TL;DR Summary

Coca-Cola delivered stable Q4 and full-year 2025 results, but nothing that changes the long-term thesis. Revenue slightly missed expectations, EPS was solid, and 2026 guidance points to mid-single-digit organic growth and high-single-digit EPS growth.

For DIY value investors, this remains a quality compounder — but valuation discipline matters. My fair value estimate sits around $60–$64, suggesting limited upside unless growth accelerates.

Quarter Recap

The Coca-Cola Company reported Q4 and full-year 2025 earnings on February 10, 2026.

Key takeaways from the quarter:

- Q4 revenue grew modestly year-over-year but slightly missed consensus expectations

- Global unit case volume increased ~1%

- Net income rose modestly, reflecting stable margins

- Full-year organic revenue growth was around ~5%

- 2026 guidance calls for ~4–5% organic revenue growth and ~7–8% adjusted EPS growth

Nothing broke. Nothing accelerated dramatically either.

This is exactly what Coca-Cola has become: a steady, predictable, cash-flow-driven business.

Key Highlights

- Volume resilience: Global volumes still growing despite mature markets

- Pricing power intact: Revenue growth supported by pricing and mix

- Margin stability: Operating discipline preserved profitability

- Defensive profile maintained: Cash flow strength supports dividends and capital returns

- Guidance steady, not exciting: Mid-single-digit organic growth outlook

The market reaction was mildly negative — largely due to the revenue miss and lack of upside surprise.

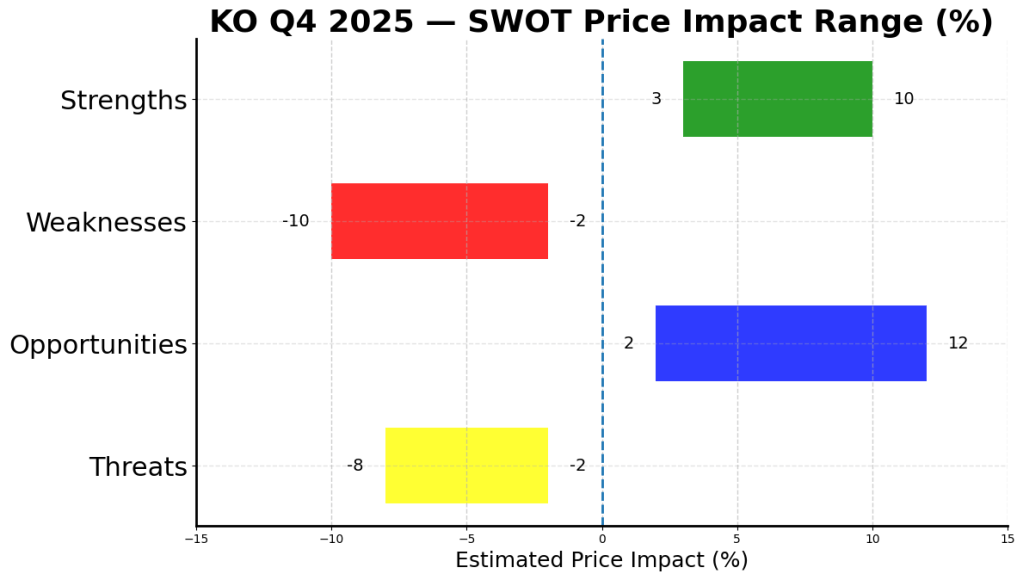

SWOT Analysis

Coca-Cola remains one of the most durable consumer franchises globally. However, valuation is the key variable. For a Type 2 value investor, the debate is not about survival — it is about growth durability versus multiple compression.

Strengths

- Global brand dominance and pricing powerEstimated price impact: +5% to +10%

- Strong free cash flow and dividend profileEstimated price impact: +4% to +8%

- Stable operating marginsEstimated price impact: +3% to +6%

Weaknesses

- Low organic volume growth (~1%)Estimated price impact: -3% to -6%

- Premium valuation relative to growth rateEstimated price impact: -5% to -10%

- Currency exposure from global footprintEstimated price impact: -2% to -5%

Opportunities

- Expansion of zero-sugar and premium offeringsEstimated price impact: +4% to +9%

- Emerging market per-capita consumption growthEstimated price impact: +5% to +12%

- Operational acceleration under new leadershipEstimated price impact: +2% to +6%

Threats

- Sugar taxes and regulatory pressuresEstimated price impact: -4% to -8%

- Consumer trade-down in weaker macroEstimated price impact: -3% to -7%

- Commodity cost volatilityEstimated price impact: -2% to -6%

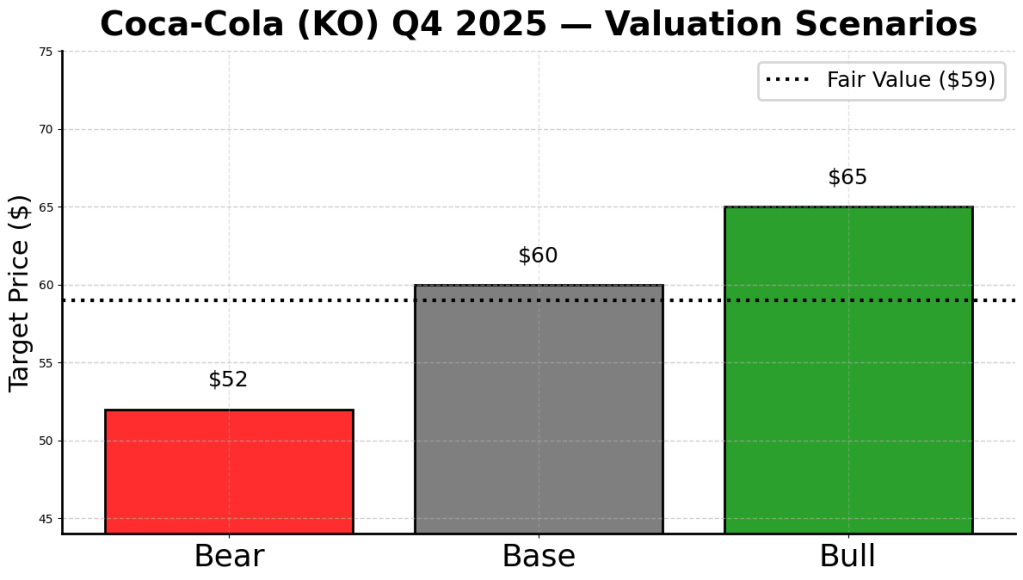

Valuation Scenarios

Coca-Cola is not a high-growth stock. It is a defensive compounder. That means valuation depends primarily on earnings durability and acceptable multiple range.

Assumptions:

- 2025 adjusted EPS ≈ $2.60

- 2026 expected EPS ≈ $2.80 (midpoint growth assumption)

- Historical defensive P/E range: 20x–26x

Bear Case

- Growth slows to ~3%

- Multiple compresses to ~20x

- Target price ≈ $52

- Probability: 30%

Base Case

- Organic growth ~4–5%

- Multiple stabilizes around ~23x

- Target price ≈ $60

- Probability: 50%

Bull Case

- EPS growth accelerates to ~9–10%

- Multiple expands to ~25x

- Target price ≈ $65

- Probability: 20%

Probability-Weighted Fair Value

Estimated fair value: ~$58–$62

Verdict

Coca-Cola remains one of the safest consumer franchises globally. But at today’s valuation, investors are paying for stability, not acceleration.

For value investors:

- Below $58 → Attractive entry

- Around $60 → Fair value

- Above $65 → Fully priced defensive

This is no longer a turnaround story. It is a disciplined compounding story.

Call to Action

If you are a DIY value investor, the key question is simple:

Are you buying durability at a reasonable price — or paying a premium for safety?

Follow SWOTstock for structured, valuation-driven analysis on quality businesses.

Disclaimer

This analysis is for informational and educational purposes only and does not constitute investment advice. Always conduct your own research and consult a financial professional before making investment decisions.

Leave a comment