Palantir (NASDAQ: PLTR) dropped a strong Q1 2025 earnings report. Revenue was up, profits were solid, and its AI platform (AIP) is gaining traction. But even with all the good news, the stock dropped 8% after earnings. So… what gives?

Well, it might be less about the business—and more about the price. Let’s break it down, in plain English.

📊 Quick Q1 2025 Snapshot

- Revenue: $634M (+39% YoY)

- U.S. Commercial Revenue: $255M (+71% YoY)

- Net Income: $214M

- Free Cash Flow (FCF): $441M (42% margin)

- Big Contracts (>$10M): Up 73%

- Customer Count: Up 39% YoY

- Stock reaction: −8% after earnings

Palantir’s business is clearly growing, but investors are now wondering if the current stock price has already priced in too much future success.

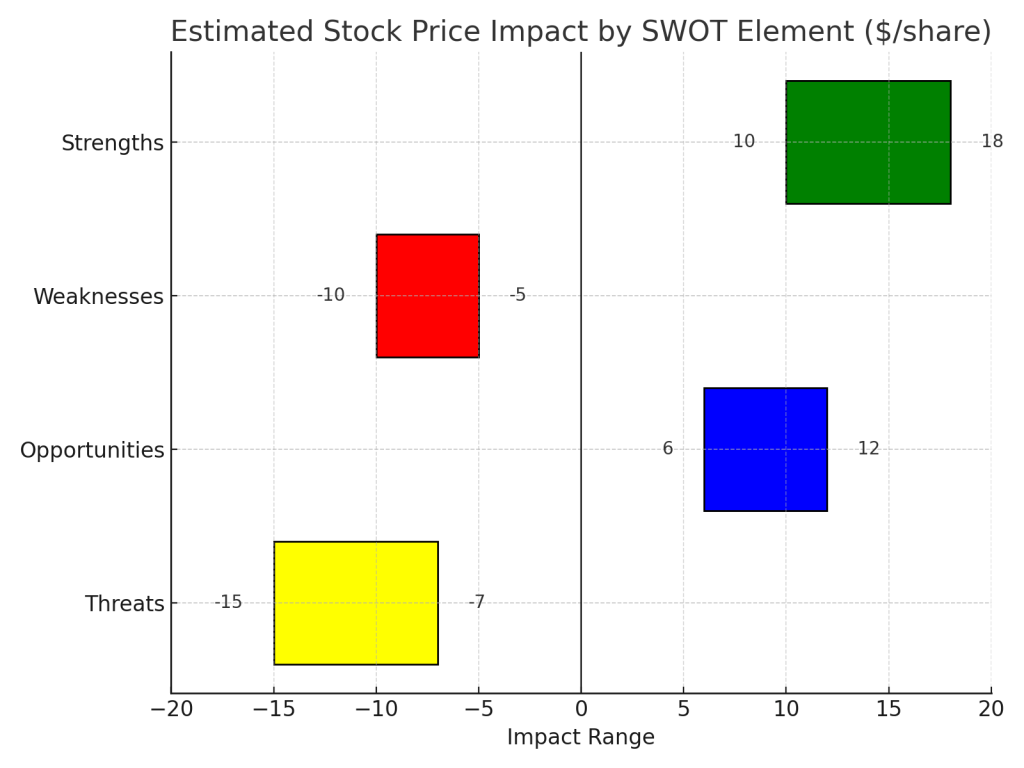

🧠 SWOT Analysis: Strengths, Weaknesses, Opportunities, Threats

Let’s run through a full SWOT breakdown—plus what each factor means for the stock’s value.

✅ Strengths: Commercial Business on Fire

Palantir’s commercial segment (especially in the U.S.) is growing like crazy. They’re moving beyond defense and government, and they’re finally generating serious free cash flow.

📈 Valuation Impact: +32%

We estimated that if this growth holds, it adds about $24 per share to fair value. This is based on raising long-term FCF assumptions and applying a ~30x FCF multiple to commercial earnings.

- U.S. commercial revenue up 71%

- High-margin, cash-generating operations

- Expanding large enterprise footprint

❌ Weaknesses: Still Relying on Government

Half the business still depends on U.S. government contracts. That’s stable… until it’s not. Also, Palantir’s international revenue isn’t keeping up, and that limits its global reach.

📉 Valuation Impact: −15%

This knocks $11 off fair value by capping international growth and assigning a lower multiple to defense-related revenue.

- Heavy reliance on U.S. federal contracts

- Global growth is slow

- Business model less diversified than peers

🚀 Opportunities: AI Enterprise Boom

Palantir is well-positioned to ride the enterprise AI wave. AIP is getting traction, and the company is now partnering with cloud players like AWS to reach more customers, faster.

📈 Valuation Impact: +18%

This adds ~$13 to fair value, assuming they grow revenue at a 25% CAGR over the next 5 years in the commercial AI segment.

- AI use cases expanding fast

- Partnerships make scaling easier

- Total addressable market is huge and growing

⚠️ Threats: Big Tech Competition, Regulation

Google, Microsoft, Amazon—all building their own enterprise AI tools. Plus, Palantir still faces scrutiny over its military/government work, which could lead to reputational or regulatory challenges.

📉 Valuation Impact: −18%

We subtracted ~$13 from fair value assuming increased sales competition and legal friction reduces margin and contract growth.

- Big tech is moving in

- Regulatory/political risks

- Defense-related perception issues persist

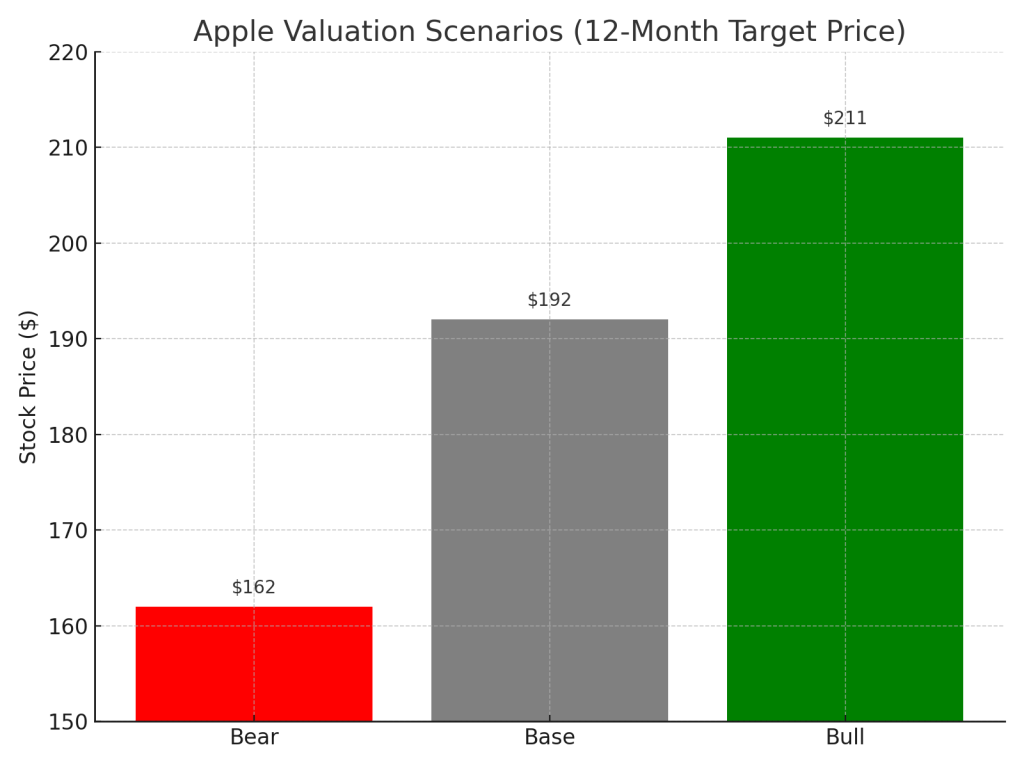

📊 Valuation: What’s the Stock Worth?

We pulled all the SWOT impacts together to estimate a fair value:

- Base Case Fair Value: ~$88

- Bull Case (faster commercial + AI wins): ~$110

- Bear Case (slow adoption + regulatory issues): ~$65

- Current Price: ~$124

👉 Conclusion: The stock looks about 30% overvalued right now based on fundamentals and growth assumptions. It’s a great company, but the market might be pricing in perfection.

💡 Final Take

Palantir is clearly executing well. Their AI platform is getting adopted, they’re profitable, and they’re building momentum in the commercial space. But the stock might be a bit ahead of itself right now.

If you’re in it for the long haul and believe in Palantir’s AI vision, it might still be worth holding. But if you’re looking to start a position, it could make sense to wait for a pullback.

📌 Disclaimer & Final Notes

This analysis is based solely on official company disclosures—including Palantir’s Q1 2025 financial report, earnings call transcript, and direct management commentary. No third-party commentary or speculative sources were used.

Please note that this content is for informational purposes only and does not constitute investment advice. Always do your own research or consult a licensed financial advisor before making investment decisions.

📬 Want more no-nonsense breakdowns of AI stocks and earnings?

Subscribe to stay updated with the latest earnings summaries, fair value estimates, and plain-language analysis—tailored for everyday investors who want to stay sharp.

One response to “Palantir Q1 2025 Earnings Recap: Big Numbers, Big Valuation?”

-

[…] check out our recent breakdowns of AMD Q1 2025, Palantir Q1 2025, Meta Q1 2025 and Alphabet Q1 2025 for more actionable […]

LikeLike

Leave a comment