Q1 2025 Highlights: What Investors Need to Know

Berkshire Hathaway (NYSE: BRK-A, BRK-B)posted lower operating earnings and unrealized investment losses in Q1 2025, but its balance sheet has never been stronger. With $189 billion in cash and minimal debt, Buffett’s firm is in prime position for future moves—just not in a rush to make them. Despite short-term softness, long-term upside remains, and the stock may be modestly undervalued.

Quarter Recap

In the first quarter of 2025, Berkshire Hathaway reported operating earnings of $8.48 billion, a 7.9% decline year-over-year, reflecting mixed performance across its key segments. Insurance underwriting weakened, GEICO remained under pressure, and BNSF Railway delivered flat results. Meanwhile, investment income benefited from higher interest rates on Treasury holdings.

Buffett and his team remained firm in their philosophy: act only when the odds are overwhelmingly in their favor. Despite a sizable unrealized investment loss of $11.2 billion for the quarter, largely due to equity market fluctuations, they emphasized long-term discipline and capital strength.

One line captures the essence of the quarter: “Better to hold cash than chase risk.”

Key Highlights

- Operating Earnings: $8.48B (–7.9% YoY)

- Net Earnings: $(11.2)B (driven by unrealized investment losses)

- Insurance Underwriting Profit: $1.16B (–19% YoY)

- Cash and Treasury Holdings: $189B (record high)

- BNSF Railway Earnings: Flat YoY

- Interest Income from T-Bills: Estimated $7.5–8B annualized

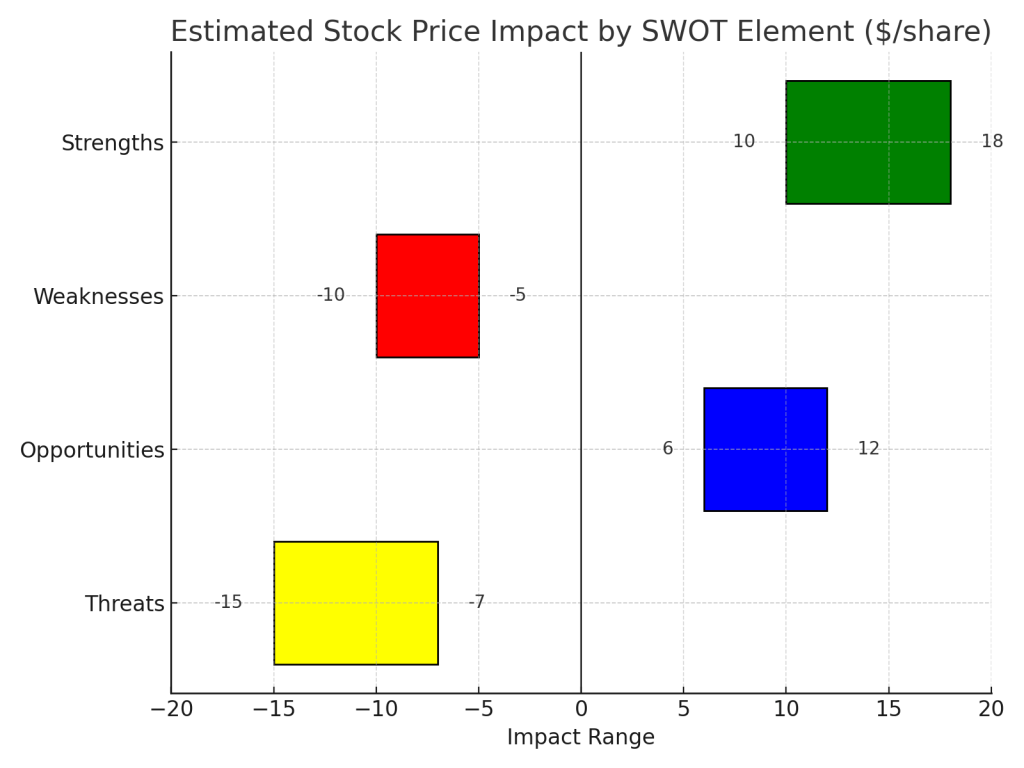

SWOT Analysis

Let’s break it down using the simple SWOT framework—what’s going well, what’s not, where the upside is, and what risks could derail the story.

Strengths (Estimated Impact: +30 to +50 USD/share)

Berkshire Hathaway’s greatest strength this quarter lies in its unrivaled financial flexibility. With $189 billion in cash and Treasury holdings, minimal debt, and stable earnings from insurance, utilities, and BNSF Railway, the company maintains a defensive yet opportunistic posture. Its insurance float continues to be a low-cost source of funding, while interest income alone now contributes nearly $8 billion annually at minimal risk. This level of capital strength supports a premium valuation multiple and provides built-in downside protection. If investors continue rewarding this structural advantage, these strengths could add $30 to $50 per share to Berkshire’s valuation.

Weaknesses (Estimated Impact: –15 to –20 USD/share)

The downside in this quarter comes from persistent softness in GEICO underwriting, which remains below peer performance despite years of restructuring. Insurance profits fell 19% year-over-year, while BNSF’s earnings were flat due to freight volume stagnation and inflationary pressure. In addition, Berkshire’s manufacturing and retail units—exposed to consumer cyclicality—continue to underwhelm. These underperforming segments may weigh on consolidated earnings growth and investor sentiment, potentially reducing fair value by $15 to $20 per share if they fail to rebound over the next several quarters.

Opportunities (Estimated Impact: +35 to +45 USD/share)

The most compelling upside comes from Berkshire’s ability to deploy capital. With markets remaining volatile, Berkshire is uniquely positioned to act during dislocations. Even without a major acquisition, its Treasury yield is now a legitimate earnings driver, supporting operating income with near-zero risk. In addition, the orderly CEO succession to Greg Abel appears to be progressing well, boosting investor confidence in the post-Buffett era. If Berkshire begins putting even a fraction of its cash to work in high-return assets, and if market sentiment improves around capital efficiency, the stock could gain $35 to $45 per share in valuation upside.

Threats (Estimated Impact: –25 to –30 USD/share)

However, risks remain. Unrealized equity investment losses totaled $11.2 billion in Q1, raising concerns over market volatility and concentration in large holdings like Apple. Succession optics—while stable—still carry narrative risk if markets test Berkshire’s leadership. Moreover, macroeconomic headwinds such as a slowdown in U.S. freight or tighter regulation on insurance operations could strain profitability. If equity markets falter or earnings growth continues to slow, the downside from these threats could weigh $25 to $30 per share on the stock, particularly if investors shift toward faster-growth alternatives.

SWOT Summary

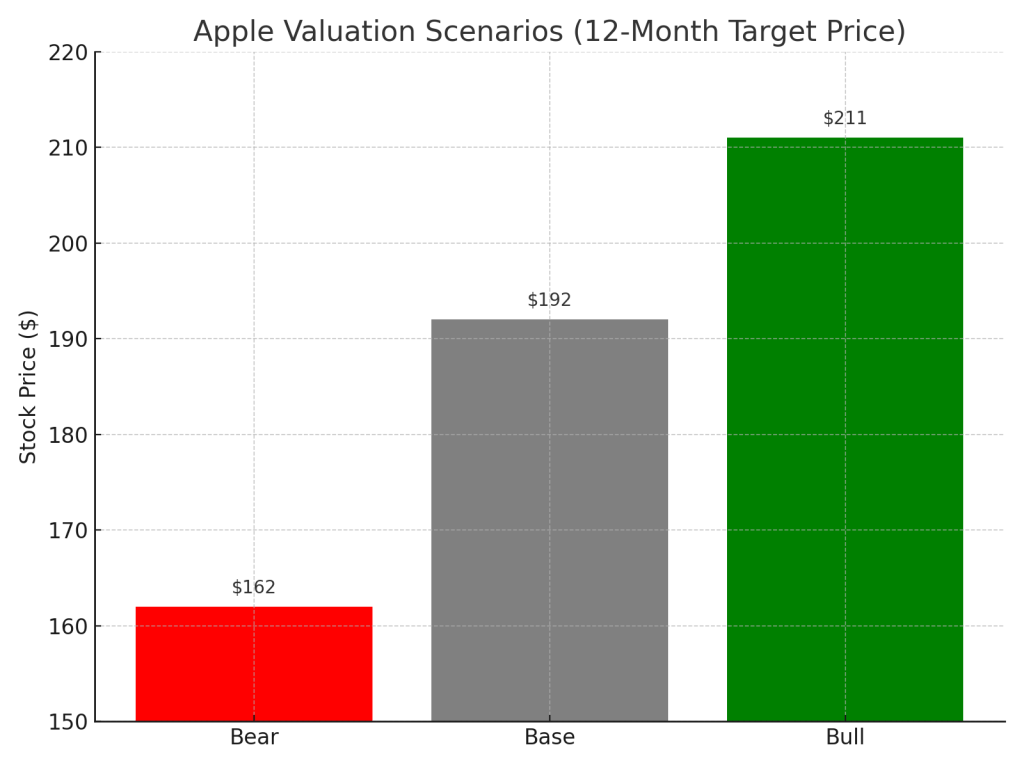

Valuation Scenarios (BRK.B)

Bull Case – $470/share (25% probability)

In the most optimistic scenario, Berkshire deploys a meaningful portion of its $189B cash into high-return investments, insurance underwriting improves across GEICO and reinsurance segments, and its equity portfolio—especially large tech holdings—rebounds strongly. Interest income continues contributing ~$8B annually, lifting operating earnings. If normalized earnings rise and the market awards a 17x multiple (reflecting premium safety and compounding potential), BRK.B could trade at $470. This assumes both smart capital allocation and a favorable macro backdrop, and we assign it a 25% probability.

Base Case – $420/share (60% probability)

The base case assumes Berkshire maintains steady performance: insurance earnings stabilize, BNSF and energy divisions grow modestly, and equity marks remain flat. Interest income boosts baseline earnings, but no major acquisitions occur in the near term. We estimate operating earnings around $35B, applying a conservative 15x multiple in line with historical norms. This results in a $420 valuation. Given Buffett’s cautious stance and consistent fundamentals, we assign this scenario the highest probability at 60%.

Bear Case – $360/share (15% probability)

In the downside scenario, insurance losses persist, equity markets underperform, and Berkshire delays deploying its excess capital, weighing on return on equity. If investment losses continue and operating income weakens due to economic headwinds, the stock could be re-rated at a 12x multiple. This implies a $360 valuation. While Berkshire’s balance sheet offers downside protection, market overreaction or leadership transition sentiment could push shares lower, justifying a 15% probability for this outcome.

Probability-Weighted Valuation

(420 × 0.6) + (470 × 0.25) + (360 × 0.15) = 252 + 117.5 + 54 = $423.50

Verdict: Is BRK.B Overvalued?

- Current Price (May 9, 2025): $513.74

- Estimated Fair Value: $423.50

Conclusion:

At ~21.3% above fair value, BRK.B appears overvalued based on company fundamentals and risk-weighted scenarios. The current price reflects investor confidence—but may leave little room for error or near-term upside.

Call to Action

Want simple stock breakdowns like this in your inbox?

Subscribe now and get the next big-name earnings decoded—before the headlines do.

Disclaimer

This post is based solely on Berkshire Hathaway’s official Q1 2025 financial report and shareholder meeting transcript. No third-party commentary or external data was used. This is not investment advice. Please do your own research before making investment decisions.

Leave a comment