Airbnb (NASDAQ: ABNB) reported its Q1 2025 earnings on May 1, 2025, highlighting steady growth in bookings and revenue, alongside strategic investments aimed at long-term expansion.

📅 Airbnb Q1 2025 Recap

Airbnb delivered a solid Q1 2025, marked by steady growth in bookings and resilient financial performance, despite macroeconomic headwinds. The company reported $2.27 billion in revenue, reflecting 6% year-over-year growth, which would have been approximately 11% on a constant-currency and calendar-adjusted basis. Although net income fell to $154 million (from $264 million a year ago), this was largely due to higher stock-based compensation, write-downs on investments, and lower interest income. Importantly, free cash flow reached a record $1.8 billion, driven by strong seasonality and healthy booking trends.

Operationally, nights and experiences booked rose 8% year-over-year to 143 million, with Gross Booking Value (GBV) up 7% to $24.5 billion. Growth was driven particularly by strength in Latin America (low 20s%) and Asia Pacific (mid-teens%), while North America showed more modest gains. Airbnb also returned value to shareholders through $807 million in stock repurchases, reducing its diluted share count to 660 million.

Management emphasized ongoing investment in product innovation—such as pricing transparency tools and improved communication features—to drive long-term differentiation. Looking forward, Q2 guidance anticipates ~12–14% revenue growth with stable ADRs, reflecting a cautious but optimistic outlook heading into the summer travel season.

📊 Q1 2025 Financial Highlights

- Revenue: $2.27 billion, a 6% increase year-over-year. Adjusted for foreign exchange and calendar effects, revenue growth would have been approximately 11%.

- Net Income: $154 million, down from $264 million in Q1 2024, primarily due to higher stock-based compensation, investment write-downs, and lower interest income.

- Adjusted EBITDA: $417 million, representing an 18% margin.

- Free Cash Flow: $1.8 billion, with a trailing twelve-month free cash flow of $4.4 billion.

- Nights and Experiences Booked: 143 million, an 8% increase year-over-year.

- Gross Booking Value (GBV): $24.5 billion, up 7% year-over-year.

- Share Repurchases: $807 million in Q1 2025, reducing the fully diluted share count from 677 million to 660 million.

📞 Earnings Call Summary

During the earnings call, CEO Brian Chesky and CFO Ellie Mertz discussed several key points:

- Regional Performance:

- North America: Low single-digit growth in nights booked, indicating market maturity.

- EMEA: Mid-single-digit growth in nights booked.

- Latin America: Low-20s percentage growth in nights booked, with Brazil showing a 27% increase.

- Asia Pacific: Mid-teens percentage growth in nights booked.

- Product Development: Continued investment in enhancing the booking experience, including pricing transparency and guest-host communication tools.

- Market Trends: Noted a shift in Canadian travelers opting for destinations like Mexico over the U.S., attributed to economic uncertainties and changing travel preferences.

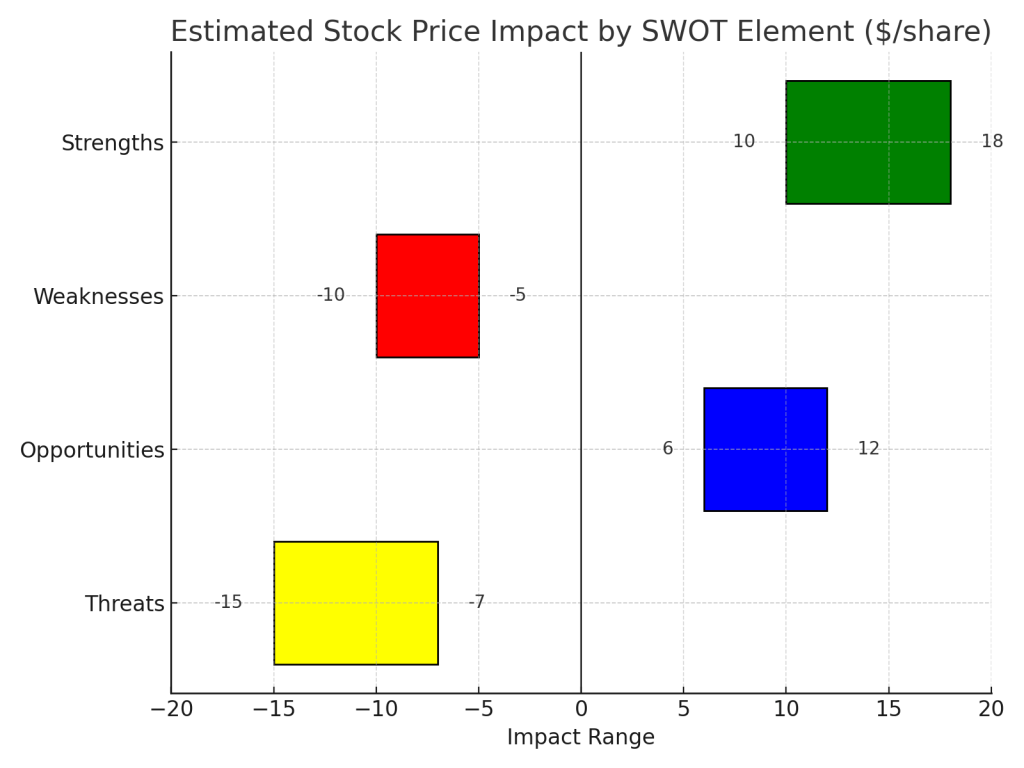

🧭 SWOT Analysis with Stock Price Impact

With the financial results and key management insights from the earnings call now clear, it’s important to step back and evaluate what these figures mean for Airbnb’s overall strategic position. A SWOT analysis—assessing the company’s strengths, weaknesses, opportunities, and threats—helps put the quarter’s performance into broader context and highlights the factors likely to influence Airbnb’s stock price trajectory in the months ahead.

Strengths (+$10–$15 per share)

Airbnb’s asset-light model continues to generate robust free cash flow ($1.8B in Q1), supporting strategic investments and share repurchases. The company’s global presence and brand recognition contribute to its resilience, potentially adding $10–$15 per share in valuation support.

Weaknesses (−$5–$10 per share)

Slower growth in North America and a slight decline in Average Daily Rate (ADR) suggest market saturation and pricing pressures. These factors may contribute to a $5–$10 per share reduction in valuation.

Opportunities (+$15–$25 per share)

Expanding into emerging markets like Latin America and Asia Pacific, coupled with product innovations, positions Airbnb for future growth. Successful execution could add $15–$25 per share in valuation upside over the next 12–18 months.

Threats (−$10–$20 per share)

Regulatory challenges in key cities and macroeconomic uncertainties, including currency fluctuations and geopolitical risks, pose potential threats. These could lead to a $10–$20 per share downside risk.

📌 SWOT Summary

| Strengths | Weaknesses |

|---|---|

| • Strong free cash flow: $1.8B in Q1, $4.4B TTM – supports reinvestment and buybacks. | • Slower growth in North America (low single digits) suggests market saturation. |

| • Global brand recognition and diversified regional exposure. | • ADR declined slightly YoY, indicating pricing pressure or product mix shift. |

| • High-margin, asset-light business model. | • Net income down 42% YoY, partly due to increased stock-based compensation and investment losses. |

| • Continued product innovation: pricing tools, guest-host features. | • FX impact and calendar shifts reduced headline revenue growth. |

| Opportunities | Threats |

|---|---|

| • Rapid growth in Latin America (+20%+) and Asia Pacific (mid-teens%) presents upside potential. | • Regulatory challenges in key markets (e.g., city-level restrictions on short-term rentals). |

| • New tools and enhancements could drive host satisfaction and retention. | • Macroeconomic uncertainty impacting travel demand (e.g., Canadian travelers shifting to cheaper destinations). |

| • Potential to further monetize experiences and expand internationally. | • Currency fluctuations and reduced interest income affecting bottom line. |

| • Share repurchase program enhances EPS over time. | • Increased competition from traditional hotels and new platforms. |

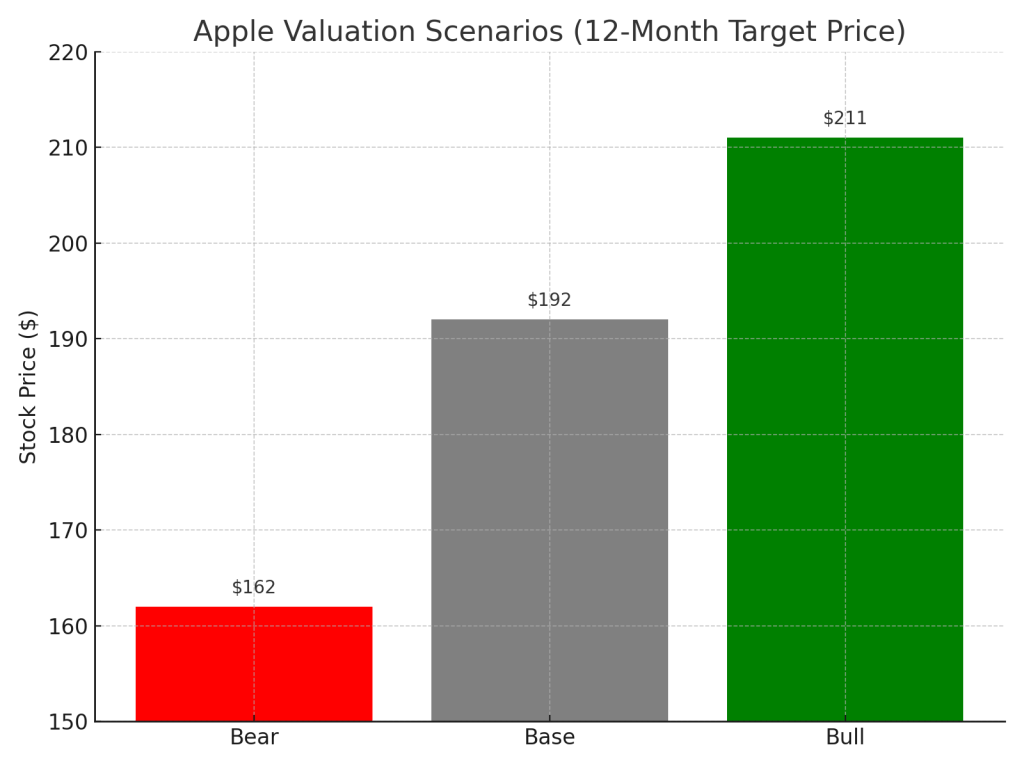

📈 Valuation Scenarios

With a clear view of Airbnb’s internal strengths and challenges, as well as the external opportunities and risks shaping its strategic landscape, we can now turn to what this all means for investors. By translating the qualitative insights from the SWOT analysis and quantitative performance data into valuation scenarios, we can estimate a reasonable range for the stock’s intrinsic value—under base case, bull case, and bear case assumptions. This helps assess whether Airbnb’s current share price accurately reflects its financial fundamentals and growth outlook.

| Scenario | Assumptions | Target Price | Probability |

|---|---|---|---|

| Base Case | Moderate growth with stable margins. | $130 | 60% |

| Bull Case | Strong global travel rebound and successful product roll-outs. | $145–$150 | 25% |

| Bear Case | Regulatory tightening and economic downturns. | $105–$110 | 15% |

💡 Final Verdict: Is Airbnb Fairly Priced?

At the current price of $125.26 (as of May 2, 2025), Airbnb appears to be fairly priced, reflecting a balance between its growth prospects and potential risks. Investors should monitor regional performance, regulatory developments, and macroeconomic indicators to assess future valuation trajectories.

Comment on Source Usage:

This analysis is based exclusively on Airbnb’s official Q1 2025 financial report and the corresponding earnings call transcript. No third-party news articles, analyst opinions, or external data sources were referenced. This approach ensures the insights presented reflect only the company’s own disclosures and strategic messaging.

Disclaimer:

This content is for informational purposes only and does not constitute financial advice, investment recommendations, or an endorsement to buy or sell any securities. Readers should conduct their own research or consult a qualified financial advisor before making investment decisions.

If you found this analysis helpful and want to stay ahead of key earnings insights, stock valuations, and strategic takeaways from top companies like Airbnb, subscribe now to receive our latest breakdowns straight to your inbox—no noise, just fundamentals.

Leave a comment