivered a strong Q4 2025 with 23% revenue growth, massive order acceleration (+252% YoY), and a $15B backlog that reinforces AI infrastructure demand. Margins expanded and free cash flow remained robust.

However, expectations are now extremely high.

Using management’s official 2026 EPS guidance of ~$6.02 and a disciplined 25x multiple, fair value sits near $150 per share. Investors must now decide: is Vertiv an AI compounder — or an expectations trap?

Quarter Recap

Vertiv closed FY2025 with clear operational momentum.

Q4 net sales reached $2.88B, up roughly 23% year-over-year. Adjusted EPS came in at $1.36, while GAAP EPS was $1.14. The key driver was demand — not cost cutting.

Organic orders surged approximately +252% YoY, pushing backlog to nearly $15B. That backlog is critical. It provides visibility into 2026 and reflects hyperscaler and AI-related infrastructure demand.

Full-year 2025 revenue reached $10.23B, and adjusted EPS was $4.20. Operating cash flow exceeded $2.1B, and adjusted free cash flow totaled $1.89B.

Balance sheet leverage remains modest at approximately 0.5x net leverage.

Management guided for 2026:

- Revenue: $13.25B – $13.75B

- Adjusted EPS: $5.97 – $6.07

- Operating margin: 22–23%

- Free cash flow: $2.1B – $2.3B

This implies continued double-digit top-line growth and ~40%+ earnings growth at midpoint.

Key Highlights

• Revenue growth remains strong at 23% YoY

• Orders exploded +252% YoY

• Book-to-bill near 2.9x

• Backlog ~$15B

• Adjusted operating margin 23.2%

• 2026 EPS guidance midpoint ~$6.02

The real story is demand visibility, not just quarterly earnings.

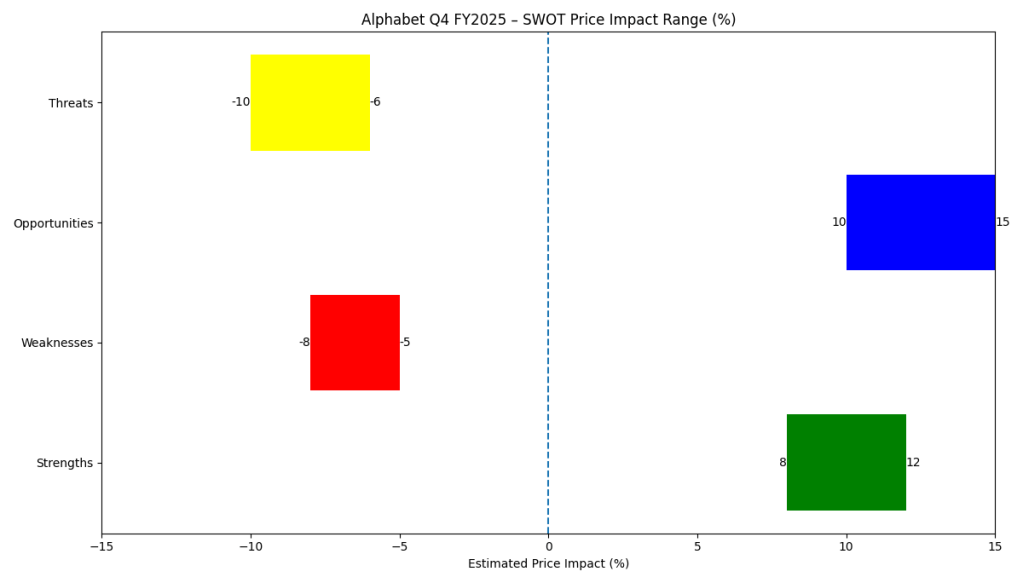

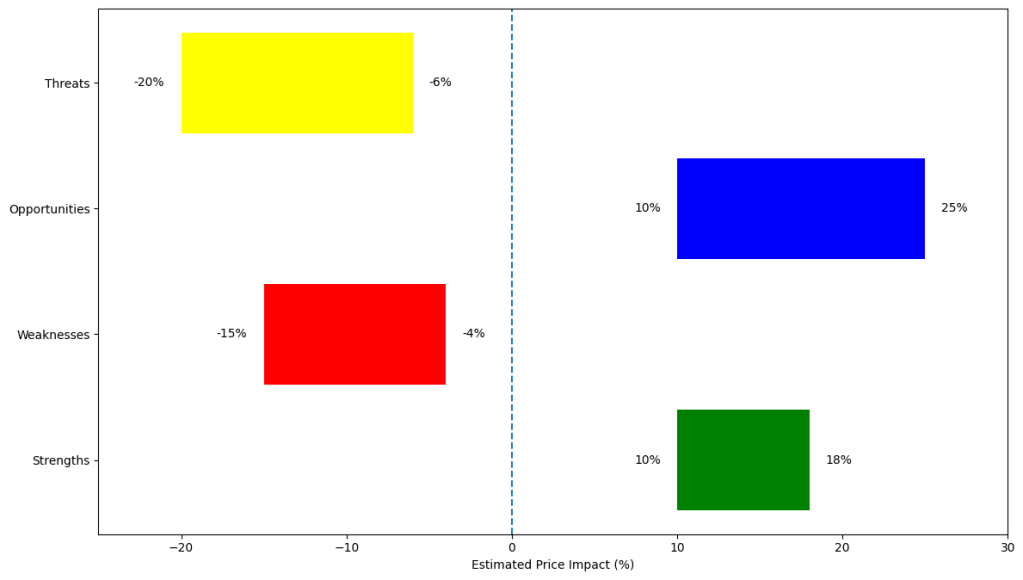

SWOT Analysis

Vertiv is no longer being evaluated as a recovery industrial. It is being priced as a structural AI infrastructure enabler. That changes the risk profile entirely.

Strengths

• Massive order acceleration and backlog visibility

Estimated price impact: +10% to +18%

• Margin expansion and operational leverage

Estimated price impact: +6% to +10%

• Strong free cash flow and low leverage

Estimated price impact: +4% to +8%

Weaknesses

• GAAP EPS slight miss vs expectations

Estimated price impact: –4% to –7%

• High embedded expectations in valuation

Estimated price impact: –8% to –15% if growth moderates

Opportunities

• AI data-center density shift (liquid cooling, high power racks)

Estimated price impact: +15% to +25% over 12–24 months

• 2026 guidance execution driving multiple support

Estimated price impact: +10% to +20%

Threats

• Hyperscaler capex cyclicality

Estimated price impact: –12% to –20%

• Competitive margin pressure

Estimated price impact: –6% to –12%

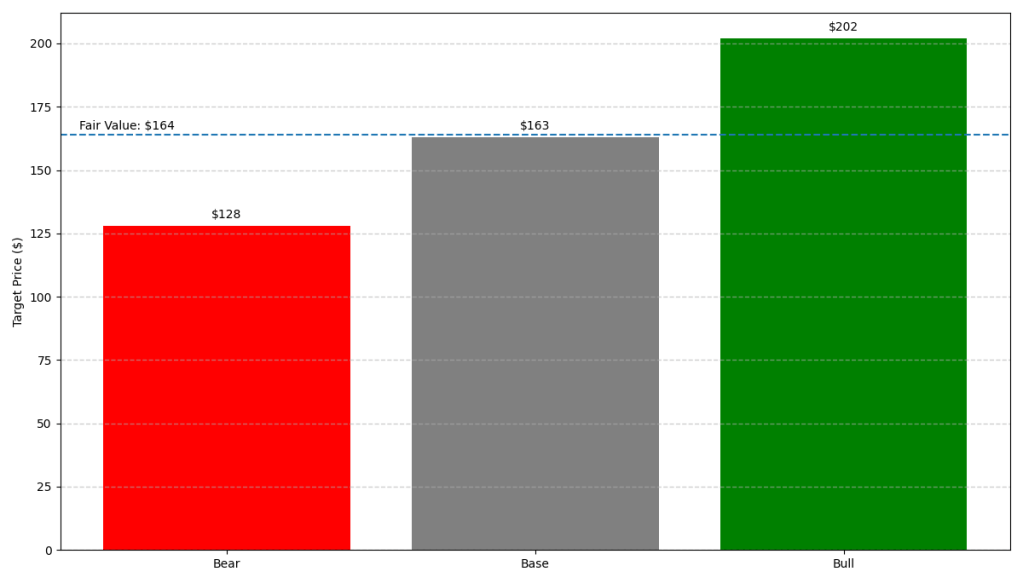

Valuation Scenarios

Vertiv guided to approximately $6.02 adjusted EPS for FY2026. Valuation sensitivity now revolves around multiple sustainability.

Bear Case

EPS: $5.80

Multiple: 22x

Price Target: $128

Base Case

EPS: $6.02

Multiple: 27x

Price Target: $163

Bull Case

EPS: $6.30

Multiple: 32x

Price Target: $202

Probability-Weighted Fair Value

Fair value ≈ $164

Disciplined fair value using only management guidance and a conservative 25x multiple: ~$150

Verdict

Vertiv is executing.

Demand is real. Backlog is strong. Margins are expanding.

The risk is no longer operational — it’s valuation compression if AI capex momentum slows or if execution stumbles even slightly.

At prices near or below $150, the stock offers a reasonable risk-reward profile for growth investors.

Above that range, it becomes increasingly expectation-driven.

Call to Action

If you found this breakdown helpful, follow SWOTstock for disciplined earnings analysis that separates fundamentals from narrative.

We focus on what the numbers say — not what the hype suggests.

Disclaimer

This analysis is for informational purposes only and does not constitute financial advice. Always conduct your own research before making investment decisions.