AI is changing everything — and faster than any technology before it.

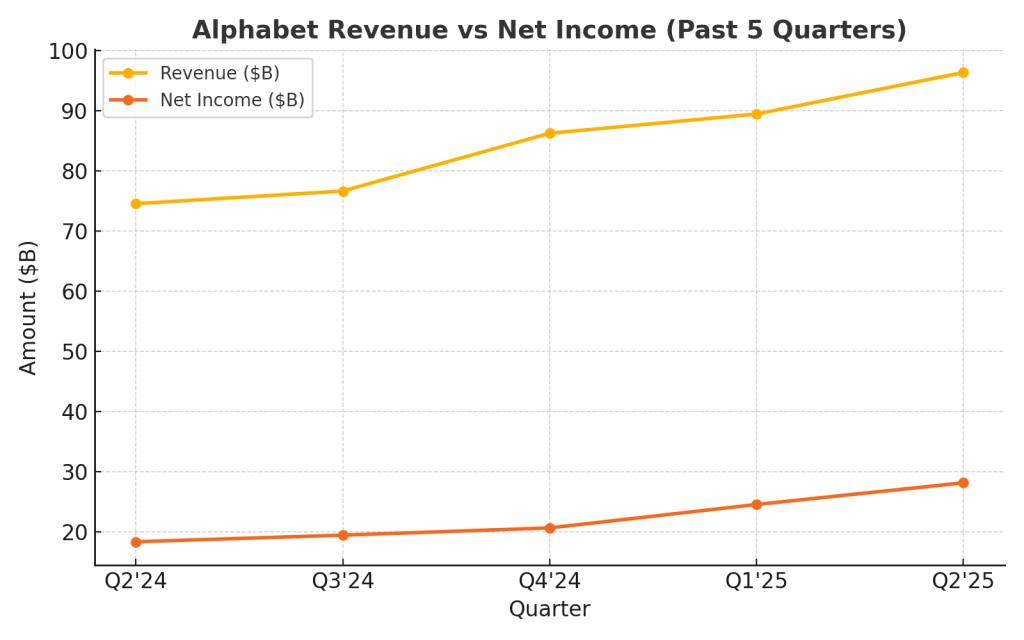

Google, Microsoft, Amazon, and Meta are spending tens of billions on AI and data centers, betting big on a future where intelligent systems power every part of business and life. Alphabet alone has raised its 2025 CapEx guidance to $85 billion — the biggest single‑year infrastructure push in its history.

This is thrilling — but it’s also unsettling.

Because history tells us that when technology moves this fast, people and communities often get left behind.

We’ve Seen This Before

AI may feel new, but the playbook isn’t.

- 1980s: Robots transformed auto plants. Companies promised “upskilling,” but Rust Belt towns were hollowed out.

- 1990s: Office computers streamlined workflows. Administrative jobs shrank. New IT careers emerged — but in different cities, for different people.

- 2000s: The internet created digital giants and e‑commerce while wiping out thousands of brick‑and‑mortar businesses.

Every time, it’s the same two‑step:

- Phase 1: Use new tech to cut costs and boost margins.

- Phase 2: Eventually reinvest the gains to create new industries and jobs — often far away from those disrupted by Phase 1.

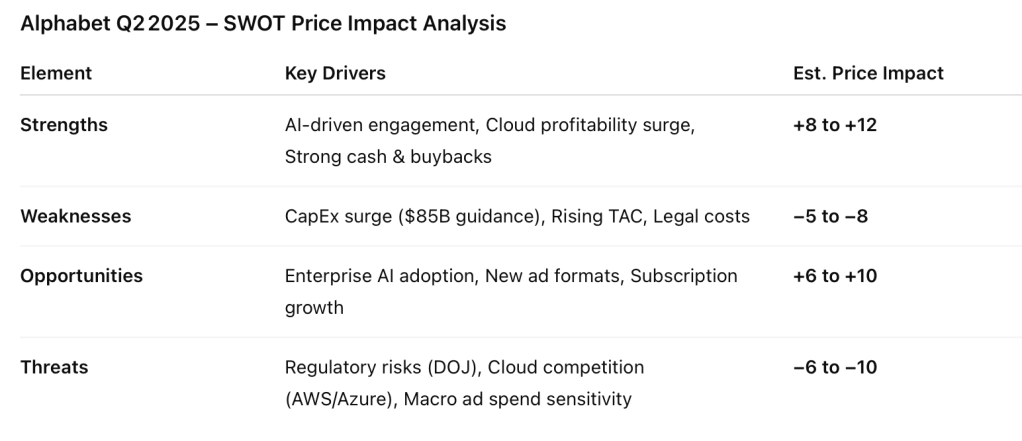

AI’s SWOT: Where We Stand Today

Looking at this AI revolution through a SWOT lens:

Strengths:

Big Tech has the scale, cash, and vision to reimagine industries. Google is reshaping search with AI Overviews. Microsoft wants Copilot in everything. Amazon is transforming logistics and the cloud. They’re building capabilities that could change how the world works.

Opportunities:

These investments could unlock entirely new markets — AI‑driven enterprise services, personalized tools, and products we can’t yet imagine. If done right, this could spark another tech‑driven growth era, creating jobs and opportunities across the economy.

Weaknesses:

The spending is enormous — Alphabet’s CapEx jumped 70% YoY — and it’s based on a bet that demand for AI will match the scale of these build‑outs. If enterprise adoption slows or ROI disappoints, this could become overcapacity, not innovation.

Threats:

The social cost is already visible: layoffs in tech, finance, and operations. Productivity gains are flowing to shareholders and elite talent — not the communities losing jobs. Political backlash is building. Regulators are circling. And if the economy slows — tariffs, inflation, geopolitical shocks — these bold bets could quickly look like overreach.

Why This Matters Beyond Big Tech

This isn’t just a Silicon Valley story.

- Communities are hollowing out. The jobs being cut aren’t coming back to the same towns.

- Wealth is concentrating. AI’s early gains are flowing to the top — executives, shareholders, and highly skilled tech workers.

- Politics are polarizing. Resentment over lost livelihoods is fueling unrest and hardening divisions worldwide.

AI isn’t the cause of these divides — but it’s accelerating them.

The Choice Ahead

Here’s the good news: this doesn’t have to end the way previous tech disruptions did.

Big Tech can choose to:

- Reinvest productivity gains into building new industries and creating meaningful roles for displaced workers.

- Upskill employees so they can thrive in an AI‑powered economy instead of being left behind by it.

- Partner with communities and governments to make AI adoption a growth engine for more than just shareholders.

This isn’t about slowing innovation. It’s about making sure progress works for more than a few.

Bottom Line

AI is the boldest bet Big Tech has made in decades. It has the potential to change everything — how we work, how we live, how we create.

But if these investments remain focused only on efficiency and cost‑cutting, they won’t just disrupt industries. They’ll deepen inequality, fuel resentment, and harden the divides already pulling societies apart.

If instead they’re used to build new opportunities for more people, AI could be remembered not as a disruptor, but as the engine of a new era of shared growth.

That choice is still on the table.

What do you think? Are these bold AI investments building a better future for everyone — or just for a few?

Leave a comment