TL;DR

AI fears triggered a massive selloff in software stocks over the past few weeks, and Intuit (INTU:NASDAQ) was caught in the narrative that generative AI could replace tax preparation and accounting software.

But Intuit’s latest earnings suggest the opposite may be happening.

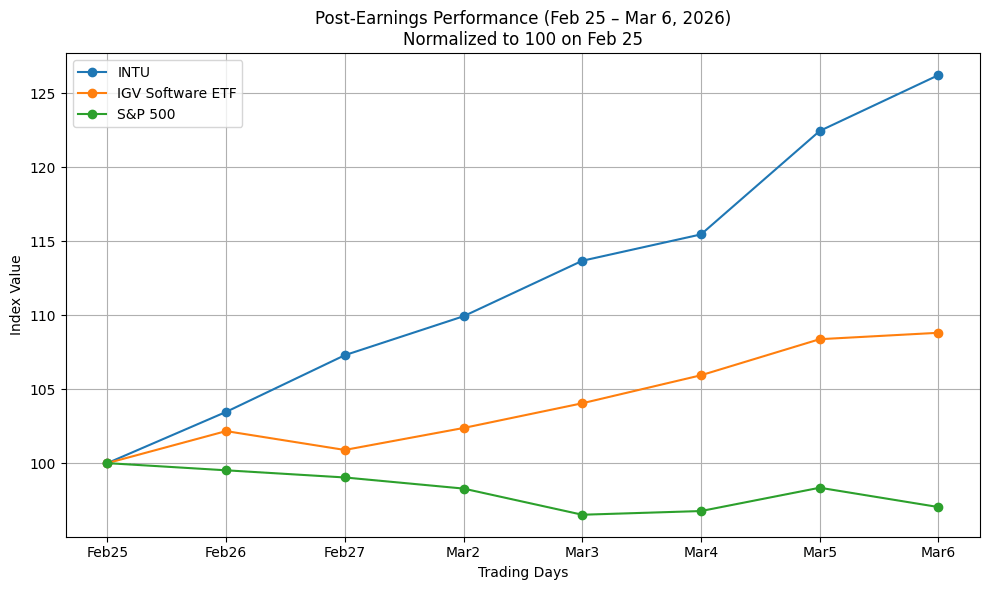

From the day before earnings to March 6, Intuit’s stock surged about 26%, dramatically outperforming both the software sector ETF IGV (~+9%) and the S&P 500 (~-3%) over the same period.

The divergence suggests investors may be reassessing the AI disruption thesis.

Tax preparation is not just software. It involves regulatory compliance, legal liability, and long-term financial data trust — structural advantages that favor incumbents like Intuit.

Quarter Recap

Intuit’s latest quarterly results demonstrated continued strong momentum across its core businesses.

Key highlights:

- Revenue grew 17% year-over-year

- Non-GAAP EPS increased 25%

- Small business and consumer segments both delivered solid growth

- Full-year guidance remained intact

Despite widespread fears that AI could undermine the company’s value proposition, the earnings report showed no signs of structural weakness in demand.

Instead, the results reinforced that Intuit’s ecosystem continues expanding across tax preparation, accounting, payroll, and financial management services.

Market Reaction

The most telling signal came from the market’s reaction.

From February 25 to March 6:

- Intuit (INTU): +26%

- Software ETF (IGV): +9%

- S&P 500: -3%

This divergence indicates the rally was company-specific, not simply a sector move.

While broader markets struggled with geopolitical tensions and macro volatility, investors appeared to reprice Intuit upward after reassessing the AI threat narrative.

Key Highlights

Three structural factors help explain why AI disruption may be harder than many investors initially assumed.

1. Tax preparation involves legal liability

Tax returns are not just informational outputs.

They represent legally filed financial documents.

Companies like Intuit effectively stand behind the accuracy of their systems. If errors occur, audits and penalties can follow.

An AI chatbot providing general advice does not carry the same legal responsibility.

2. Regulatory infrastructure creates barriers

Tax software integrates directly with government filing systems, financial institutions, and accounting workflows.

This infrastructure took decades to build and maintain.

AI models alone cannot easily replicate these regulatory integrations.

3. Financial data trust forms a powerful moat

Millions of individuals and businesses store years of financial history inside the Intuit ecosystem.

That historical data matters for:

- tax carry-forwards

- financial planning

- bookkeeping continuity

- compliance records

Switching platforms introduces risk and friction, strengthening customer retention.

SWOT Analysis

Strengths

Intuit’s moat rests on regulatory integration, trusted infrastructure, and proprietary financial data.

These advantages make the company far more resilient to AI disruption than typical SaaS providers.

In fact, AI may enhance the platform by enabling new capabilities such as automated bookkeeping, predictive financial insights, and tax optimization.

Estimated price impact: +$40 to +$80

Weaknesses

Despite the recent rally, Intuit still faces high expectations for continued growth.

If growth slows significantly or AI commoditizes certain services, the market could compress valuation multiples.

Estimated price impact: −$20 to −$40

Opportunities

AI could expand Intuit’s platform into a broader financial operating system for individuals and small businesses.

Potential capabilities include:

- automated financial forecasting

- real-time tax planning

- intelligent expense classification

- AI-assisted audit preparation

These features could increase platform engagement and raise switching costs.

Estimated price impact: +$60 to +$120

Threats

Some adjacent product areas — particularly marketing automation and other software services — face more traditional competitive pressures.

Additionally, government initiatives around simplified tax filing could create long-term competitive risks.

Estimated price impact: −$40 to −$80

Valuation Scenarios

Bear Case — AI commoditizes some services

If growth slows to high-single digits and valuation multiples compress:

Estimated fair value: $350–380

Probability: 25%

Base Case — AI enhances the platform

If Intuit maintains mid-teens growth and expands its ecosystem:

Estimated fair value: $430–480

Probability: 50%

Bull Case — AI expands the TAM

If AI significantly increases platform engagement and revenue opportunities:

Estimated fair value: $550–650

Probability: 25%

Probability-Weighted Fair Value

Combining the three scenarios yields an estimated fair value around:

~$470 per share

Verdict

The recent earnings report does not support the idea that AI will disrupt Intuit’s core business.

Instead, the evidence suggests something more nuanced.

In industries where software intersects with legal responsibility, regulatory integration, and trusted financial data, AI may actually reinforce incumbents rather than displace them.

Intuit appears to be one of those cases.

The stock’s strong post-earnings rally suggests investors are beginning to recognize this dynamic.

Call to Action

If you enjoy this type of analysis, follow SWOTstock for more deep dives into how structural industry forces shape long-term stock performance.

Disclaimer

This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consider their risk tolerance before making investment decisions.