TL;DR Summary

Accenture (ACN:NYSE) delivered a solid quarter with record bookings and raised guidance, confirming strong enterprise AI demand. However, revenue growth remains in the mid-single digits, and margin pressure suggests AI investments are still in the build phase. The stock is trading close to its probability-weighted fair value, meaning future upside depends on execution—not narrative.

Quarter Recap

Accenture reported Q2 FY2026 results that reflect strong execution but measured growth. Revenue reached $18.0 billion, growing 7% in U.S. dollars and 4% in local currency. Adjusted EPS came in at $3.59, up 10% year over year, while GAAP EPS declined 4%.

The most notable metric was bookings, which hit a record $22.1 billion for a second quarter, indicating strong forward demand. The company also raised its full-year revenue growth guidance to 4–7%, reinforcing confidence in its pipeline.

However, margin trends were mixed. Adjusted operating margin improved slightly, but GAAP margins declined, reflecting continued investment in AI capabilities.

Key Highlights

- Revenue: $18.0B (+7% USD, +4% local currency)

- Adjusted EPS: $3.59 (+10% YoY)

- GAAP EPS: $3.19 (-4% YoY)

- Record bookings: $22.1B

- Raised FY2026 revenue growth guidance: 4–7%

- Free cash flow: $2.68B

- Share repurchases: $1.7B

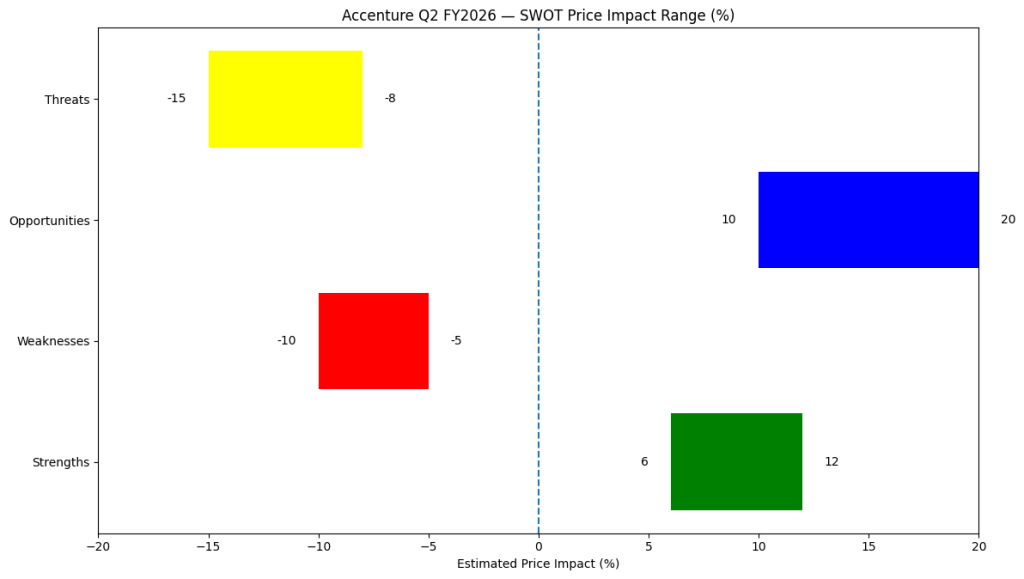

SWOT Analysis

Accenture’s results reinforce its position as a high-quality execution platform for enterprise transformation and AI adoption. The company is seeing strong demand and improving visibility, but the market is still waiting for clear evidence that this demand can translate into sustained revenue acceleration and margin expansion.

Strengths

- Record bookings ($22.1B) → strong forward revenue visibilityEstimated impact: +6% to +10%

- Raised FY2026 guidance (4–7%) → improving confidenceEstimated impact: +4% to +7%

- Balanced model (Consulting + Managed Services)Estimated impact: +3% to +6%

- Positioned as enterprise AI orchestrator across ecosystemsEstimated impact: +5% to +12% (long-term)

Weaknesses

- Revenue growth still mid-single digit (4% local currency)Estimated impact: -5% to -10%

- GAAP margin compression (-70bps)Estimated impact: -3% to -6%

- GAAP EPS decline (-4% YoY)Estimated impact: -3% to -5%

Opportunities

- AI bookings converting into revenue accelerationEstimated impact: +10% to +20%

- Early-stage enterprise AI adoption cycleEstimated impact: +8% to +15%

- Large deal momentum (41 clients >$100M bookings)Estimated impact: +5% to +10%

Threats

- AI commoditization (clients internalizing capabilities)Estimated impact: -8% to -15%

- Hyperscalers capturing more value chainEstimated impact: -5% to -12%

- Macro-driven IT spending volatilityEstimated impact: -6% to -10%

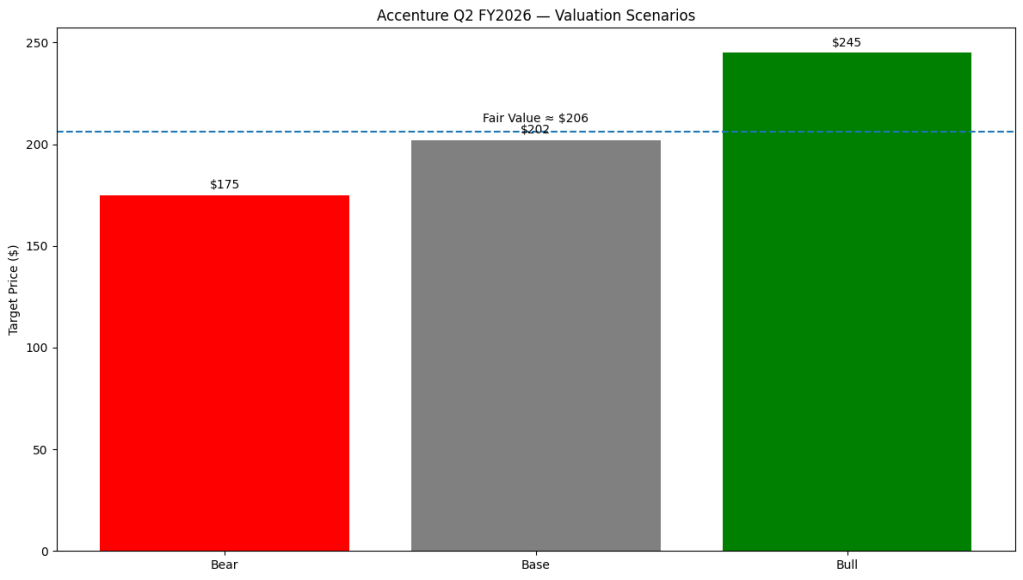

Valuation Scenarios

Accenture is currently being valued as a stable, high-quality operator with AI exposure, but not yet as a high-growth AI beneficiary. The key variable remains whether strong bookings can translate into sustained revenue acceleration.

Bear Case — $170 to $180

If revenue growth remains around 4–5% and AI demand takes longer to convert into revenue, while margins remain under pressure, the stock could see multiple compression toward traditional consulting peers.

Base Case — $195 to $210

If Accenture delivers within its updated 4–7% growth guidance and AI contributes incrementally without significantly accelerating growth, the stock is likely to remain around current levels with modest upside.

Bull Case — $230 to $260

If AI bookings translate into revenue acceleration above 8–10% and margins expand through operating leverage, Accenture could be re-rated as a leading AI execution platform.

Probability-weighted fair value

Based on the scenario analysis:

- Bear case (25%): ~$175

- Base case (50%): ~$202

- Bull case (25%): ~$245

👉 Estimated fair value: ~$206

At a current price of around $203, Accenture is trading very close to its probability-weighted fair value, suggesting that the market is already pricing in its current level of execution.

Verdict

Accenture continues to execute well, supported by strong demand and improving guidance. However, the market is still waiting for clear evidence that AI demand can drive sustained revenue acceleration.

At current levels, the stock appears fairly valued. This shifts the investment case from valuation-driven upside to execution-driven upside.

For now, Accenture remains a “show-me” story—a high-quality compounder with AI optionality, but not yet a full AI re-rating.

Call to Action

If you want more breakdowns like this—focused on how earnings translate into real price impact—follow SWOTstock for SWOT analysis on major companies.

Disclaimer

This analysis is for informational purposes only and does not constitute financial advice. Always conduct your own research before making investment decisions.