TL;DR Summary

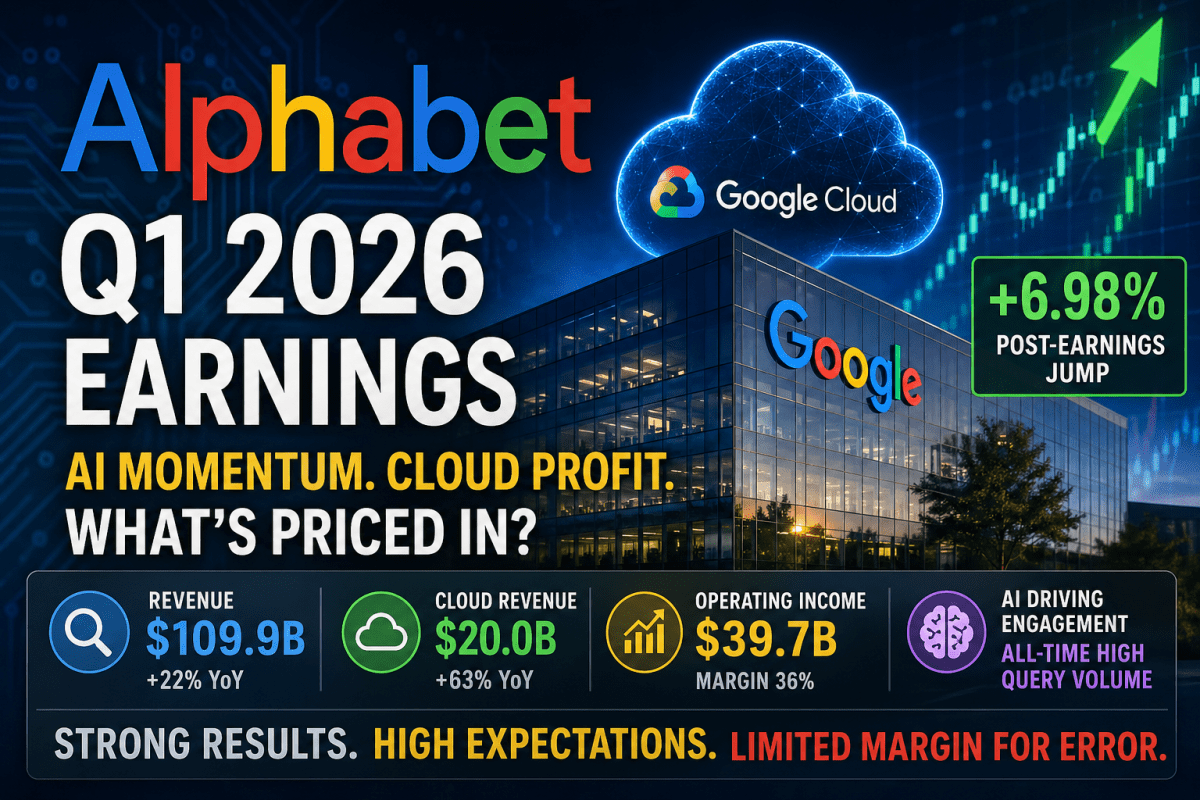

Alphabet (GOOGL:NASDAQ) just delivered a breakout quarter — but the stock may have moved even faster than the fundamentals. Revenue surged, Cloud profits inflected, and AI is clearly driving engagement. The market responded with a nearly 7% jump, signaling growing confidence that Alphabet can win in the AI era.

However, once you strip out non-operating gains and normalize earnings, the valuation tells a more cautious story. At current levels, investors are paying for a future where AI monetization and Cloud profitability scale flawlessly — a future that is not fully proven yet.

Quarter Recap

Alphabet Inc. reported a strong Q1 2026, showing that its core business remains resilient even as the industry shifts toward AI. Revenue grew 22% year-over-year to $109.9 billion, while operating income climbed to $39.7 billion, expanding margins to over 36%.

The standout performance came from Google Cloud, which grew 63% and delivered a sharp increase in operating profit. Meanwhile, Search — the company’s core engine — continued to grow at a high-teens rate, contradicting fears that AI would immediately disrupt its dominance.

Management emphasized that AI is already increasing user engagement across products, with query volumes reaching all-time highs. At the same time, capital expenditures surged, reflecting the massive infrastructure buildout required to support AI at scale.

Key Highlights

- Revenue: $109.9B (+22% YoY)

- Operating income: $39.7B (+~30% YoY)

- Operating margin: ~36%

- Diluted EPS: $5.11 (~$2.35 from non-operating gains)

- Google Cloud revenue: $20.0B (+63% YoY)

- Google Cloud operating income: $6.6B (tripled YoY)

- Capex (property & equipment): ~$35.7B

SWOT Analysis

Alphabet’s latest results mark a turning point. The company is no longer defending its position in AI — it is actively shaping the landscape. The key question now is not whether Alphabet can compete, but whether it can convert its scale advantage into sustainable profits.

Strengths

- Cloud profit inflection (+10% to +18%)

Google Cloud is now a real earnings contributor. This transition from growth to profitability could justify a structural re-rating of the business. - Search resilience in the AI era (+8% to +14%)

Continued strong growth and rising engagement suggest that AI is enhancing, not replacing, Search — a major shift in narrative. - Unmatched AI distribution scale (+6% to +10%)

Alphabet can deploy AI across billions of users through Search, YouTube, and Android, creating a monetization advantage that smaller AI players lack.

Weaknesses

- Extreme capital intensity (-6% to -10%)

AI infrastructure requires massive ongoing investment, which may pressure free cash flow and delay margin expansion. - High reliance on advertising (-4% to -7%)

Despite diversification, the majority of revenue still comes from ads, exposing Alphabet to economic cycles. - Earnings quality distortion (-3% to -5%)

A significant portion of EPS came from non-operating gains, which may not be repeatable.

Opportunities

- AI-driven monetization expansion (+10% to +18%)

If AI increases the value of each search interaction, Alphabet could unlock a higher revenue per user. - Cloud as a second profit engine (+8% to +15%)

Continued growth and margin expansion in Cloud could materially change Alphabet’s earnings mix. - Enterprise AI ecosystem growth (+5% to +9%)

Integration across Cloud, Workspace, and Gemini creates a powerful enterprise platform.

Threats

- Sustained high AI cost structure (-8% to -14%)

If inference and infrastructure costs remain elevated, profitability could be constrained. - Shift toward AI-native interfaces (-6% to -12%)

Changes in user behavior away from traditional search could weaken Alphabet’s core moat over time. - Regulatory pressure (-4% to -8%)

Ongoing antitrust scrutiny could impact distribution and growth.

Valuation Scenarios

Alphabet is now being priced as both a mature cash generator and a high-growth AI platform. The valuation depends heavily on whether AI investments translate into durable earnings growth.

Bear Case — $300–320

- AI costs outpace monetization

- Search growth slows

- Earnings normalize without non-operating gains

→ Multiple compresses, leading to downside of 15–20%

Base Case — $360–390

- Search remains stable

- Cloud continues scaling profitably

- AI monetization gradually offsets costs

→ Current valuation holds, with limited upside

Bull Case — $420–460

- AI significantly increases monetization per query

- Cloud becomes a major profit driver

- Operating leverage improves despite high capex

→ Multiple expands, driving 15–25% upside

Probability-weighted fair value

- Bear (20%): $310

- Base (50%): $375

- Bull (30%): $440

👉 Estimated fair value: ~$377

Verdict

Alphabet has clearly proven that it can compete — and even lead — in the AI era. The latest earnings remove a major overhang around Search disruption and validate the long-term potential of Google Cloud.

However, the stock’s sharp post-earnings move suggests that much of this optimism is already priced in. When adjusting for non-operating gains and considering the heavy capital requirements of AI, the current valuation leaves limited margin for error.

This is no longer a “buy at any price” growth story. It is a high-quality business transitioning into a capital-intensive phase, where execution matters more than ever.

Call to Action

If you want more AI-driven earnings breakdowns like this — focused on what actually moves stock prices — follow SWOTstock and stay ahead of the market narrative.

Disclaimer

This analysis is for informational purposes only and does not constitute financial advice. Always conduct your own research and consult with a qualified financial advisor before making investment decisions.